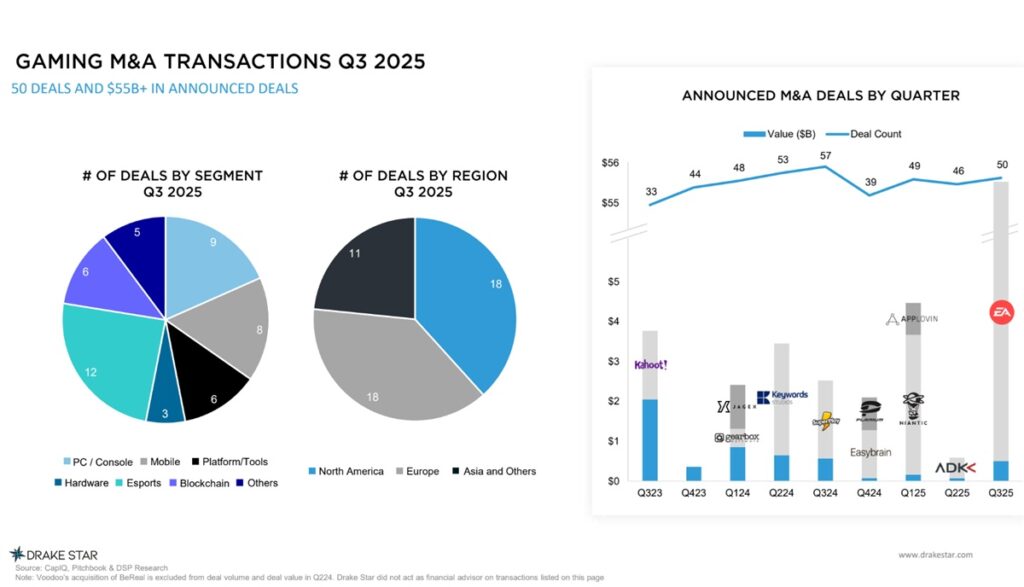

The Electronic Arts deal dominated news for Q3 acquisition deals, but overall M&A activity in Q3 reached 50 deals in the quarter — the highest level in four quarters.

Of course, EA’s announced $55 billion buyout by the Saudi Arabia’s PIF / Silver Lake /Affinity Partners consortium was the largest leveraged buyout in history, making the quarter a landmark one for gaming deals.

And after a year-long slowdown, Q3’25 saw a recovery with 113 private financing rounds, the first increase since Q1’24. Notable rounds included Lingokids ($120 million), Good Job Games ($60 million), Appcharge ($58 million), Million Victories ($40 million), Kong Studio ($36 million), and Distinct Possibility Studios ($31 million).

Interest in growth financings for mobile studios surged again in Q3, with five of the largest rounds going to mobile game developers.

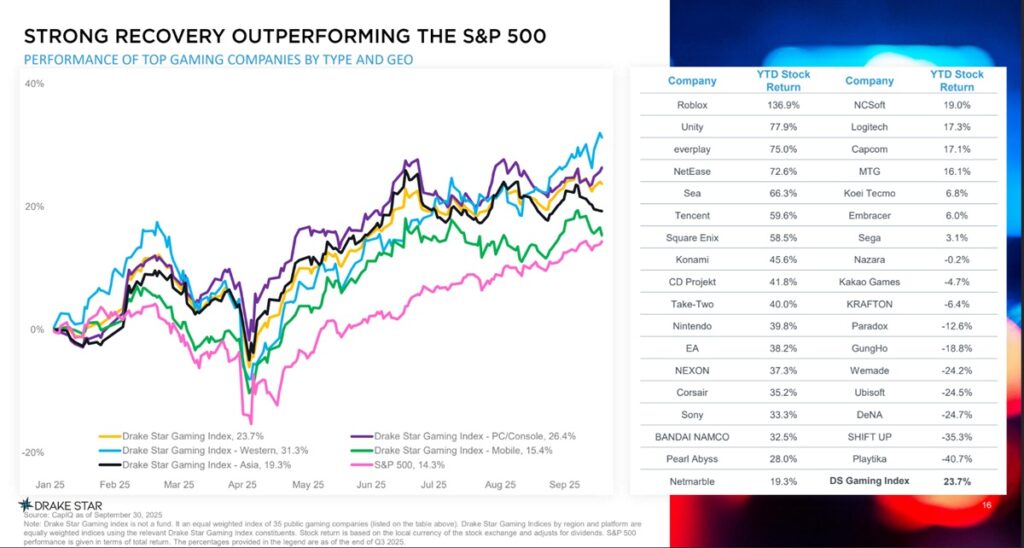

Western public gaming equities performed exceptionally well in Q3’25, with the Drake Star Western Gaming Index up 31.3% for the year. Top performers included Roblox (+136.9%), Unity (+77.9%), and Everplay (+75.0%). The broader Drake Star Index, tracking the top 35 global public gaming companies, is up 23.7% YTD, far outperforming the S&P 500’s 14.3% gain.

The other big deals overshadowed by EA include Aonic’s $250 million acquisition of Prime Insights, Krafton’s $96 million purchase of Eleventh Hour Games, DoubleDown’s $76 million deal for WHOW Games, and Impact46’s $53 million buyout of Kammelna.

“There are a lot of really great highlights this quarter,” said Michael Metzger, partner at Drake Star Partners, in an interview with GamesBeat. So first, obviously, a lot of people have been speculating around EA for the last years. It was rumors of the media companies acquiring it, or Amazon, and now this deal is happening with the PIF. It’s also the largest leveraged buyout ever in history. That makes this a landmark quarter.”

He added, “Then the second thing that was really encouraging is that the number of overall M&A deals increased increase ticked up to 50. We hit a low in Q4 last year, and went up to 49 last quarter, we went down to 46 and now we’re definitely in an uptick. And it’s the highest number within a year. And that’s maybe also an indication of the overall market.”

In terms of value, every deal was much smaller than the EA deal. But it’s still encouraging to financial people and those who are looking to make money by investing in game companies. This doesn’t exactly correlate to a recovery among game companies, but it’s a positive indicator for the overall value of the industry.

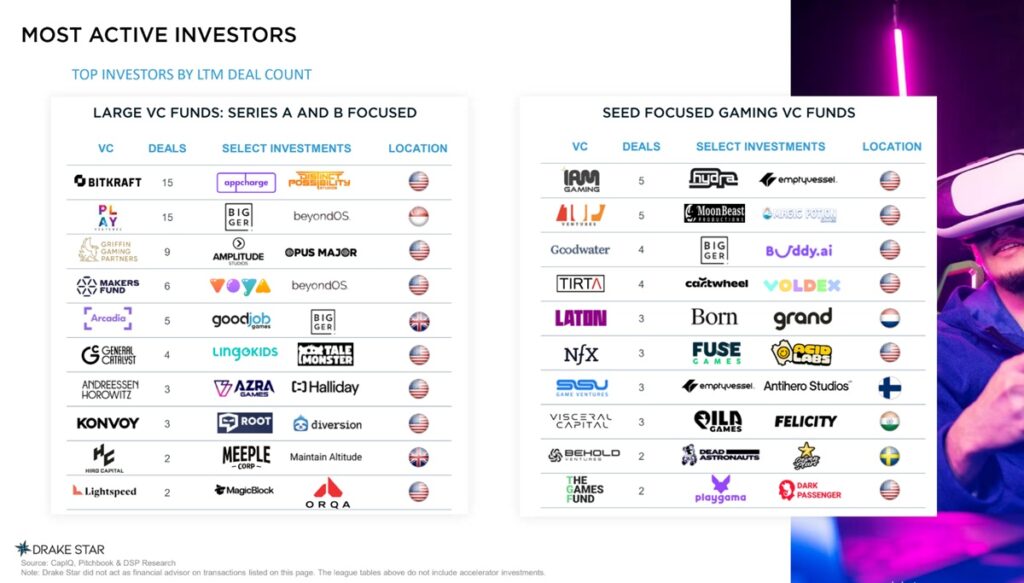

Most active investors over the past year included Bitkraft, Play Ventures, and Griffin Gaming Partners among larger funds, while 1AM Gaming, 1UP Ventures, and Goodwater were the leading seed-stage investors.

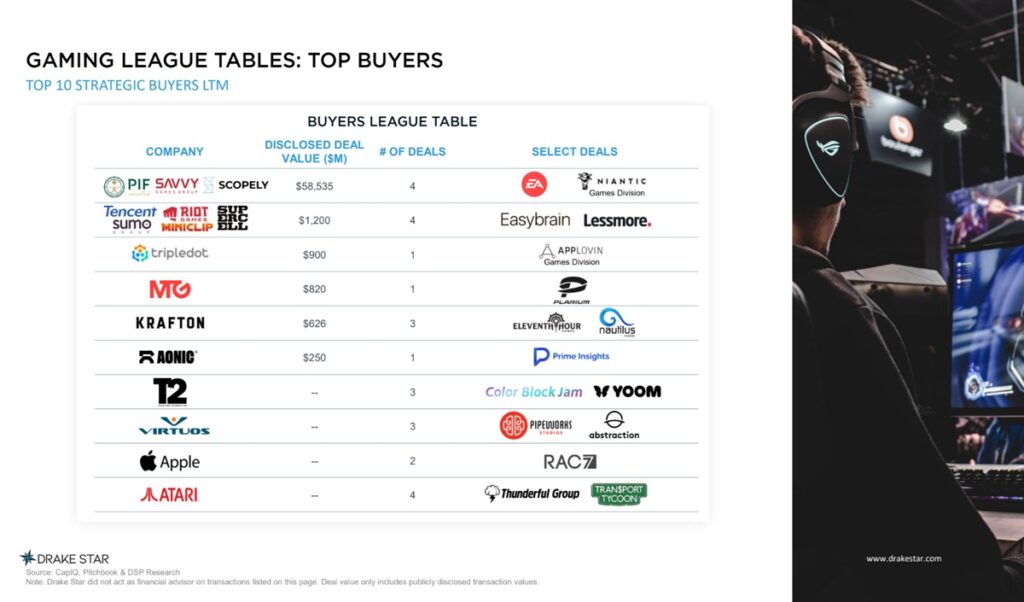

On the strategic side, Tencent, Krafton and Smilegate drove the most activity, while Animoca, Spartan, and Big Brain were the most active players in blockchain gaming.

Western public gaming equities performed exceptionally well in Q3’25, with the Drake Star Western Gaming Index up 31.3% for the year. Top performers included Roblox (+136.9%), Unity (+77.9%), and everplay (+75.0%). The broader Drake Star Index, tracking the top 35 global public gaming companies, is up 23.7% YTD, far outperforming the S&P 500’s 14.3% gain.

Light & Wonder, including its social casino arm SciPlay, announced the pricing of $1 billion in new debt financing. Azerion Group issued $260 million in new bonds, while Turtle Beach secured a $150 million senior credit facility.

The rebound in public gaming equities is paving the way for a surge in gaming M&A through 2026, as strategics are seizing the opportunity to capitalize on higher valuations and fuel bold inorganic growth to sustain investor momentum.

Drake Star Partners expects Coffee Stain Group to complete its IPO following the spin-off from Embracer by year-end and remain optimistic about the prospects for a strong Discord listing in 2026.

PE momentum in gaming shows no signs of slowing, with major funds eyeing public gaming companies for take-privates and top private studios becoming prime acquisition targets for growth-focused investors. With the resurgence of growth financing for mobile game studios in Q3’25, we are optimistic that funding activity across the gaming sector will continue gaining momentum in the coming quarters. AI and tools continue to be hot sectors.

“On the financing side, there are two things that were very positive” on the game investment side, he said. “We picked up from 110 to 113 for the number of [game investment] deals this quarter compared to last quarter,” Metzger said. “And this was really the first time we saw an uptick since Q1 2024. At least we’ve flattened out, and it’s going up again, which is great.”

Another positive was that if you look at the largest deal for the quarter, five of them were mobile studio deals, and that’s very encouraging because investment in studios has been challenging over the last year or two, Metzger said.

“Time will tell if this is a one-off thing this quarter, but it’s definitely encouraging that more money is flowing into game studios again, at least during the last quarter,” Metzger said.

He also noted that if you look year to date, the best-performing companies were mostly Western companies. The Western gaming index is up over 30%, with companies like Unity and Roblox leading the way.

“What I felt was also very encouraging is specifically the Western [public] companies are doing great,” Metzger said.

One of the things that Metzger expects to happen — without any insider knowledge — is that Discord will go public next year in an initial public offering. He has a very high confidence in that, given the company hired Humam Sakhnini, a former leader at Activision Blizzard, to be the Discord CEO.

Metzger said that a lot of VCs seemed to defocus on investing in studios. He also saw mobile game studio deals pick up and funding get steered into those deals. He thinks that the right investments in the right AI tools will be crucial for every company. And even for blockchain game companies, there are positive signs like growth on Telegram. Add to that drivers like Hollywood and games, and you can see how there’s optimism.

Of course, perhaps the biggest harm to gaming has come from layoffs in the industry in the last three years — 34,400 according to the Game Industry Layoff Tracker. It’s not clear whether improving financial performance and better deal numbers will turn into good news for game jobs. In fact, the use of AI could very well reduce the number of jobs.

I continue to hope that we can see a recovery with financial growth, job growth and technological innovation including AI that makes the industry better and leads to job growth rather than job elimination.