The memory chip market has entered a “Hyper-Bull” phase, with current conditions eclipsing the historic 2018 peak, according to a report by Counterpoint Research.

If you’re looking for a culprit, look no further than the tech trend that has brought so much prosperity in the tech industry: demand for AI. Corporations in every industry have a hunger for AI chips, and that in turn creates demand for memory chips used in the same systems. Reporters at Nvidia’s CEO Q&A session at CES 2026, the big tech trade show in Las Vegas this weeked, peppered Jensen Huang with questions about memory prices. Huang said it was necessary for the ecosystem to plan for adequate supplies.

One of the consequences for the game industry is that the prices of game consoles and gaming PCs are higher than in the past, raising the prospect of price increases at a time when gaming was showing signs of recovery.

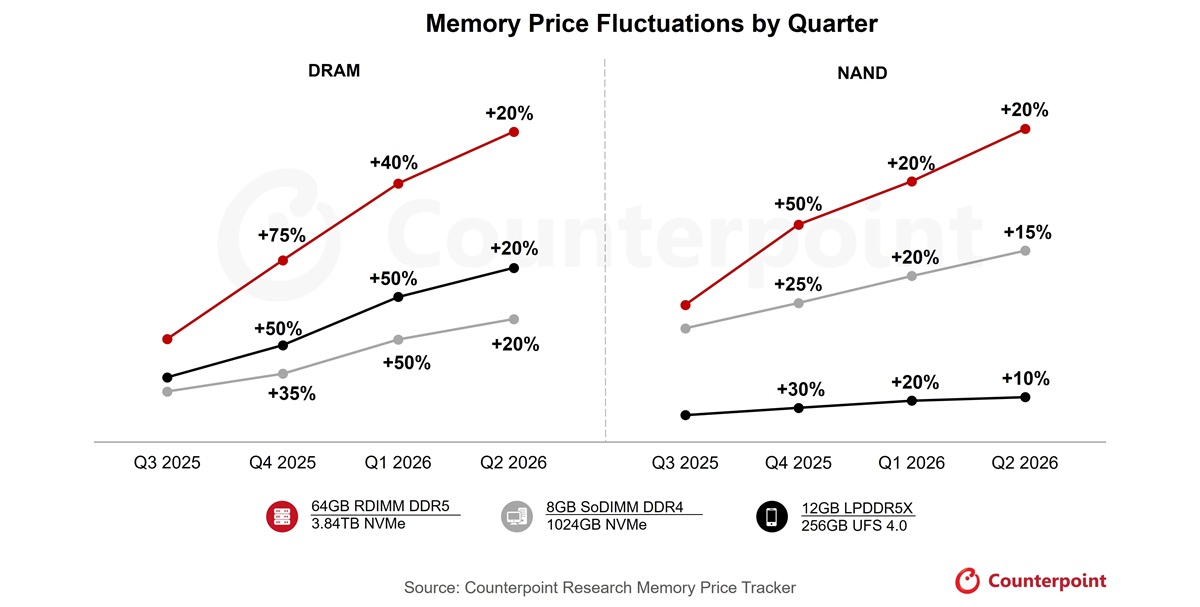

Supplier leverage is at an all-time high, driven by an insatiable demand for AI and server capacity. Memory prices are expected to surge 40%-50% in Q4 2025 and further increases of 40%-50% are expected in Q1 2026 and around 20% in Q2 2026.

Price Trajectory: Shattering Historical Records

Th report said 64GB RDIMM prices, which jumped from $255 in Q3 2025 to $450 in Q4 2025, are targeted to reach $700 by March 2026.

- The $1,000 Milestone: It would not be surprising if prices climbed to $1,000 this year, reaching $1.95 per Gb, which is almost double its 2018 high of $1.00 per Gb.

Structural shift in bill of material (BOM) costs

The rising cost of memory is fundamentally altering the BoM for hardware manufacturers:

- Smartphone Impact: Memory accounted for over 10% of the iPhone 17 Pro Max BoM in 2025, a massive leap from the 8% in the iPhone 12 Pro Max seen in 2020. For flagships configured with 16GB-24GB LPDDR5X RAM and 512GB-1TB UFS 4.0 storage, memory can represent 20% or more of total BoM with the current price hikes.

- Legacy Squeeze: Supply for older tech (LPDDR4, eMMC) is evaporating as giants like Samsung and SK hynix, and even Chinese players like CXMT, pivot production to high-margin Server DDR5.

Supply Outlook: Capex is Up, But Relief is Slow

- Demand-Supply Gap: DRAM (dynamic random access memory) production is projected to grow 24% YoY in 2026. Although capex is also rising, it will take time to meet demand.

For more details, please refer to Counterpoint Research Memory Monthly Pricing Tracker Report.