By any measure, the first quarter of 2026 was a record setter for venture capital fundings, according to a final report by Pitchbook and the National Venture Capital Association (NVCA).

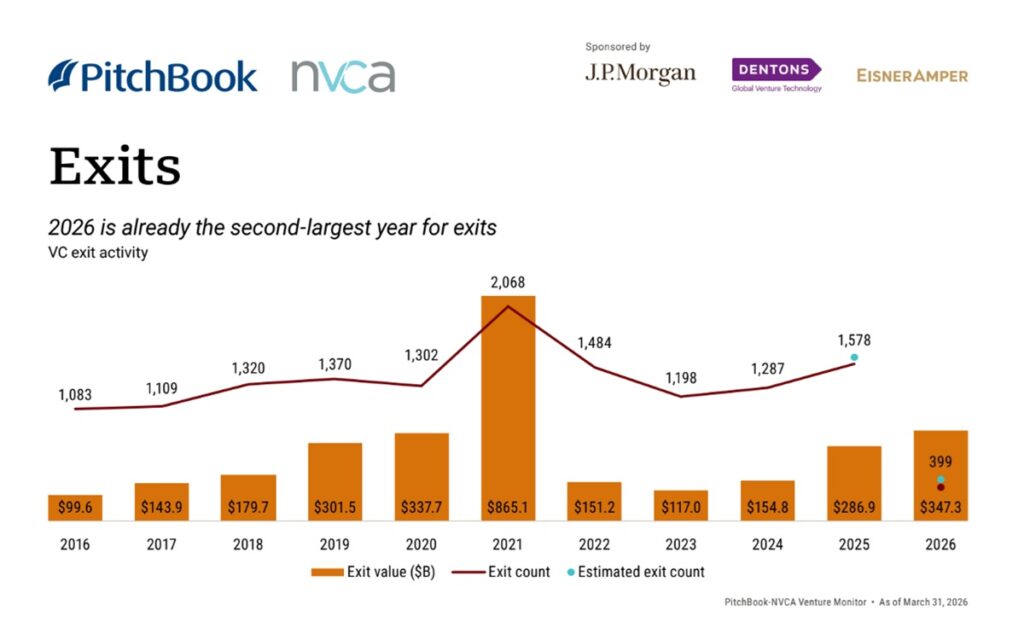

The $267.2 billion in quarterly deal value topped all full-year totals except for those of 2021 and 2025, and the $347.3 billion in exit value set a quarterly high, already placing 2026 as the second-highest year for exit value ever.

However, the foundation of the fundings was narrow in the sense that there were focused on AI, and if you take out the five largest deals, the figures ball by 73.2%. If you exclude the five largest exits, the value falls by 86.6%, the report said.

“Concentration has increasingly defined VC over the past couple years, but Q1 marked a

new extreme. Capital is consolidating around a narrower set of perceived winners than ever before,” said Nizar Tarhuni, executive vice president of research & market intelligence at PitchBook, in a statement.

He noted most of the money went ot just five firms. It’s worth noting these numbers are gargantuan compared to what is going into the games industry (the low billions for funding).

“These are not the signals of a broad recovery — they’re the signals of a market where a shrinking group of players is setting the terms, and where record headlines are obscuring how little has changed for the rest of venture. Liquidity is still tight, the IPO window remains mostly closed, and founders and fund managers outside that top tier are navigating a market that looks very different than the numbers suggest,” Tarhuni said.

Concentration has defined VC in recent years, but Q1 marked a new extreme. Four deals above $15 billion were completed, including OpenAI’s $122 billion financing, and xAI’s merger with SpaceX was the largest VC-backed exit of a US company ever, though the

narrative was muted because SpaceX is gearing up for an estimated $1.5 trillion+ IPO later this year, the report said.

Underneath the big numbers

Beneath the top-line figures, the market remains much the same as it was in liquidity continues to be tight for most of the market, and there has not been significant movement in IPO registrations. The onset of the war in Iran has added another obstacle to opening the IPO window. After tariffs and a government shutdown weighed on 2025’s new listings, Q1 2026 contended with fresh policy and geopolitical risks, the NVCA/Pitchbook report said.

The public software-as-a-service- and AI-induced market volatility in late February revealed a market on edge—and that investors are searching for reasons to sell amid the uncertainty. VC-backed tech startups continue to struggle with elevated past valuations, uncertain market conditions, and looming mega-IPOs.

To say the market underneath is unchanged from the past few years does not discount the strength at the very top. Potential IPOs from SpaceX, Anthropic, OpenAI, Databricks, and Stripe would provide an enormous windfall; the top three listings could near $2.5 trillion in exit value, more than the total of all the IPOs in this century. However, this potential masks challenges that still characterize the market.

The median VC IRR for North American fund vintages since 2019 sits in the single digits, and the median distributions to paid-in multiple for vintages over the past decade remains

below 1x. Until there is a broader move to unlock liquidity, a large portion of the venture market will remain constrained.

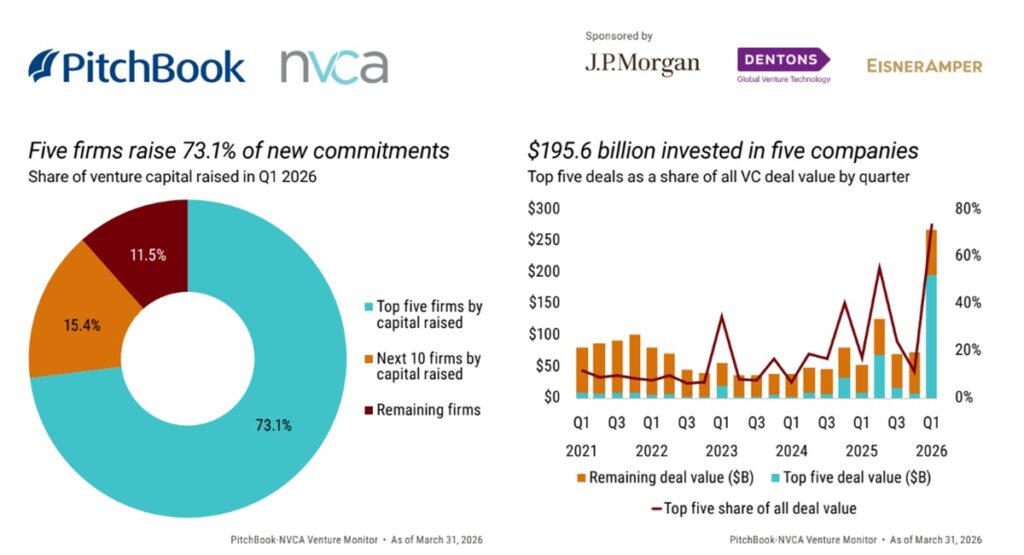

Looking ahead to the rest of 2026, annual records for deal value and exits will undeniably be a theme. Fundraising is on a different trajectory. 73.1% of the capital committed in Q1 went to five VC firms, and emerging managers dcontinue to struggle mightily with attracting capital. As LPs look ahead, the uncertainty in public equity markets will likely weigh on their willingness and ability to commit capital to new VC funds. This will not impact megafunds nearly as much as smaller vehicles and firms, which will rely more heavily on smaller, less flexible LPs. More funds over $1 billion closed in Q1 than during

all of 2025, and we expect megafund counts to continue to surge toward 2022 highs.

VC has entered the era of consensus deals, and that dynamic will likely persist. Across all stages and series, a small portion of companies is vastly outraising the rest. As concentration continues to build in funds, those with dry powder will pile into the perceived “top” deals, pushing valuations and deal sizes higher. The median seed pre-money valuation has risen to $18.4 million, which is more than double the figure of 2021. The fast pace of development in AI puts a premium on capital, and those companies with the agility afforded by larger cash bases and large fund investors have leverage to move fast and win.

For liquidity’s sake, 2026 was supposed to build on monetary easing and deliver several more rate cuts that could have raised risk appetite among investors and driven demand for growth tech stocks.

Wall Street is currently pricing in zero rate cuts for the rest of the year. Uncertainty in the market—and the potential economic pressure that could weigh on liquidity and investment in AI-related sectors—is a burden the market must now carry.

VC dollars are flowing to fewer companies in larger amounts at increasingly elevated valuations. This dynamic is evident across every stage of the market, not just among

marquee names.

Median pre-money valuations and deal sizes have steadily expanded across series. The median Series A pre-money valuation reached $62 million in Q1— nearly triple the $21 million recorded in 2020—while the median Series A deal size rose to $19.6 million from

$7.5 million over the same period. At Series C, the moves were even more striking: The median pre-money valuation surged to $579 million from $167.2 million in 2020, and the median deal size expanded to $75 million from $35 million. These are not incremental

changes but a sustained shift in the cost to participate at each stage of the venture lifecycle. Half of early-stage deals now exceed $10 million, the highest share of large early-stage deals in the past decade.

The wide gap between median and average deal sizes tells an equally important story. At Series A, the Q1 2026 median of $19.6 million sits well below the average of $39.6 million; at Series C, the $75 million median sits well below the average of $124.6 million. The persistent and widening divergence between median and average deal sizes reflects an

increasingly bifurcated market.

Over the past four quarters, deal counts have increased most notably for the early stage due to two tailwinds, the report said. First, aging dry powder is creating pressure as the significant capital raised for early-stage investing has yet to be deployed. Second, the most active firms have materially accelerated their pace of seed and early-stage investments:

In Q1, Andreessen Horowitz and Y Combinator each made 46 investments, General Catalyst made 25, and Sequoia Capital made 22. Together, these trends reflect a structural shift in how leading managers are approaching portfolio construction, favoring volume and velocity at the earliest stages.

The early-stage resilience is real, but it will take years before those investments are realized. The market’s more immediate liquidity problem remains unsolved—particularly as the aggregate post-money valuation of unicorns has crossed $5.8 trillion. 44.6% of those unicorns had their first VC round in 2016 or earlier, meaning that the early investors and employees of nearly half of all unicorns have been waiting more than a decade to realize returns.

The result is a market increasingly defined by divergence: abundant capital and rising valuations at the top and a growing cohort of mature companies with no clear path to liquidity at the bottom.

The top unicorns

The top unicorns were identified by the NVCA/Pitchbook report. The IPO probably for those companies was 96% to 97%. They included Zipline, OpenAI, Databricks, Glean, Whoop, Institutional Capital Network, Apptronik, Kraken, Tomorrow.io, Mainspring, Ramp, Cerebras Systems, Ayar Labs, Whatnot, Sila, Form Energy, Cursor, SpaceX, PsiQuantum, Clear Street, Gecko Robotics, Mammoth Biosciences, Tenstorrent, Upgrade and HawkEye 360, the report said.

AI is the new VC

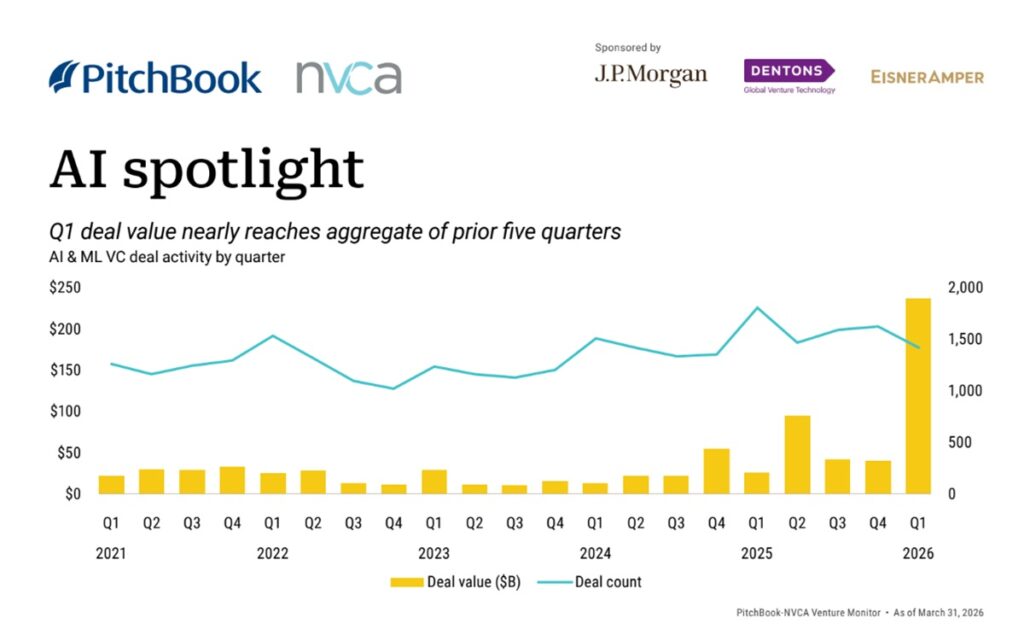

The statement “AI is the new VC” is difficult to challenge, the report said. AI companies’ proportion of all completed deals has risen every quarter but one since 2022. 42.5% of deal count in Q1 involved an AI startup. As large as that figure seems, especially compared with AI’s 14.6% share a decade ago, it still understates investors’ heightened focus on AI.

More than half (51.7%) of the megadeals completed during Q1 involved AI companies, and the market value of AI startups is now only outpaced by that of software-as-a-service startups, which greatly overlap with AI companies and hold a large amount of value from 2021 deals that has likely deteriorated since.

The AI trade in VC has been driven by enthusiasm for the technology’s future; its ability to immediately create efficiencies for young companies; and, largely, FOMO. The speed with which AI deals are getting done far outpaces non-AI dealmaking. AI companies that closed rounds in Q1 did so roughly half a year sooner than non-AI companies.

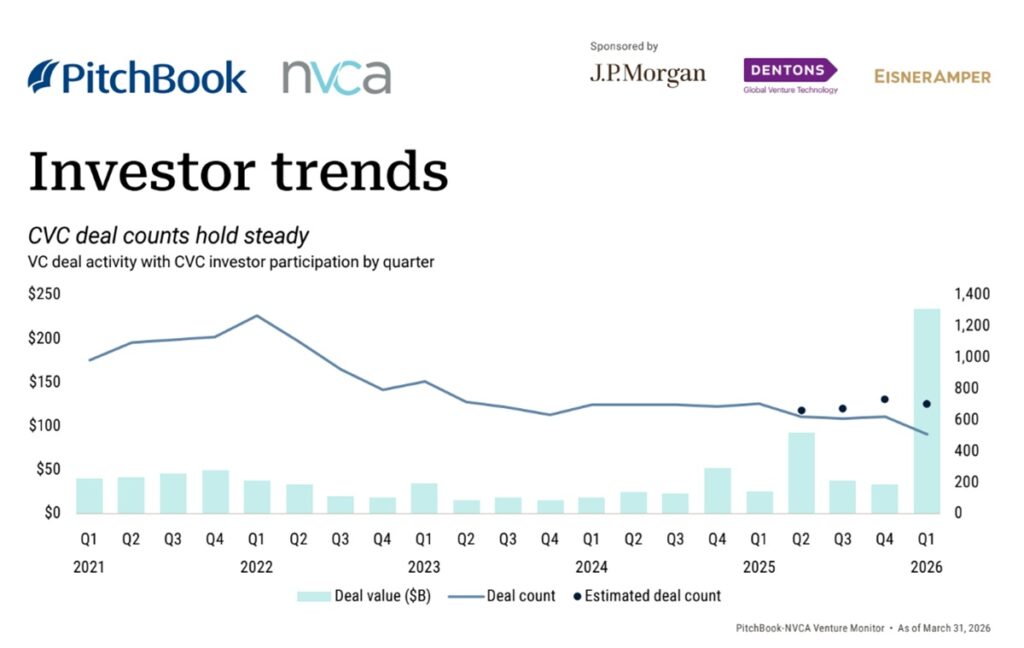

VC firms are not the only ones deploying capital into AI at scale, either. Beyond the megacap public hyperscalers, smaller and more traditional corporate VC firms (CVCs) have shifted their focus to AI to harness the strategic and financial gains the technology could

deliver for their parent organizations. In Q1, more than half of CVC deals were in AI.

The next phase of AI momentum and VC deployment is already underway. With OpenAI and Anthropic on the IPO doorstep, the rest of 2026 may begin to reveal the returns that AI investments can generate. Those two IPOs could serve as a catalyst for additional companies to file and generate liquidity—provided their listings receive a strong reception and sustain a positive performance.

The chase for AI druns throughout the venture lifecycle. AI is the most invested vertical at every stage. AI companies move through the early venture lifecycle at much higher rates than non-AI companies, and at higher valuation step-ups, reflecting strong investor conviction for AI even at the earliest stages.

The IPOs of OpenAI and Anthropic will not be ordinary. They will likely be transformational listings that chart a path for AI investment more broadly. The structural position of these

companies within AI places significant weight on their success, as a growing number of businesses are being built on the models they have developed, the report said.

Exits

With only one quarter completed, 2026 is already breaking exit records. Q1 generated $347.3 billion in exit value, the highest quarterly total on record by a wide margin. 2026 already has the second-highest annual exit value in history, trailing only 2021, the report said.

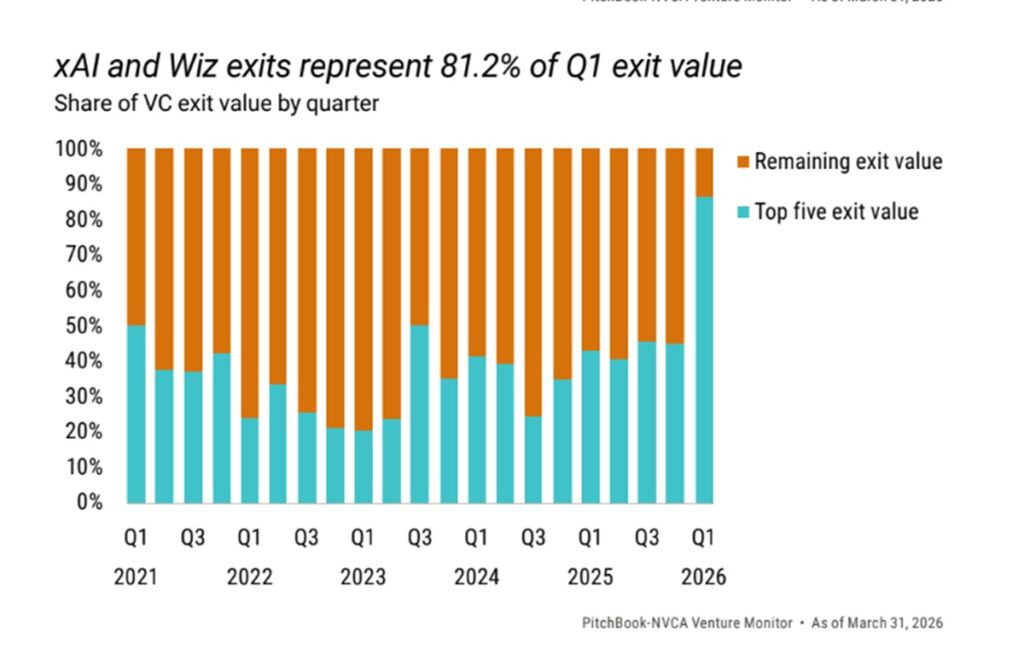

These figures do not, however, reflect the current state of VC exit activity, which remains largely frozen. A single transaction accounts for 72% of the quarter’s exit value: SpaceX’s $250 billion acquisition of xAI. Both are Elon Musk’s companies, making this less a traditional acquisition than a consolidation of affiliated assets.

Excluding it, the quarter’s underlying exit environment looks considerably more modest at $97.3 billion, which is still the highest quarter since Q4 2021. The concentration problem runs deeper still: 86.8% of Q1 acquisitions had undisclosed valuations, implying significant markdowns and limited returns for investors. That said, any liquidity in an extended stalemate is valuable, even at a discount, the report said.

The quarter’s top acquisitions were centered on the AI strategy. Google finalized its $32 billion acquisition of cybersecurity company Wiz, the largest corporate acquisition of a

VC-backed company on record. Marvell Technology’s $6 billion acquisition of Celestial AI addresses the high-bandwidth, low-latency connectivity demands of large-scale AI deployments. Cybersecurity firm Palo Alto Networks’ $3.4 billion acquisition of observability platform Chronosphere targets the challenges of monitoring The IPO market continued its measured recovery in Q1. The quarter’s 15 VC-backed IPOs put 2026 on pace for 60 listings—above 2025’s 50 but well short of what is needed to clear the years-

long backlog. 40% of the quarter’s IPOs were in biotech & pharma, driven by the listing companies’ focused paths to commercialization, advancing clinical trials, and more disciplined capital requirements.

This represents a notable shift from the platform-heavy wave of 2021, when companies went public on the promise of their science rather than the strength of their products.

Two of Q1’s largest IPOs, EquipmentShare and BitGo, capture a pattern that defined 2025 listings and is expected to continue in 2026. These companies were either profitable or

operated in sectors closely aligned with the Trump administration’s policy priorities, such as AI, crypto, aerospace, and defense. Construction rental firm EquipmentShare, which reported a 2025 net income of $40 million, was profitable at the time of its listing. As

a digital asset infrastructure company, BitGo reflects the crypto tailwind, with $8.1 million in net income on $10 billion in revenue for the first nine months of Both companies listed in January,were priced above their marketed ranges, and saw initial enthusiasm quickly fade—a pattern that has become yet another reason the IPO pipeline remains thin, the report said.

The most consequential variable for 2026’s IPO outlook has yet to materialize. Potential listings from SpaceX, OpenAI, and Anthropic—each of which would rank among the largest

IPOs in history—could reshape the exit landscape entirely, for better or worse. Strong reception would serve as a catalyst, reaffirming public market appetite for high-growth, venture-backed businesses and encouraging additional companies to file. The risk, however, is equally significant: If these mega-IPOs absorb available underwriting capacity

and institutional allocation, the resulting crowding-out effect could push the return of IPOs into 2027, further straining VC’s liquidity needs.

Fundraising results

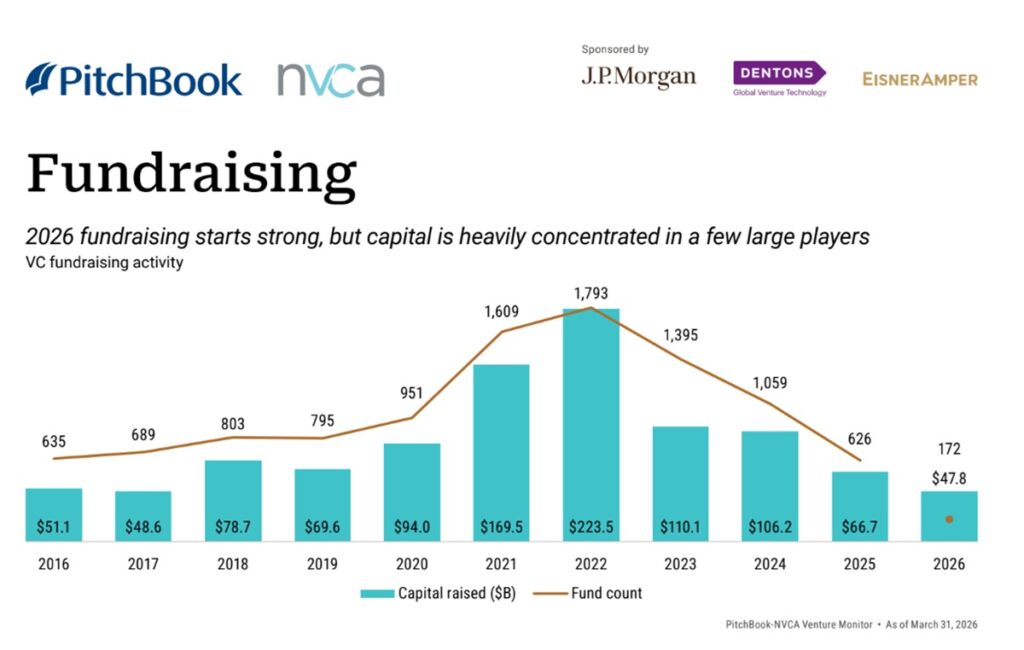

In Q1 2026, $47.8 billion was raised across 172 funds. Compared with the full-year 2025 total of $66.7 billion, the Q1 figure suggests the fundraising market is recovering. The headline number is distorted, however, by extreme capital concentration within a

handful of large managers.

Six managers—Andreessen Horowitz, Thrive Capital, Founders Fund, Battery Ventures, Kleiner Perkins, and Lux Capital—together raised $36.4 billion, or 76.2% of the quarter’s total capital, meaning the remaining funds closed during the quarter accounted for less

than 25% of the Q1 capital raised.

This concentration is not new—it was building throughout 2025—and carries meaningful implications. As AI-driven companies sustain capital-intensive development cycles and continue to delay public listings, large funds are well positioned to support portfolio

companies through extended holding periods without forcing premature liquidity events. A core risk to the market, however, is compounding concentration at both the fund and

company level. A significant share of capital is being deployed into AI companies whose valuations, in many cases, rest more on anticipated growth trajectories than on realized financial performance. A meaningful correction in AI sentiment or fundamentals would

reverberate broadly across the venture ecosystem, not only dampening returns but also weighing further on already- thin liquidity.

These dynamics reflect a market bifurcating at an accelerating pace. Experienced firms captured 90.9% of capital raised in Q1 2026, up from 73.7% for full-year 2025 and the highest share on record in this dataset. Established managers have always held a structural advantage in LP fundraising—brand and track record are durable edges—

but that share has now climbed to a level at which the fundraising market is practically closed to most emerging managers.

The squeeze extends beyond emerging managers. Even established firms with strong track records have faced LP resistance amid shifting regulatory frameworks, heightened geopolitical tensions, and overallocation to venture.

For emerging and first-time managers, conditions are considerably more severe—LP commitments remain scarce for all but those with a clear, differentiated edge.

Beneath the headline fundraising figure, fund sizes are contracting across most of the market. The median fund size fell to $15.3 million in Q1 2026 from $25 million in 2025—and with 25th percentile figures also declining while the 75th percentile holds flat, the

compression is broad, sparing only the top of the market. The emerging manager figures warrant a closer read: Not all managers classified as demerging represent new entrants to the industry—spinouts from established platforms and new vehicles launched by known investors are included in the data. Conviction Partners, founded by former Greylock partner Sarah Guo, closed two funds in 2025; Seligman Ventures, a first-time fund with

institutional lineage, closed in Q1 2026.

For managers that are genuinely new to the market, the threshold has risen materially—a differentiated strategy and a clear manager-strategy fit are now prerequisites, not advantages.

The data on the time to close funds reinforces the bifurcation in the fundraising market. The median time to close a US VC fund fell from 15 months in 2025 to eight months in Q1

2026—not because fundraising has become easier, but because the funds that are closing quickly are those with strong LP relationships and established reputations. Until distributions improve and LP appetite broadens, the structural divide between managers that can raise and those that cannot is unlikely to narrow.