The second quarter was volatile for U.S. funding thanks to Donald Trump’s threat of tariffs, but venture exits showed signs of life by the end of Q2, according to a report by the National Venture Capital Association and Pitchbook.

Volatility and IPOs were Q2’s defining features. The quarter opened with a jolt from Liberation Day tariff announcements, plummeting the S&P 500 by over 10% in a few days and prompting many startups that had already filed to hit the brakes on going public, the report said.

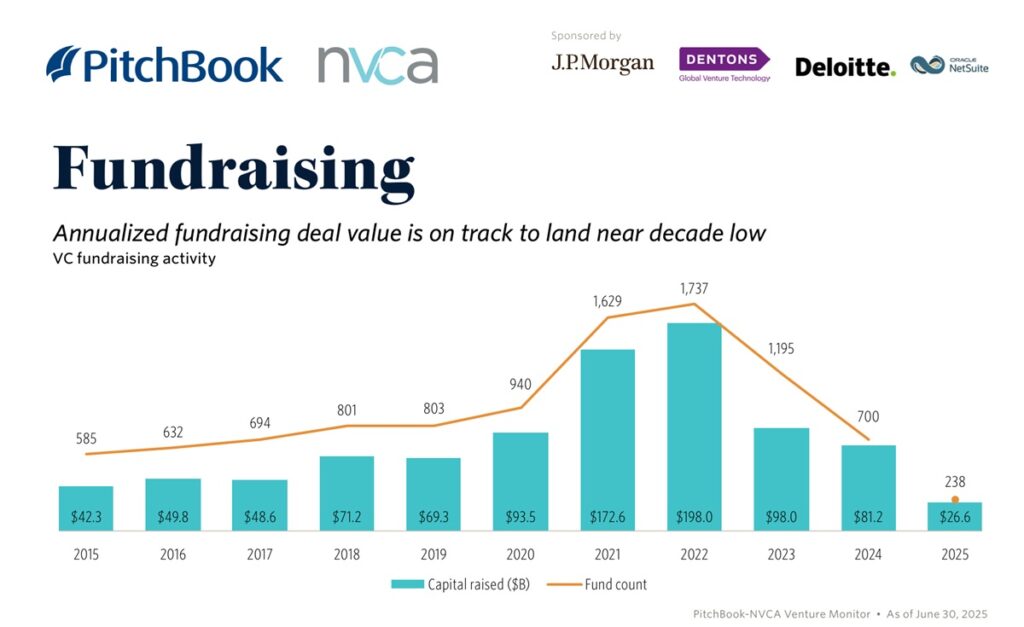

Fundraising was weak. During the first half of the year, $26.6 billion was raised across 238

funds, putting the annualized fundraising pace near the decade low.

In a partial reversal, the Trump administration soon issued a 90-day pause on tariffs, which helped steady public equities (only to unpause the tariffs this week).

In June, consumer sentiment recovered for the first time since December 2024 as consumers began adjusting to the tariff shock, even though they remain wary, Pitchbook said.

Despite the rocky start, there were a handful of high-profile IPOs and billion-dollar

M&A deals at the end of the quarter. Companies operating in AI, national security, defense tech, fintech, and crypto—sectors aligned with the administration’s priorities—are attracting disproportionately more investor interest, and this trend will likely continue throughout President Donald Trump’s term, the report said.

The liquidity outlook for the rest of 2025 is cautiously optimistic, marking a reset

rather than a full recovery. Unanswered questions about the pace and magnitude

of Federal Reserve rate cuts, unresolved global trade disputes, and geopolitical instability—particularly in the Middle East—create a risk environment that complicates company pricing, the report said.

This is not ideal in a market where down round IPOs have already become the norm, as

nearly every high-ticket public listing YTD has priced well below their peak private round valuations. Q2 did not have a surge in new IPO filings, revealing that many startups are prioritizing flexibility and optionality until some major macro questions are resolved.

In response, the secondary market has grown into a vital release valve for pent-up liquidity demand. Pitchbook’s current estimate of the U.S. VC direct secondary market ranges from $48.1 billion to $71.5 billion, with a midpoint of $60 billion.

However, the market size is modest compared with VC’s liquidity needs. $60 billion makes up less than 2% of total unicorn valuations and is comparable to Q2’s primary exit value of $67.7 billion. Trading volume continues to be concentrated among a narrow slice of elite startups that have the highest primary and secondary investor demand and, consequently, strong pricing confidence. For example, Hiive reported that just 20 startups accounted for 83.2% of trading volume in Q1, with the top five alone representing over half.

Still, multiple signs point to the continued expansion of secondaries as a structural pillar of the venture ecosystem, especially in a landscape where IPOs and M&A remain selective and lumpy. VC-specific secondary dry powder has more than doubled since 2022, and tender offers are becoming more common, providing companies price certainty and low cap table churn while still offering early employees and investors a path to partial liquidity.

VC investments decline 24.8% in Q2 from prior quarter

In Q2 2025, VC firms deployed $69.9 billion across an estimated 4,001 deals, representing a sharp 24.8% QoQ decline in deal value. This drop was due primarily to the lack of a $40

billion deal in Q2.

OpenAI’s deal from Q1 would alone represent roughly 57% of Q2’s aggregate. By contrast, Q2’s largest transaction was Scale AI’s $14.3 billion venture-growth round, which fell well short in scale, despite being the second-largest VC deal ever.

Fueled by select outsized Q1 deals and persistent AI momentum, venture growth-stage deal activity surged in H1 2025, with $83.9 billion deployed across an estimated 499 deals. On an annualized basis, this implies $167.8 billion in growth-stage venture capital deployment, far surpassing the 2021 peak of $91.6 billion and marking a potential record-setting year for this stage. While we do not expect another outlier deal on the same scale as the market continues to see outsized AI deals such as the Scale AI deal featuring Meta purchasing a 49% stake in the company in Q2.

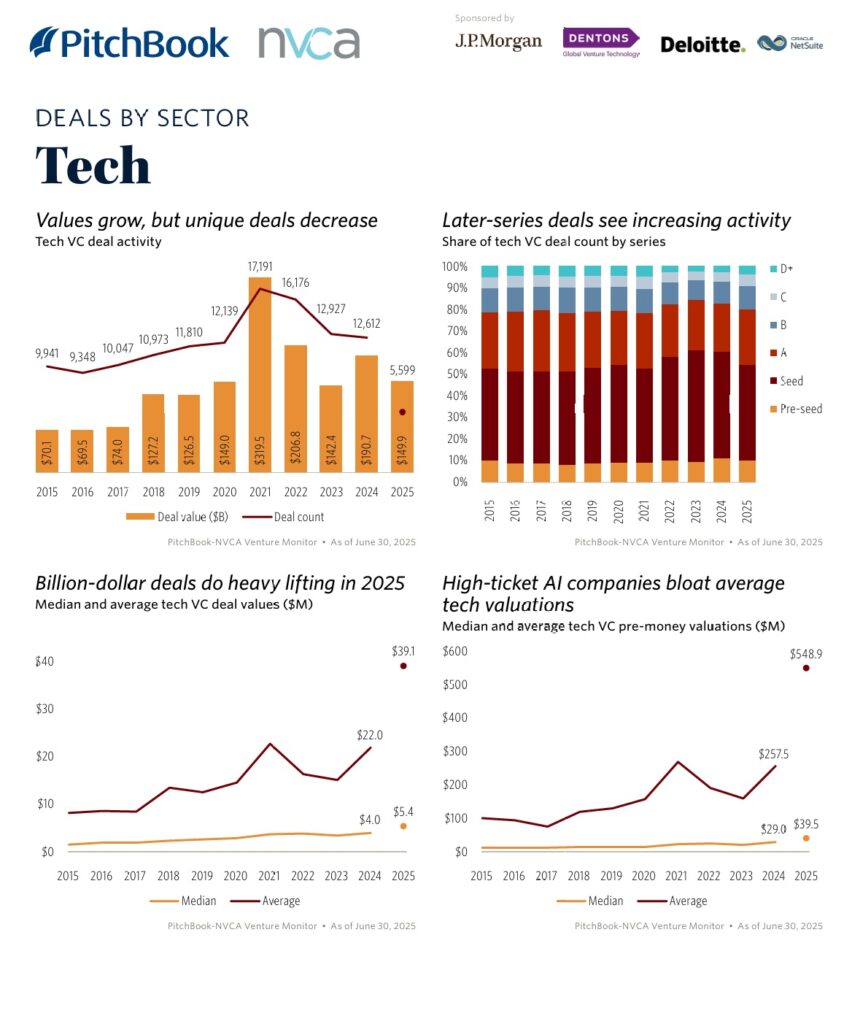

AI continues to dominate the upper end of the deal spectrum. In Q2, five AI deals topped $1 billion, including Scale AI, Safe Superintelligence, Thinking Machine Labs, Anduril, and Grammarly.

The sector represented 64.1% and 35.6% of H1 2025 deal value and count, respectively, highlighting sustained investor conviction.

Corporate investors are cautious

Corporate investors have continued to withdraw from VC. So far this year, only 1,112 corporate investors have closed a deal, just 35.7% of the 2022 high. These investors are also shifting their strategy, relying less on seed deals, which now account for just 24% of corporate venture capital (CVC) deals. This is in sharp contrast to 2022 when more than one-third of CVC deals were made at that stage, indicative of how the fast-paced, low-interest-rate environment shifted CVC activity. At this pace, 2025 could see the lowest

share of pre-seed/seed CVC deals since 2017, signaling a move toward less risk in the current environment.

Just 22% of deals include a CVC investor VC deal activity with CVC participation as a share of all VC deals Unsurprisingly, CVC activity remains focused on AI. While this trend may

mirror broader market movements, CVCs are motivated to invest in AI to avoid disruption. 42% of CVC deals have occurred into an AI company in 2025, up from 35% in 2024 and

Although corporate investment may not always lead to M&A, many corporate parents are leveraging AI to stay ahead of the curve. According to a recent McKinsey study, 78% of respondents reported their organization uses AI in at least one operation. Increased AI use can give CVC investors valuable insights into how a company might need AI or where

AI software could streamline costs. This might push active CVCs beyond their traditional investment areas to leverage that knowledge.

Crossover investors have largely stayed on the sidelines, despite their participation in many billion-dollar plus AI deals. Crossovers investors participated in only $11 billion worth of VC deals—the lowest total in six quarters and the third lowest since 2020.

The largest crossover round in Q2 was Neuralink’s $650 million investment. Outside of OpenAI and Anthropic’s deals this year, crossover funds have been absent from many

other large AI investments. Whereas corporates have leaned into these deals, crossovers may see them as too large for their taste and may still be reeling from the overinvestment and high valuations of 2021.

An interesting trend in the market is the shift of several investors to Crossovers participate in just $11 billion of deal value in Q2 VC deal activity with crossover investor participation by quarter registered investment advisors (RIAs).

Lightspeed’s move to RIA registration was completed in Q2, sparking many articles about this trend. Fewer than 30 traditional VC firms are RIAs, but this status offers broader opportunities.

A major benefit of RIA status in this market includes an increased ability to buy secondaries, both to acquire additional ownership stakes in top portfolio companies and add new companies to a portfolio. However, RIA managers do not all use their status the same way. For example, General Catalyst has added portfolio lending services and purchased a healthcare platform, which differs from Andreessen Horowitz’s broad platform of fund strategies. While this trend is worth noting, we believe it will stay limited to a small group of firms with large AUMs and a desire to diversify strategies to attract new LPs.

Still, the reporting requirements and additional costs may be too burdensome for most VC firms.

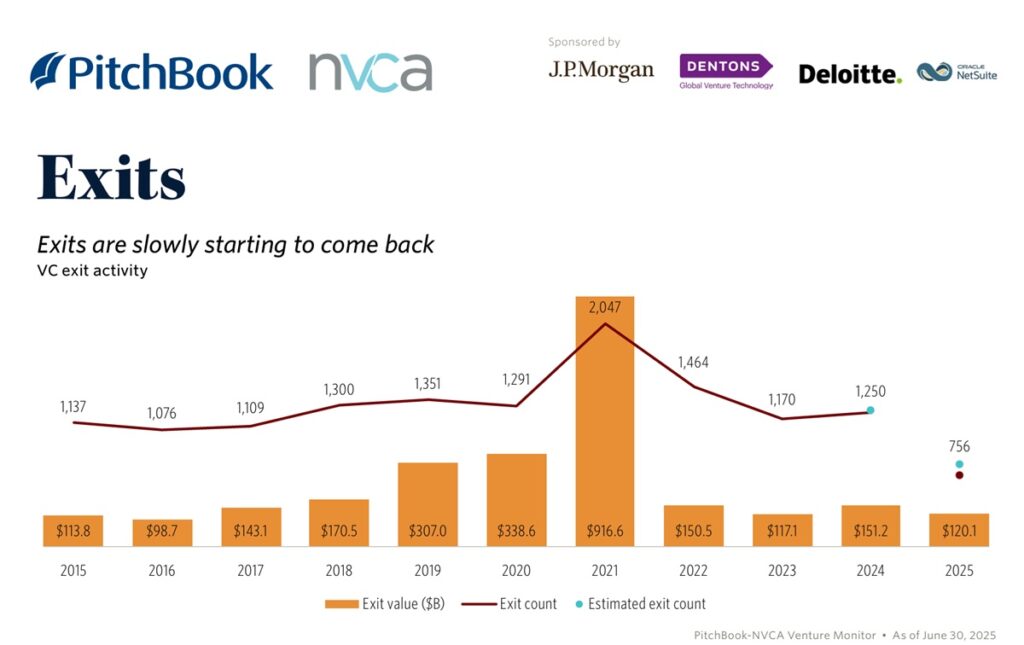

Exits continued to grow in Q2

Exit activity continued its ascent in Q2, generating $67.7 billion across 394 exits, which is the highest quarterly value since Q4 2021. Unlike Q1, when CoreWeave was the lone unicorn to go public, six companies with pre-money valuations over $1 billion completed their IPOs in Q2.

However, a deeper dive into the data reveals that down round IPOs have become the new normal. Rather than hold on to lofty valuations from pandemic-era highs, companies are prioritizing raising additional capital and providing liquidity for shareholders as venture’s exit drought extends past its third year.

In Q2, nearly every major listing debuted at significantly lower valuations than their highs. Notable examples include financial technology company Chime’s $9.1 billion IPO pre-money valuation versus its $25 billion peak, digital health company Hinge Health’s $2.3 billion valuation versus its Tariff tensions have dampened 2025’s exit outlook.

The greatest IPO beneficiaries are sectors like crypto and defense technology, which align with the Trump administration’s key policy themes.

It is no coincidence that the public markets have embraced Circle, the issuer of the second-largest stablecoin, USDC. As of June 30, 2025, Circle’s share price soared by over 117% from its first day of trading, while PresidentTrump continues to ease SEC oversight over crypto and the Guiding and defense and space technology company Voyager went public at a much larger valuation. Despite being unprofitable and reliant on government contracts, Voyager had an oversubscribed offering and a more than 80% share price increase on its first day of trading due to its ties with President Trump’s priorities of national security and technological sovereignty.

Despite the recent spike in public listings, it is still too early to claim that the IPO window has fully opened. A small cohort of companies—such as crypto firm Gemini, design software company Figma, AI chipmaker Cerebras, travel tech firm Navan, and fintech platform Wealthfront—have filed and are preparing to go public, but otherwise, there has not been a rush toward new filings. Top unicorns that have seemingly unquenchable private investor demand have few incentives to go public, and startups that are not focused on the administration’s key sectors may not garner sufficient public investor demand.

Acquisitions generated $32.2 billion across 229 closed transactions in Q2. Despite new leadership, the Federal Trade Commission has maintained its regulatory scrutiny, so Big Tech companies will likely continue their restrained pace of acquisitions.

Weak fundraising

U.S. VC fundraising remained subdued in H1 2025, as the prolonged liquidity crunch continued to weigh on LP sentiment. During the first half of the year, $26.6 billion was raised across 238 funds, putting the annualized fundraising pace near the decade low.

This figure would mark a 33.7% YoY decline in terms of capital raised, building on already

weak momentum from 2024.

Fund managers are taking significantly longer to close new vehicles. As of Q2 2025, the median time to close a U.S. VC fund stretched to 15.3 months, up from 12.6 months in 2024—the longest fundraising cycle in over a decade. This extended timeline underscores persistent LP reluctance to commit large sums due to the recent underperformance of the asset class and liquidity constraintsEmerging managers continued to face fundraising friction. However, their share of total capital raised stabilized, rising slightly to 23.1% in

Q2 2025, up from 20.6% in 2024. They also accounted for 45.0% of all funds closed, a mild decline of 2.7% from 2024, suggesting that while LP caution remains, support for newer GPs is no longer significantly deteriorating.

Meanwhile, first-time managers continue to grapple with severe headwinds amid a prolonged fundraising slowdown. In H1 2025, only $1.8 billion was raised across 44 funds,

setting annualized figures on track for a 32.1% decline in capital raised and a 40.5% drop in fund count YoY. Of the 11 first-time funds that closed at or above $50 million, many had founding team members who were spinouts from a pedigreed firm, including Sentinel Global I ($213.5 million), CIV One ($200 million), Cherryrock Capital I ($172 million), and Category Ventures I ($160 million). This trend reflects LPs’ continued preference for experience and track record, even when backing new firms.