Gaming saw a 94% increase in venture funding during the first quarter of 2024, compared with the fourth quarter of 2023, according to a report by Konvoy Ventures. It’s not much, but it’s worth celebrating.

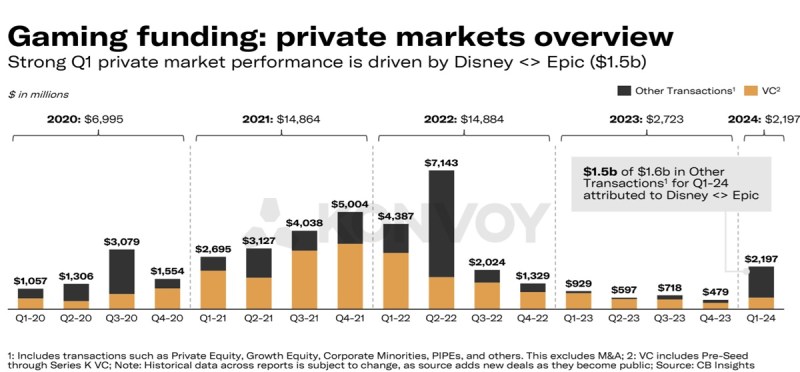

The first quarter saw strong private game market performance, mostly driven by Disney’s $1.5 billion investment in Epic Games to build a Disney gaming universe connected with Fortnite. After hitting bottom in the last quarter of 2023, the game investment market rose to about the same level it was close to a year ago. It also about the same in the number of deals as it was in Q4 2020.

It’s just an upward blip, driven by a few rare events, but it’s perhaps the best news the game industry has seen in a while. By comparison, Q4 funding was down 83% compared to a year ago. While the funding level in Q1 was down 28% compared to a year ago, it was up from Q4. That could be a turning point.

During the quarter, venture capital investments in games reached $594 million, with big deals driving the growth such as Build A Rocket Boy ($110 million) and Second Dinner ($100 million). The quarterly amount was up from $319 million in Q4 2023.

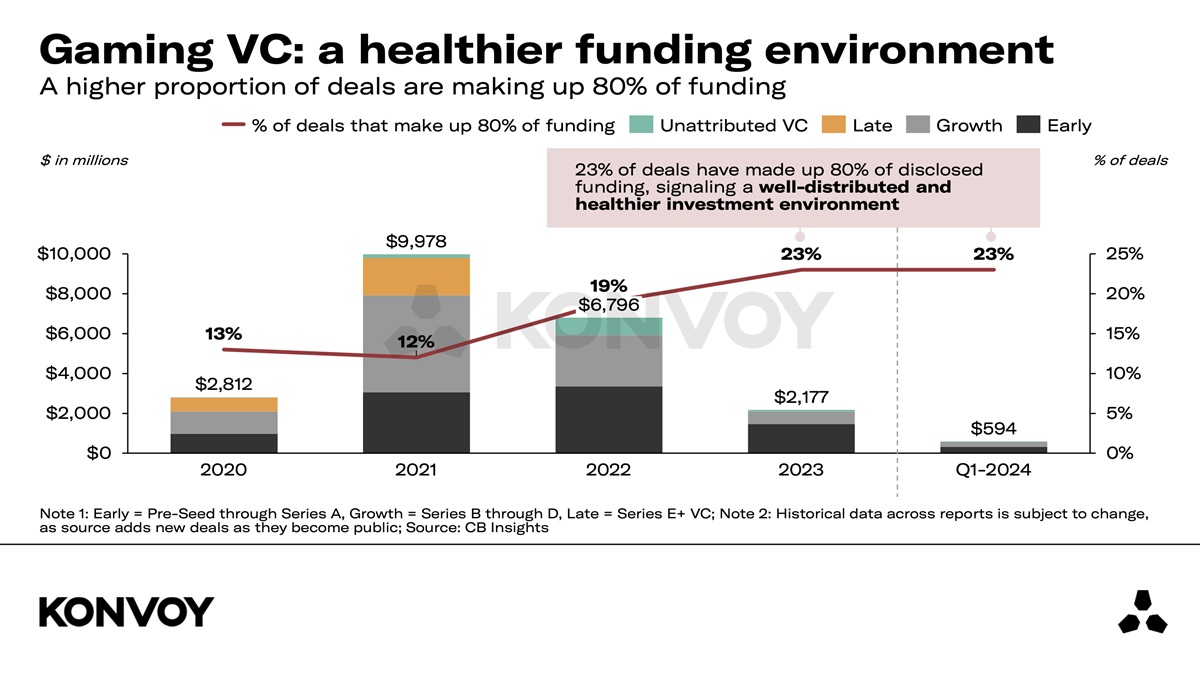

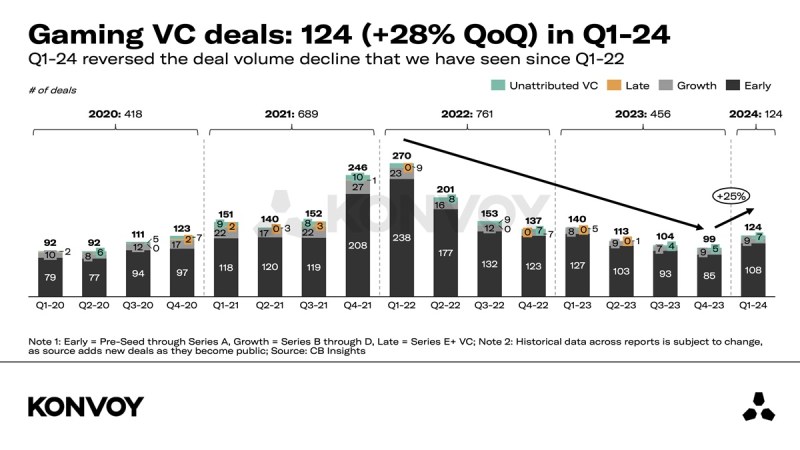

There were 124 companies that raised funds in Q1, up 28% from the previous quarter. About 23% of deals have made up 80% of disclosed funding, signaling a well-distributed and healthier investment environment.

By deal count, Q1 2024 saw a reversal of the deal volume decline that we have seen since Q3 2022.

This quarter, there was a large swing in deal funding back toward companies focused on

content development. The top 10 disclosed content deals totaled $333 million, which was more than three times to the amount of disclosed funding into the top 10 tech and platform companies. The top 10 game technology and platform companies raised $90 million in Q1 ( down 13% from the previous quarter).

“The investment climate around gaming has now turned a corner. We believe the worst of this correction cycle is behind us and 2024 and 2025 will showcase a healthy VC investment pace, a few selective M&A events, notable IPOs next year, and continued secular growth for the industry,” said Josh Chapman, managing partner at Konvoy, in a statement.

Gaming’s public financial snapshot

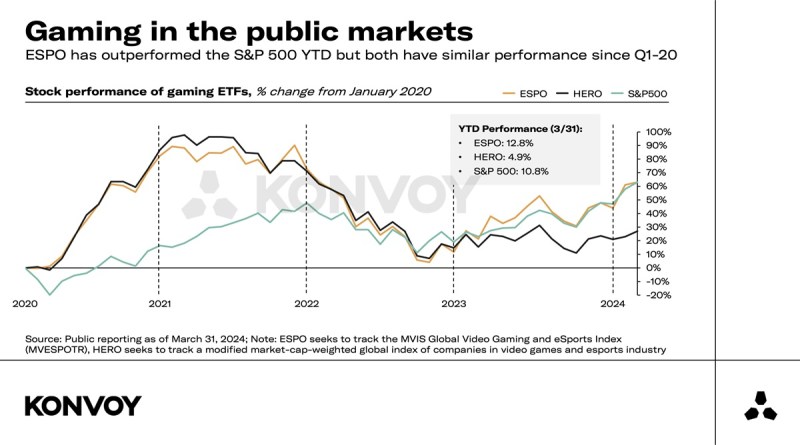

Overall, public reports from Newzoo and others predict that the size of the game market increased 2.9% in 2024 to $189.3 billion, compared to $184 billion a year ago. Public gaming electronic trading funds (ETFs) are up 4% to 12%, compared to 10.7% for the S&P 500 index. Konvoy and other public reports predict it will grow 3.5% a year to $225 billion in 2029. That’s a milder growth rate than we’ve seen before.

Early and growth venture capital has normalized to pre-COVID levels. Q1 2024 reversed the deal volume decline that we’ve seen since the second quarter of 2022, Konvoy said.

Public game companies hold about $35 billion in cash and equivalents, signaling a likely return to mergers and acquisitions. Tech giants with gaming divisions hold $267.2 billion in cash.

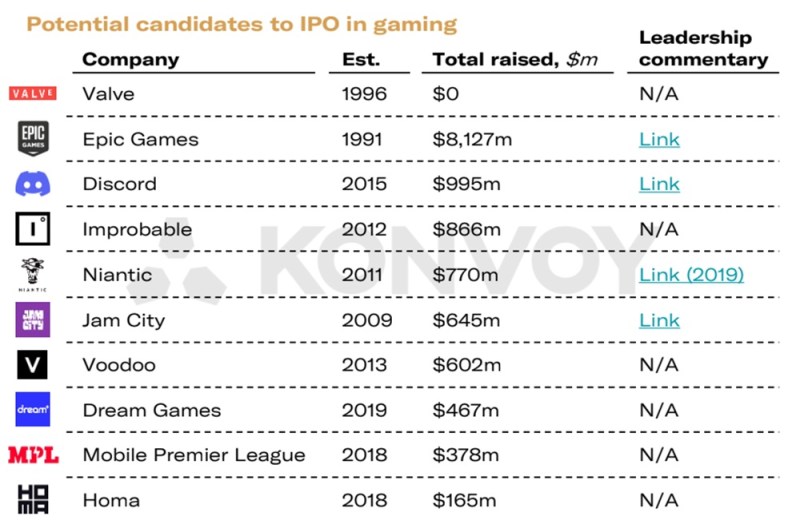

Q1 saw 40 transactions in gaming M&A. Some IPO candidates may be emerging, Konvoy said, compared to 41 in the previous quarter and 41 a year ago. In other news, the app stores are facing increasing scrutiny, and the U.S. is considering a ban on TikTok, the popular social platform used to make games more popular.

Konvoy said seven of the top 10 tech and platform deals in gaming involved companies in North America. The top 10 tech and platform funding totaled $89.6 million, down 13% from the previous quarter. Three of the top 10 tech and platform deals are building in the alternative game engine and operating system space (W4 Games via Godot, Playtron, and Jabali).

As for more game content VC deals, Konvoy said content was a large driver of disclosed deal activity this quarter. The top 10 content deals totaled $333 million, up 83% from $117.5 million in the previous quarter.

And this quarter, there were three growth-stage content deals with large disclosed deal volumes greater than $15 million.