SpaceX was the center of the VC universe in the first half of 2026. Elon Musk’s company saw a $1.7 trillion initial public offering in the largest IPO of all time, the NVCA/Pitchbook reported.

It was bigger than the next U.S. VC tech IPO by 17 times. Meanwhile, the announced $60 billion purchase of Cursor, a four-year-old coding startup, and the $250 billion merger with xAI in Q1 have made SpaceX the ultimate “kingmaker” in VC, said the Venture Monitor report from the National Venture Capital Association and Pitchbook.

But the wealth is concentrated. Overall, the market has still struggled to unlock IPOs, and few M&A deals outside of healthcare have been notable. The distributions that will be generated from the SpaceX IPO and eventually from the xAI and Cursor acquisitions will reach a broader investor base than normal for three companies because of SpaceX’s size and use of secondaries, but they do not signal a reopened liquidity market.

“SpaceX’s IPO was the first of three potential trillion-dollar listings by US VC-backed companies in 2026, and what many want to view as the opening of an IPO window,” said Nizar Tarhuni, Executive Vice President of Research & Market Intelligence at PitchBook, in a statement. “The scale of these companies is their differentiating factor, though, largely boxing out the rest of VC from public markets. The pipeline of companies in IPO registration remains low, and broad liquidity hasn’t yet returned, leaving exit value very concentrated through Q2, and very likely through the rest of 2026.”

Tarhuni added,”The same concentration is showing up in how capital gets raised: nearly half of all H1 capital commitments went to just three firms, and managers with track records pulled in more than 9 out of every 10 dollars deployed into venture funds. LPs aren’t spreading bets anymore — they’re consolidating around track records and brands, a response to five years of thin distributions. This year’s numbers will look like a recovery, but for most of the industry, it likely won’t feel like one.”

This is the likely story for the next couple of quarters. Anthropic and OpenAI have confidentially filed for IPOs. Those IPOs will likely add two more trillion-dollar exits by VC-backed companies. Along with the SpaceX IPO, these exits will generate more value than all US VC-backed exits since 2000.

That would more than make up for the lack of liquidity the market has endured over the past few years, but a large portion of investors and their LPs will not see distributions from those deals. These deals are the greatest example of the VC power law and a reminder that a few good exits do not make a great liquidity market, the report said.

“The second quarter reinforced an emerging trend: capital is flowing back into American innovation with real force,” said Bobby Franklin, President and CEO at NVCA, in a statement. “Investment activity is picking up, fundraising is improving, and there are early signs the IPO market is beginning to reopen. AI continues to drive much of the market’s momentum, even as investment and fundraising remain concentrated across a relatively small number of companies and funds. Healthier IPO and M&A markets will be critical to unlocking value, restoring liquidity, broadening access to capital, and supporting the next generation of American innovators across the country.”

What happens next?

The next-10-largest unicorns would generate $843 billion in exit value if they were ascribed a 40% step-up in valuation at IPO. However, none of those companies has positioned itself to be the next IPO. And the pipeline of unicorn tech IPOs is limited, at least when looking at those currently in registration.

Unicorn formation has not been limited, however, which has widened the gap between paper value creation and exit value realization. Despite the trillion-dollar IPOs, there remains a price imbalance between the public and private markets. That is a major reason why aging unicorns have not looked to go public. The continued availability of capital for private investments further exacerbates that imbalance, which lower interest rates will likely not alleviate. Public markets have remained stable, and indexes continue to reach new highs despite steady interest rates.

Proposed legislation to create a smoother transition between the private market and the public market is making its way through the approval process.

Increasing off-the-shelf offerings and limited reporting requirements are the main points of the legislation. These changes are a start, but they alone will likely not provide the incentive for high-growth, highly coveted companies to go public, at least for top startups.

The pitfalls of delayed liquidity are easily tracked through the 2021 cycle. Private capital was plentiful then, but so was liquidity with an abundance of SPACs, a high volume of IPOs, and

a strong M&A market. PitchBook’s Time to Exit Model shows that more companies completed new listings than were expected in 2019, 2020, and 2021, and by a significant margin.

However, the strong financing market of those years led to many more unicorns than ever before. And many of those companies opted instead to raise more private funding because it

was available, and probably at a higher valuation than an exit may have offered.

But now they are stuck in the private market with fewer options for liquidity. Those unable to raise capital since have seen a significant degradation in their value.

Liquidity benefits are not limited to SpaceX, Anthropic, and other large unicorns, but the returns are not headline-worthy. No matter the power-law dynamics, liquidity generated through midsize unicorns can still provide strong returns, and these companies are more akin to public market companies than the high-revenue, high-loss companies near the top of the market.

For investors not on the cap tables of the mega-unicorns, the timing of distributions from their portfolios is a key piece of information that can inform fund-reserve management and shape return expectations and the narrative to LPs.

If relaxed reporting regulations can restart the IPO pipeline, the benefits will have a wide reach. Price discovery for M&A will be enhanced, public comps will enrich secondary due diligence, and the liquidity generated will return money to LPs’ hands to recycle into new venture funds. Until then, liquidity remains tight as private market valuations balloon.

Dealmaking

In H1 2026, venture dollars continued to flow unevenly. Megadeals (rounds of $100 million or more) made up 87.5% of the $412.7 billion deployed. That half-year total already exceeds the 2025 full-year figure. Deals under $100 million drew $51.4 billion, and their share of value has compressed consistently and sharply over the years, from 43.8% in 2024 to 33.1% in 2025 and 12.5% this year, further evidence of how highly capital has concentrated at the top of the market.

Q2’s seven rounds at or above $1 billion—from Anthropic, Prometheus Industries, Anduril Industries, Baseten, MiRus, Kalshi, and Cognition—totaled $87.2 billion. Five were for AI companies, a sign of AI’s dominance among the largest rounds.

Anthropic’s $65 billion round marked a 157.1% pre-money valuation step-up to $900 billion from $350 billion three months earlier and lifted its post-money valuation to $965 billion, ahead of OpenAI’s.

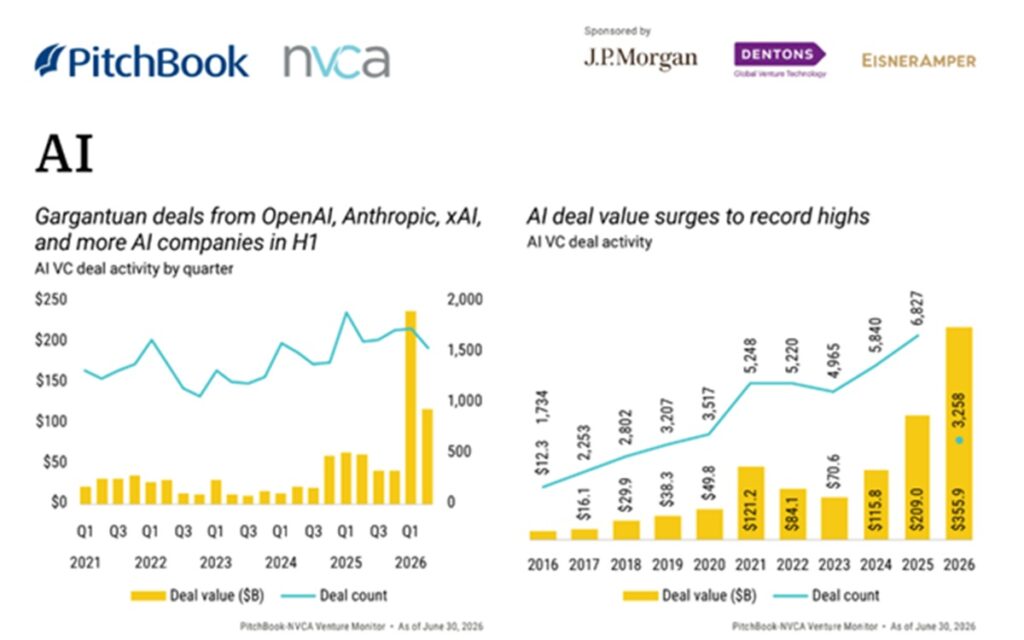

AI continued to define the venture market in H1 2026. The total AI deal value of $355.9 billion made up 86.0% of all venture dollars in the period. The companies driving the largest private

rounds are now moving toward public markets: OpenAI and Anthropic through confidential IPO filings, and xAI through its acquisition by SpaceX, which has listed.

The exits of these mega-round issuers thin the near-term pipeline of rounds at this scale, though they do not necessarily signal the end of outsized financings of tens of billions of dollars.

The next few quarters should surface the latest batch of companies able to command that kind of capital: names familiar to investors even if they do not yet carry the broad public recognition of Anthropic or OpenAI.

The AI race

AI maintained its dominance in the tech sector, an extension of a years-long trend. The shift is structural. AI has lowered the cost to build tech, with AI coding tools speeding up product

development and foundation models giving founders a base layer to develop upon without having to train their own models. The talent that can build at the frontier, though, is scarce and clustered on the West Coast, particularly the Bay Area, so if capital keeps following that talent, value creation in AI may stay geographically concentrated. First-time financings reached an estimated 5,674 deals in H1 2026, putting the year on pace to see more than 10,000 companies raising their first venture round, which would be a record.

Valuations have not just recovered from the 2022-to-2023 correction; they have pushed past their 2021 highs at every series. The median pre-money valuation more than doubled relative

to 2021 at pre-seed, seed, and Series D+. Among the middle stages, Series C came closest at 95%, followed by Series A at 89.9% and Series B at 83.3%.

The driver differs from that of the 2021 surge. Then, low rates and abundant liquidity lifted valuations broadly. Now, AI is the main force as expectations of fast revenue growth and market capture push the largest valuations higher and set comparables across stages. That reliance on a single theme raises the risk of a broad correction if AI growth or returns fall short. The power law of venture compounds the risk: Even if AI delivers, returns will concentrate in a

small number of winners, so funding a wide field at elevated prices leaves many of those entries exposed.

Many of the largest rounds are structured in tranches, or they fold in prior commitments. For instance, $15 billion of Anthropic’s $65 billion round was committed earlier, so the figure

cited in media headlines overstated the new money going into the company.

The post-money valuation, usually the highest mark in the round, is not the price every investor pays. That figure can be misleading: It reflects the top valuation in the round, not a common

entry price, and it can overstate the momentum behind a company. In a market this competitive, those marks can intensify the scramble to get onto the cap tables of the most sought-after AI companies.

The gap between private and public valuations remains an obstacle. Even with public indexes near record highs, listings have been limited, and several recent ones priced below their last private rounds. Investors across stages have questioned whether every company carrying a high valuation can reach the $1 billion+ outcome it implies.

High entry prices raise the bar for the growth and exits needed to justify them, and some of these companies will not clear it.

The next six months will test these bets. Companies that raised at elevated prices on compressed timelines need to show fast growth to justify their valuations and raise again, or they risk a down round. The mega-IPO of SpaceX and the pending ones from OpenAI and Anthropic will reveal whether public investors will validate private marks. The time between

rounds has compressed, especially for AI companies, so the margin for error is thin, and investors and their LPs will be watching for growth that meets elevated expectations.

Nontraditional investor activity has moved at a slower pace this year than in 2025 as a shrinking number of crossover funds, asset managers, and corporates are writing progressively

larger checks into the same narrow set of late-stage AI and infrastructure names.

Nontraditional investor deal value reached $379.4 billion in H1 2026, but much of it is attributable to a handful of companies, including OpenAI and Anthropic. This concentration is not so much concerning as it is reflective of the current state of the market, especially as liquidity pressure remains high for nontraditional investors.

SpaceX details

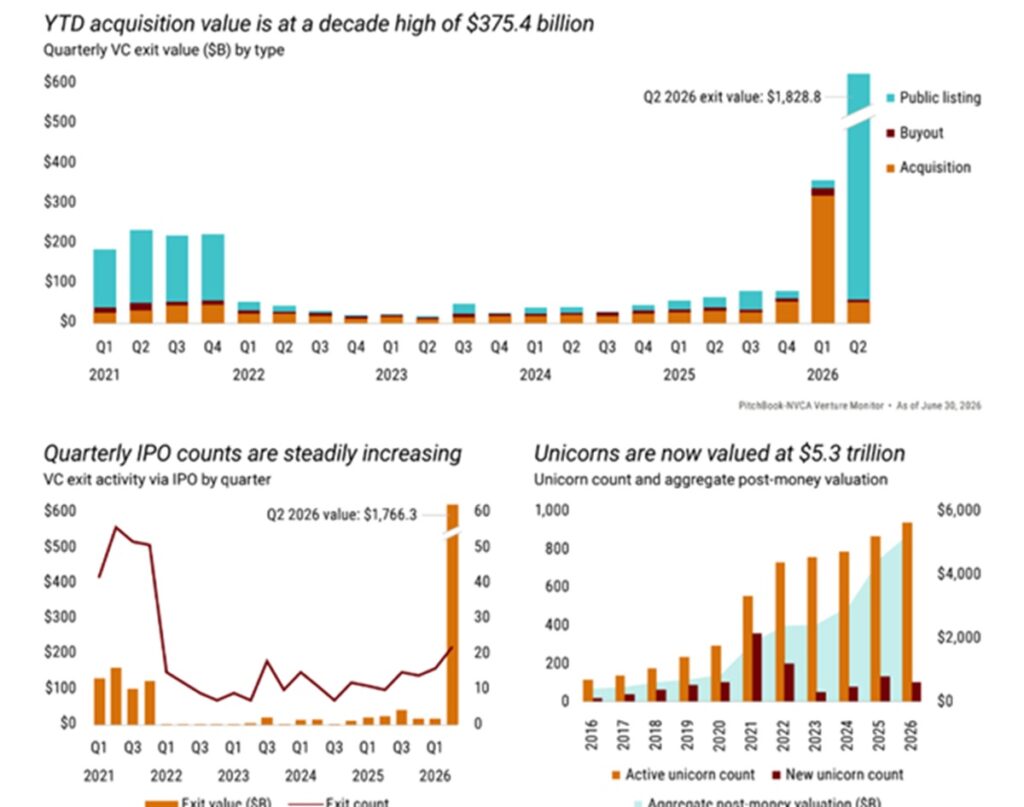

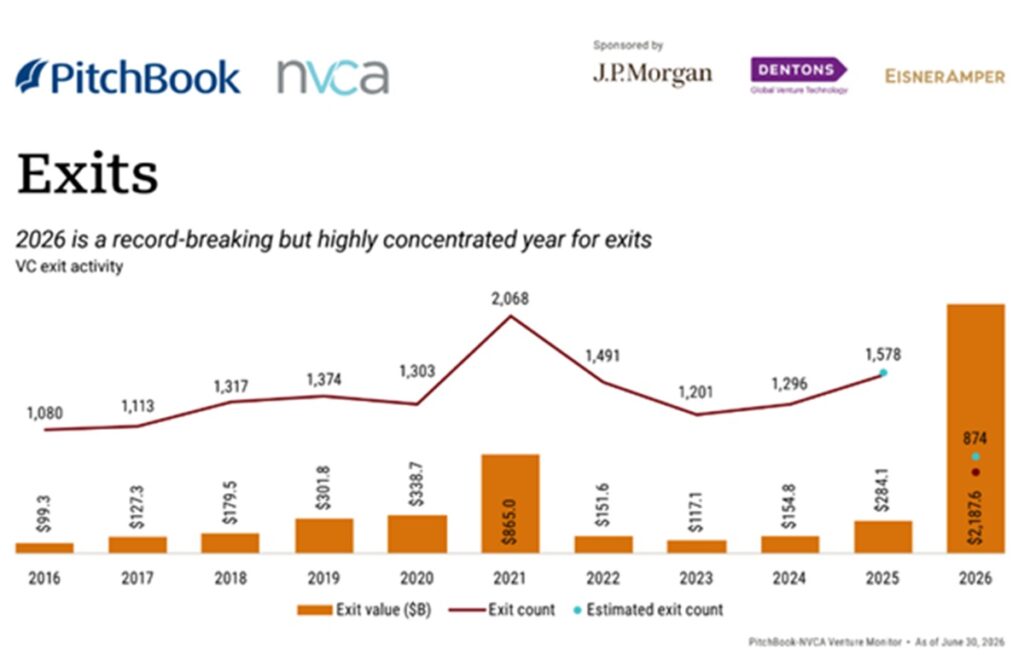

SpaceX has been the biggest story of H1 2026 for several reasons. In Q1, its acquisition of xAI totaled $250 billion, the largest acquisition of a VC-backed company ever. In Q2, SpaceX’s $1.7 trillion IPO generated more value than all exits in the past decade combined, raised $75 billion, and saw its market capitalization surge above $2 trillion in early trading. Plus, SpaceX’s $60 billion all-stock acquisition of Cursor will be the second-largest M&A of a VC-backed company, behind its acquisition of xAI.

However, without SpaceX, the quarter’s exit value would sit at a level more consistent with the constrained environment of recent years. The IPO window is cracking open, but only narrowly for certain sectors like AI, space technology, and crypto. There have been some promising listings, like Cerebras’ $34.3 billion IPO. The company canceled a 2025 public listing, raised $1 billion, and then completed its IPO at a valuation 5x higher than in the year prior.

Positioning itself as a competitor to Nvidia, Cerebras has ridden the wave of AI semiconductor

fervor. Still, it has not been able to hold its price. After opening at $385 per share, more than double its IPO price, it has steadily declined to below its IPO price at the time of this writing.

This decline continues the trend of highly valued tech companies seeing their stock prices fall in their first year as public companies. Of the 10 largest US tech IPOs, excluding Cerebras and

SpaceX, just three posted positive performance in their first year.

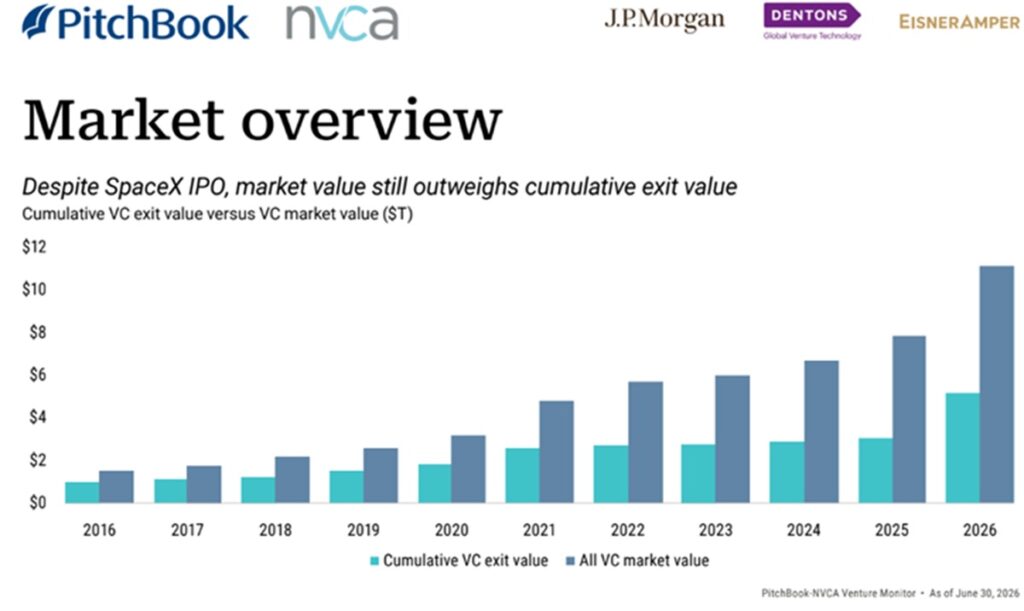

Beneath the record exit figures sits a backlog of trapped value that the SpaceX windfall did little to release.

Exits

In Q2, active unicorn counts reached a record 945, up 9.4% from year-end 2025, and aggregate unicorn value totaled $5.3 trillion. The distribution shortfall that has pressured LPs for years persists despite the quarter’s record exit value, because that value is overwhelmingly

concentrated in a single newly public company and has not yet flowed through to the broad base of funds and their investors.

Until the AI listing wave broadens into sustained liquidity across multiple companies, the gap between record paper value and realized distributions will remain the defining tension of the market.

With OpenAI and Anthropic confidentially filing, the second half of 2026 will test how much institutional capital remains once these AI giants absorb their share. The everyday exit paths remain thin for the broader market, and realistically, many typical venture-backed companies without a path to a marquee IPO may need to accept exit prices well below peak-era expectations.

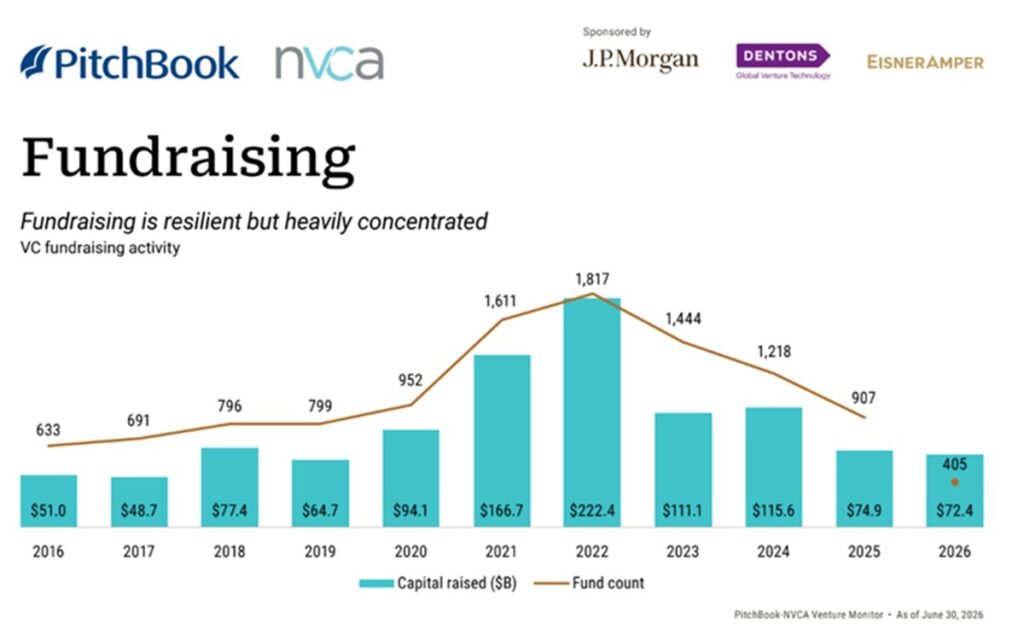

The split between resilient aggregate capital and a shrinking number of vehicles repeats the concentration theme that runs throughout this report.

In H1 2026, capital raised reached $72.4 billion across only 405 funds, just below the full-year 2025 total of $74.9 billion across more funds. LP dollars are still flowing, but they are reaching a smaller set of large established managers rather than the broader market. Fund formation, a leading indicator of the asset class’s future capacity, is contracting sharply. Over time, that

could concentrate pricing power among the managers holding the most dry powder, and because much of that capital is bound for AI, it deepens the market’s exposure to a single sector.

Capital is concentrating in large late-stage and multistage vehicles backing large later-stage AI companies. Funds of $1 billion or more raised $49.5 billion in H1 2026 across 16 vehicles, already well above the $27.5 billion those funds raised across 13 vehicles in all of 2025.

Thirteen firms have crossed $1 billion in commitments this year, and a few brand-name firms accounted for most of the capital raised. Andreessen Horowitz raised $14.2 billion across seven funds; Thrive Capital, $10 billion across two; and Founders Fund, $10.6 billion across two. Together those three firms took in $34.8 billion, or 48.1% of all venture capital raised in H1 2026. For these managers, paying up at the earliest stages is a choice the fund size can afford: A large vehicle can take a sizable position before valuations climb rather than competing for a sliver of a later, pricier round.

The shift toward established managers has come at the expense of emerging and first-time funds. Experienced firms raised $64.5 billion in H1 2026, against $7.9 billion for emerging

firms. With experienced firms taking 89.0% of capital, the greatest share in a decade, the market is showing a strong preference for track records in an uncertain environment. First-time

funds raised only $3.4 billion across 53 vehicles; the annualized value is well below the $11.4 billion they raised in all of 2025.

Many of the emerging and first-time managers still raising are spinout managers from pedigreed funds or are veteran operators and investors, so the contraction reflects LP caution

more than a shortage of credible new entrants. The pattern traces back to the distribution drought: With LPs receiving little cash back from existing commitments, they are concentrating

re-ups on their highest-conviction relationships. The longer-term cost is the narrowing of a manager base that has historically seeded the next generation of venture franchises, an

erosion that record megafund totals can obscure.

One operational metric underscores the same divide. The median time to close a VC fund fell sharply to 6.4 months in H1 2026 from 15.1 months in 2025. The faster pace is best read as

a signal of which funds are reaching a close. The vehicles closing today are disproportionately the well-positioned, established funds that LPs are eager to back, while much of the broader market that has historically taken longer to raise has slowed or stopped fundraising.

The path back to a broader market runs through liquidity, and that will take time. SpaceX has listed, and OpenAI and Anthropic are expected to follow, but lockup periods mean GPs cannot

sell into those listings right away, and share prices may move sharply by the time GPs are able to. Cash will not reach LPs until lockups expire and shares are sold, so the distributions that would free up new commitments are still a ways off. Until that cash flows back, the fundraising pattern is unlikely to shift, and capital should keep concentrating in the largest funds. That selectivity, visible in deals, exits, and investor participation, is the through line of H1 2026: a venture market setting records at the very top while contracting almost everywhere beneath it.