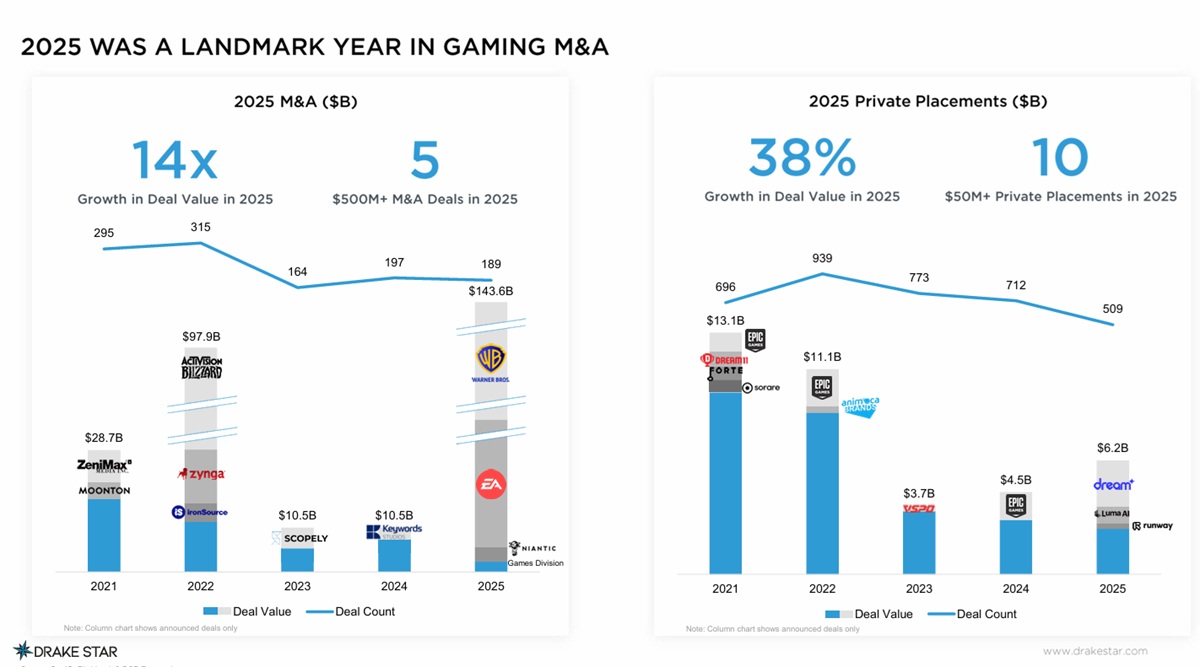

Gaming mergers and acquisitions (M&A) saw a landmark year thanks to two mega deals announced: the $55 billion Saudi-led leveraged buyout of Electronic Arts (EA) and Netflix’s $82.7 billion proposed acquisition of Warner Bros., including Warner Bros. Games.

In parallel, Paramount–Skydance launched a hostile $108.4 billion bid for Warner Bros. Discovery, underscoring the scale and intensity of consolidation across media, entertainment and gaming according to a report by Drake Star Partners.

Just as important than as the mega deals, gaming looks like it is set to advance on number of fronts in 2026 in terms of big game launches like Grand Theft Auto VI. There could also be more investments in game startups (driven by AI and mobile), new growth thanks to new user acquisition funds and more IPOs like Discord expected this year, said Michael Metzger, partner at Drake Star Partners, in an exclusive interview with GamesBeat.

“There’s obviously a lot of focus on tech and AI, but also the whole media landscape is really dramatically changing, like with over $160 billion in M&A deals. EA is being bought out and Netflix, which has not been acquisitive in years past, is trying to acquire Warner Bros.,” Metzger said. “The media landscape is just dramatically changing.”

The Drake Star Global Gaming Report 2025 is the firm’s sixth annual report, and it analyzed gaming and esports dealmaking in 2025 and outlined what to expect for 2026 and beyond.

Highlights

Gaming M&A activity reached $161 billion in disclosed value in 2025, largely driven by the EA and Warner Bros. mega deals.

As for the outcome of the big Warner Bros. deal, Metzger noted it will be a long process and Warner has already rejected the higher bid from Paramount.

“It seems at this point [Warner is] determined to move forward with Netflix, but I’m not sure what the regulatory hurdles will be,” Metzger said.

Other big deals

Other notable deals include the $3.5 billion acquisition of Niantic’s gaming business by Savvy Games Group and Scopely and the $800 million sale of Applovin’s gaming division to Tripledot. Netflix also acquired the avatar tech company Ready Player Me in Q4’25 (Drake Star was the exclusive financial adviser on the deal).

As far as M&A deals go, Europe came in at 70, North America at 68 and Asia at 50. He said he expects more Chinese game developers will become ore and more successful.

Strong private investments

Private financings were led by mobile and AI. Major mobile deals included VC/Blackstone’s $2.5 billion investment in Dream Games, alongside raises by Lingokids ($120 million), Good Job Games ($60 million), and Million Victories ($40 million).

Big AI investments

On the AI side, companies building AI world models with the potential to transform how games are made raised large rounds, including Luma AI ($900 million), Runway ($308 million), General Intuition ($134 million), and Decart ($100 million).

Numbers of deals are rising

Overall financing activity bottomed out in the second quarter of 2025 with 105 rounds, then rebounded strongly in the second half of the year, rising to 118 rounds in Q3 and 137 rounds in Q4.

The most active investors in 2025 included Play Ventures, Bitkraft and Griffin Gaming Partners among larger funds, while Impact46, Merak Capital, and Tirta were the leading seed-stage investors.

On the strategic side, Tencent, Krafton, and Smilegate drove the most activity, while Animoca, Arbitrum Gaming Ventures, and Spartan were the most active players in blockchain gaming.

It seemed to me that there were good and bad trends in these numbers. I guessed that investments in game studios were down, which is why we saw some game studios shut down, while investments in AI game tools were up.

Why game AI is hot and game studios are not?

Metzger said it was hard to tell whether there was a precise logic to the financing in Q4. But he said it was true that AI-related game deals went up and there was not much happening in Q4 for game studio investments.

“Game studios continue to be a very hard area for financing,” Metzger said. “I don’t necessarily see that changing.”

But he noted the rise of new user acquisition funds, (a couple of them backed by General Catalyst) which could invest in growth for game companies.

“That’s fundamentally a different business model,” he said. “VCs look for exits many years down the road. With the user-acquisition funds, it’s a much shorter cycle.”

He noted that the traditional game funds did not raise new rounds during the quarter, and it was welcome to have a larger fund like General Catalyst providing user-acquisition funding.

Game M&A slowed down in Q4 compared to Q3, but we still saw announcements of some of the biggest deals in history.

“What’s exciting is on the financing of private placements, we saw a bottoming out from a deal volume point of view. In Q2, we saw 105 deals, then we saw 118 in Q3 and then 137 as a nice step up in Q4,” Metzger said.

“It seems there’s more life in the early-stage startup ecosystem, at least from a funding point of view,” Metzger said.

Public deals coming back

The most notable public deals included Embracer’s spin-outs of Asmodee and Coffee Stain, and Ubisoft’s $1.25 billion raise from Tencent. Take-Two completed a $1.19 billion equity offering, and GameStop raised $3.75 billion in debt.

The Drake Star Gaming Index, which tracks the top 35 global gaming companies on an equal-weighted basis, rose 12% for the year, driven by strong performances from Unity (up 92%), Nexon (up $63%) and Netease (up 57%).

Given the rise in gaming stock prices, it makes sense that initial public offerings could come back. With public markets recovering, Drake Star anticipates IPO-ready gaming companies like Discord, Animoca Brands and MTG’s SimplePlay to go public this year.

“I think the environment for IPOs improved a lot, and we see a good amount of healthy IPOs. And I think that’s going to further increase this year,” Metzger said.

Outlook

Drake Star has a very positive outlook for the gaming & tech M&A market in 2026, following a year of several mega deals.

Key buyers to watch include PIF / Scopely, Netflix, Paramount, Tencent, KRAFTON, NCSoft, MTG, Take-Two, everplay, Sony, Keywords Studios / EQT, and Jagex / CVC. Private equity is expected to remain a major force in the market, with several publicly listed gaming companies increasingly viewed as attractive take-private opportunities.

Drake Star anticipates a healthy number of seed and early-stage financings, following the positive trend in the last quarters, along with select mid-to-late-stage rounds. Several new UA funds are expected to help scale mid-stage mobile studios. For financings, AI, UGC, tools and tech platforms are expected to continue to be shining stars.

“For 2026, we are generally bullish,” he said. “We are hoping that the M&A trend will conintue, but I think financing will continue to stay very difficult. Companies just need to be more focused on being cost efficient.”

The firm expects to finally see the launch of Grand Theft Auto VI as the biggest game release ever, now targeted for November 19, 2026. Other highly anticipated titles include Marvel’s Wolverine, Resident Evil: Requiem, Lords of the Fallen II, and 007: First Light.

“GTA VI is going to create a lot of excitement for the game industry,” Metzger said.