Mega initial public offerings could threaten smaller expected IPOs in 2026, based on an analysis of liquidity by analysis firm Pitchbook. The firm raised the simple question, “If these companies go public, is there enough liquidity for the rest of market?

SpaceX, OpenAI, and Anthropic are rumored to go public in 2026. Should that occur,

they would likely be the three largest VC-backed IPOs ever and could conceivably

create more value than all VC-backed IPOs since 2000 have collectively, Pitchbook said.

This would be a win for venture capital, a market that has been stranded in a liquidity crunch for several years. However, these returns would be relatively concentrated, with large portions of value being held by corporates and non-VC investors.

2026 has been seen as a year when the IPO market could bounce back. (Of course, the Iran war and rising oil prices could spoil that). After a rise in IPO activity in 2025 and the increase in unicorns going public, 2026 was expected to continue that momentum. Currently, only a few companies are in the registration process, and no major IPOs have been completed in the first two months of the year.

SpaceX is reported to be aiming to raise between $50 billion and $75 billion, and OpenAI and Anthropic could raise another $50 billion combined, which would be roughly as much as was raised by US VC-backed company IPOs over the past decade. With such large sums being raised by just a few listings, the potential lack of capital for less unique offerings should concern VCs, Pitchbook said.

Companies that completed IPOs in 2025 were met with a lack of enthusiasm, for the most part, post-listing, as many have traded lower since their listing. It is not uncommon for high-growth tech companies to trade lower through the first six months in the public market, but any selling pressure up until a lockup period expires for these mega IPOs could induce worry by VC-backed companies, as a volatile market would be less ideal for new listings.

Equity markets already must contend with unclear economic signals, as well as the Iran war, Pitchbook said. Further uncertainty due to poor listings by any of these companies could create a further freeze in VC-backed IPOs and lead to an extension of the weak liquidity climate that GPs and LPs already face.

Potential mega IPOs of 2026

If any of the potential IPOs of SpaceX, OpenAI, or Anthropic are completed in 2026, they

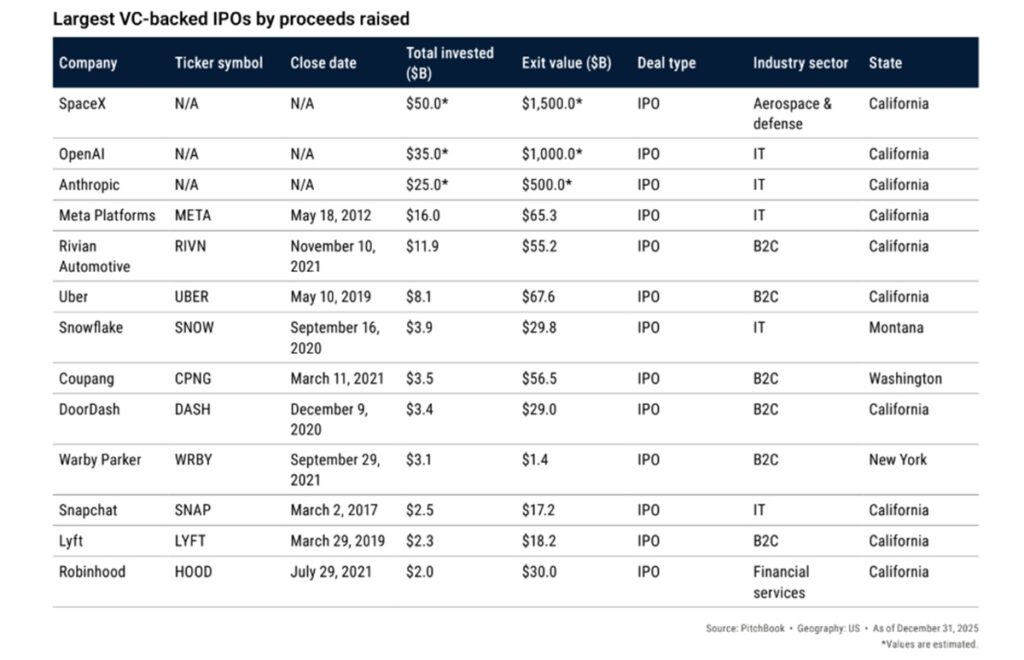

would be the largest US VC-backed tech IPO ever. Meta (previously Facebook) went public

at a valuation of $104 billion. Alibaba holds the record for the largest global tech IPO,

at $175 billion.

Each of the three companies is currently valued much higher than those valuations. SpaceX’s recent merger with xAI created a $1.25 trillion market value, while OpenAI and Anthropic have been valued at $840 billion and $330 billion, respectively— though soon after this note is published, one or more of those could change, Pitchbook said.

The considerable intrigue for these IPOs not only stems from their individual valuations

but also from the large number of companies still private and the lack of liquidity the US

VC market has endured since 2022. These IPOs would be significant for the market for

several reasons.

With these companies being the base of the AI market, OpenAI’s and Anthropic’s IPOs would further validate the enormous amount of capital flowing into the market if the listings are strong. All three companies would also add validation to the secondary markets, of which they have been able to generate a considerable amount of liquidity already for employees and early investors.

More importantly, strong listings could pull more companies into IPOs, unlocking billions of returns for investors. At least that is the hope.

It is also reasonable to believe that these company listings could add further challenges to

many companies looking to go public this year. VC is currently experiencing an extended

liquidity drought, not only because fewer companies have gone public in the past four

years compared with 2021 alone, but because M&A activity has been slow and value is

accumulating in late-stage private companies, Pitchbook said.

For many unicorns, that value has become stagnant, and the returns promised to LPs have not and likely will not be delivered. The attention that these mega IPOs take from the market could push a broadly open IPO window into 2027, which would add another year of stale fundraising for much of the market and further extend liquidity timelines, the analyst firm said.

Media attention is not the only thing these mega IPOs could absorb. IPO underwriting would be constrained by the amount these companies are able to raise. US VC-backed

IPOs raised a record $62.1 billion in 2021. Alibaba raised a record $22 billion when it was

listed in 2014, and was led by six lead underwriters. SpaceX is reportedly looking to raise

$50 billion itself, and along with OpenAI’s and Anthropic’s listings, they could together

easily push above $100 billion in proceeds.

The hope has been that 2026 could be a continuation of the IPO rebound for tech that started in 2025. Obviously, the total exit value created by even one of these companies

would be an enormous lift for aggregate VC returns. Those returns would be relatively

concentrated, but they would be much-needed drivers of total distributions and inject

positive sentiment back into the venture market.

What is at stake for the venture market?

What is at stake is a fair question that examines both why these companies choose to go

public and how it affects venture capital. It is undeniable that these listings will provide a

huge windfall for VC, Pitchbook said.

The past few years have been mediocre at best for VC-backed IPOs. Public equity investors have shifted their focus to other more reliable market sectors and strategies, including the Mag7 companies, which offer high-growth, liquid opportunities for exposure to the same technologies—especially AI—that investors often seek from VC-backed firms. This is particularly relevant for OpenAI and Anthropic, which compete directly with Google and are backed by significant investments from others like Microsoft.

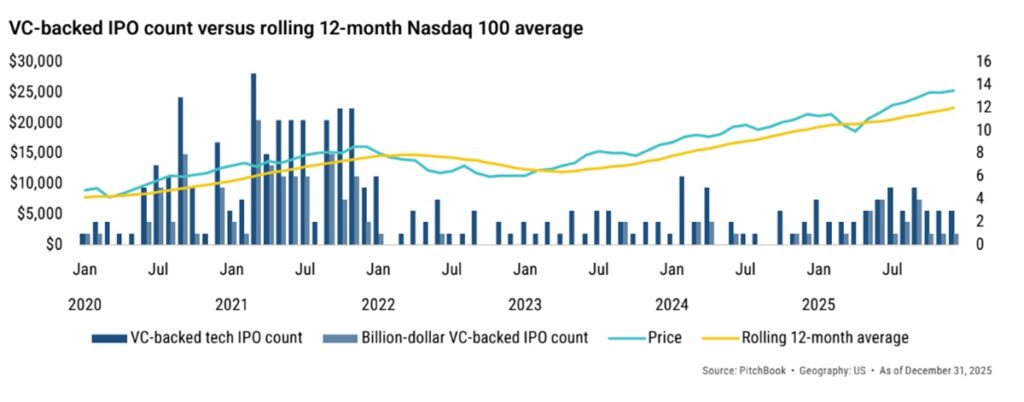

Unicorn age is defined as the years since a company first received VC funding. New completed listings have largely been met with underwhelming receptions, and none have been able to kickstart the development of a large pipeline. Some of the slow movement to go public has been due to outside factors, with both policy (tariffs) and geopolitical uncertainty reigning over the past couple of years.

These have complicated IPO timing, as well as pricing, as the uncertainty has added volatility to the market and compressed multiples for tech. In 2025, 17 unicorns went public, with 14 at lower valuations, and many traded lower after listing, Pitchbook said.

Pitchbook’s optimism about the VC-backed IPO market is notably more subdued than in some other market areas. The three mega companies might attract different support from the public markets than traditional VC-backed firms because of their uniqueness (SpaceX)

and their role as the foundation of the AI revolution (OpenAI and Anthropic). Most unicorns, however, are operating in a very different market reality.

Certainly, these three mega companies do not need to go public now to generate liquidity

for early investors or employees. Each has conducted multiple or semi-regular tender

offers, generating billions in liquidity for employees and early investors seeking an exit

to realize their long-held gains, Pitchbook said.

Each secondary sale has been at a significantly higher valuation, but there is eventually a ceiling to illiquid investments. That ceiling is not necessarily at a $1 trillion valuation, but keeping these companies private poses material risks to investors who bought stakes at such high private valuations.

For most other VC-backed unicorns, the IPO decision is more complex and driven more by

necessity than perfect timing. Many unicorns face inadequate liquidity from the secondary

market to return capital to investors and LPs. This pressure forces companies to help

investors realize gains they have been reporting. PitchBook Valuation Estimates shows

that at least 25% of unicorns have valuations below $1 billion.

The U.S. VC market has nearly reached $7 billion in aggregate value. More than $4 billion of that is in unicorns. Unlocking this value, specifically, is the most pressing need of VC.

Possible scenarios for the market to consider

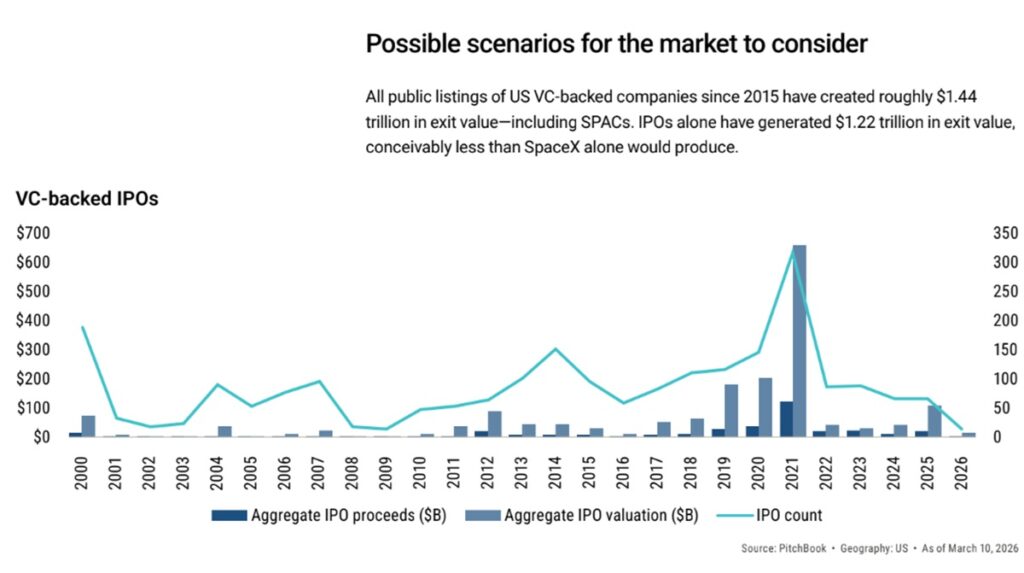

All public listings of US VC-backed companies since 2015 have created roughly $1.44

trillion in exit value—including SPACs. IPOs alone have generated $1.22 trillion in exit value, conceivably less than SpaceX alone would produce.

A benchmark to show just how much value these IPOs would generate is 2021. During

that year, $518 billion of exit value was created through new listings. That was spread

across 198 IPOs, which is the highest number of VC-backed listings during any year. 2021

was characterized by a significantly different market. The Federal Reserve cut rates to

the lowest level seen in a decade. The venture market churned out companies with high

revenue growth rates and listed them into public markets with high revenue multiples.

The S&P 500 returned 28.4% for the year, and 21 of 24 major global market indexes

were positive.

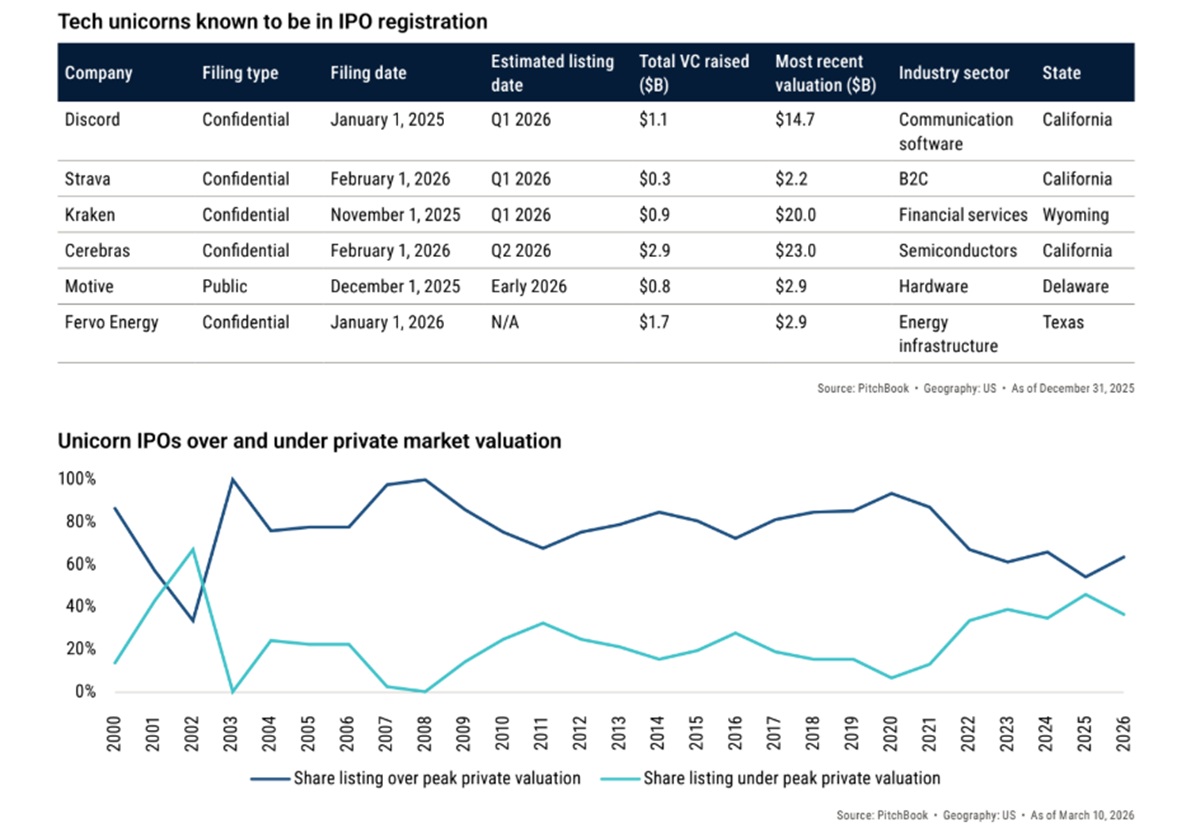

Currently, there is not a large pipeline of companies that have filed S-1s. Crypto exchange

Kraken has filed its S-1 confidentially, while Cerebras has refiled its papers confidentially

after postponing a previous IPO plan. Beyond that, Discord is rumored to be considering a

listing, and several healthcare and smaller tech companies have begun the IPO process.

However, the list is not long.

With SpaceX reportedly weighing a March confidential filing, our belief is that there will

not be much activity until the second half of 2026, possibly after a SpaceX IPO. Under

that assumption, potential scenarios for the market driven by the IPOs of SpaceX, OpenAI,

and Anthropic are crucial for the IPO recovery.

These mega IPOs could serve as catalysts, encouraging more companies to go public based on market reception. Conversely, negative scenarios are also possible: If these companies absorb the capital that would otherwise go to tech IPOs, or if poor market reception causes a further split between these companies and future listings, liquidity for investors could be delayed until 2027 or later, Pitchbook said.

Strong listings will likely benefit the market. There is some truth to the idea that most

companies going public will not be comparable to any of the three major firms. SpaceX

is less like the majority of VC-backed unicorns, so its real impact on the venture market

might lean more toward boosting positive sentiment for GPs and LPs—showing that

returns for these highly valued companies can be realized—rather than signaling that

public market investors are back to seeking risk in tech companies.

At a rumored $1.5 trillion valuation, the IPO would yield an over 10x return for investors

from the 2023 round that valued the company at $137 billion. Nearly 50 investors are

listed as participants in that round alone. While a single company will not fully revitalize

fundraising, the distributions from SpaceX’s IPO would be broader than a typical major

listing. The fact that these 50 investors invested at such high valuations and are still seeing

10x returns is remarkable.

For OpenAI and Anthropic, market validation of AI would likely increase, potentially

catalyzing IPOs and boosting investment in AI startups.

Though these companies are much more highly valued than other AI unicorns, they often

form the core of the current venture market. Strong IPOs and sustained post-listing support would signal several things: first, that public market investors are willing to back

risky, unprofitable startups. Even if these companies do not fit the traditional startup

mold, they are still losing money with high burn rates, Pitchbook said.

OpenAI’s $110 billion fundraising would only last about five years at current spending levels—which are expected to grow.

Suddenly, a company going public with only $1 billion in annual losses would seem trivial.

Second, it would reassure VC investors that their push into AI is justified. By maintaining

optimism about IPO prospects, this sentiment could encourage billions in additional investment into late-stage companies, increasing marketing spend and governance

preparations for a public listing.

The optimism wave

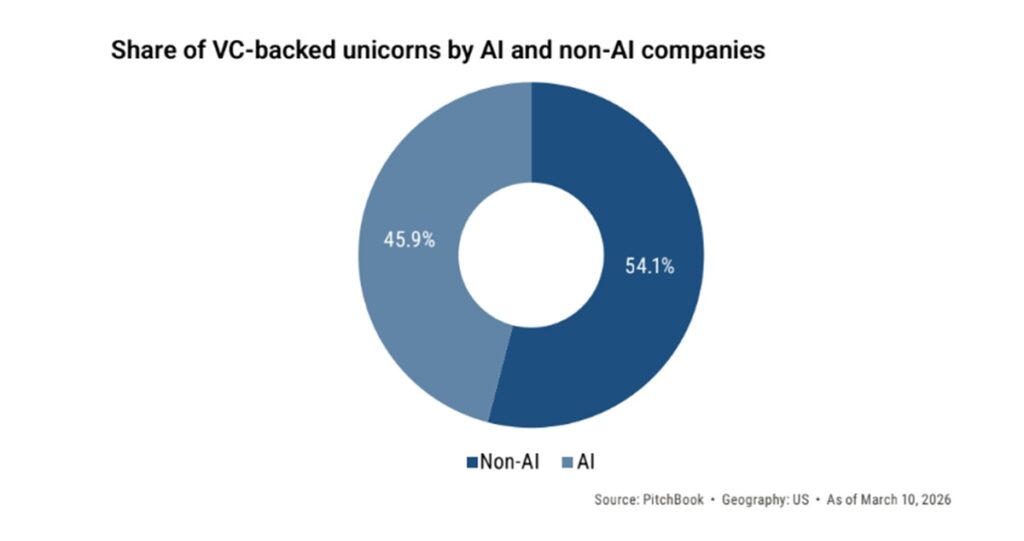

Currently, 30% of VC-backed unicorns are AI-native or AI-adjacent. Two AI leaders

receiving strong market support could provide the liquidity boost that the market needs.

Tech has been riding a wave of optimism.

The few companies in the registration process could also help trigger a rush of filings.

Beyond these, there are rumors of IPOs. If Databricks releases financials to compare

favorably with Snowflake, it would suggest that it is waiting patiently for its opportunity to

list—possibly to see how OpenAI and Anthropic fare.

Strong public market support for such high valuations would also help stabilize overall

market pricing, easing some of the pressure on private market valuations that have caused steep discounts for many unicorns in recent years. Venture market prices have risen significantly recently, largely driven by AI, Pitchbook said.

A challenge for the market that could arise from a boosted pipeline and heavy allocation

to these companies is systemic underpricing for the rest of the IPOs. First day pops are already celebrated by the market, but they are essentially money left on the table by listing companies. For unicorns needing capital to fuel growth, this can be problematic.

Alongside the question of “why go public?”, the need for liquidity for more recent investors

is a major issue these companies will all face. Secondary sales have eased liquidity

needs for early investors and employees, but realizing returns for investors holding

shares valued at hundreds of billions of dollars (either through primary or secondary

sales) remains limited.

For SpaceX, OpenAI, and Anthropic, going public provides liquidity for late investors taking on higher-than-normal risks by investing in illiquid shares. Any selling pressure on the stock before the lockup period ends could increase volatility when it expires, typically after six months. VC-backed companies that go public often do not perform well immediately, Pitchbook said.

Mechanically, this may not be much different from the large unicorn IPOs of the past.

Alibaba’s performance over its first year post-listing was down 40% from its debut price,

returning roughly to its IPO price. Meta and Uber both experienced a similar decline in their early months as a public company.

The most recent large unicorn IPO, Figma, is currently trading below its IPO price. What those companies lacked was a trillion-dollar valuation or anything close to it. They also did not carry the weight of VC market liquidity.

It is reasonable to think that mega IPOs would get strong allocation, keep their valuation

high, and possibly see a surge during their debut days. Private markets have not lacked

capital for them. However, their post-IPO performance is more uncertain. How many

buyers will there be at a $1 trillion valuation with financials that look quite different from

other companies in that valuation range? Will retail investor enthusiasm outweigh the

liquidity needs of institutional investors?

Generally, for VC-backed IPOs and even tech IPOs, there has not been a strong correlation

with volatility as expected. Sharp spikes in volatility tend to delay or slow listings, but on a

monthly average, volatility does not significantly impact the number of companies going public. Using a rolling 12-month VIX average, data suggests that longer periods of lower

volatility tend to increase listing activity. If market volatility picks up—perhaps because

investors rotate holdings or indexes rebalance into large companies with high volatility, low floats, and high multiples—the IPO pipeline might slow, waiting for market conditions

to stabilize.

A worst-case scenario for IPOs would be poor reception by the public markets. It is

worth examining current narratives around these companies. SpaceX likely has a better

reputation and a business model that is less typical of most unicorns or companies in

general. Its long-term vision may overshadow immediate concerns, Pitchbook said.

Anthropic’s Department of War challenge

In contrast, Anthropic has become controversial due to its reluctance to allow the Department of War to use its AI, leading to canceled government contracts and complications for defense contractors.

Until its S-1 is filed and made public, it is hard to gauge how much that will impact the company’s revenue and growth prospects. Although the Claude app quickly became the most downloaded on the Apple App Store, Anthropic’s core business relies on enterprise retention. Meanwhile, OpenAI has been capital inefficient, raising $64 billion to generate about $20 billion in annual recurring revenue and approximately $13.3 billion in 2025 revenue. This $64 billion does not include its recent $110 billion raise, which would not affect past revenues. OpenAI’s losses exceeded $6 billion in 2025, and its total expected burn by the time it becomes profitable could surpass $100 billion.

Looking at potential fallout from poor IPOs, WeWork offers a useful example. When filing

its S-1 in 2019, it was the most valuable private company, at around $40 billion. Its poorly

communicated vision, weak financial metrics, and high debt led to the cancellation of the

IPO and sparked a shift toward prioritizing profitability.

Over the next few months, IPO activity slowed to a halt, even during a year that produced the second-highest amount of exit value through US IPOs ever. WeWork’s canceled IPO occurred in September 2019, when just a couple of months later, concerns about COVID-19 began affecting markets—a caveat to be noted.

WeWork’s fall from grace temporarily shifted the venture market rhetoric. The 2019

unicorn of unicorns faced a tough decline, damaging the idea of mega IPOs. When interest rates dropped to near zero and the COVID-19 economy pushed stocks to new heights,

valuations recovered. However, this was a poor sign for VC-backed companies and the

tech sector overall.

Market volatility caused by mega listings—or worse, lack of investor enthusiasm—would, at best, restrict IPOs to only mega offerings. At worst, it could delay or completely push out potential listings for VC-backed firms, Pitchbook said.

Outlook

OpenAI, Anthropic, and SpaceX are not the only potential mega IPOs in the pipeline; they

are simply the most valuable companies currently. Databricks, Stripe, ByteDance, and

Anduril could go public at or above $100 billion. These companies, however, would not

have nearly the same impact on the market as the first three, even if their IPOs perform

exceptionally well. The extended private market for these companies and many other

unicorns has created liquidity challenges should an IPO window open.

The war involving the US, Israel, and Iran threatens a relatively stable market and, at

minimum, increases uncertainty and the temptation for companies to delay going public.

Although markets have not experienced a quick shock due to the war, it is definitely a

factor that could influence VC-backed listings. Defense tech company Anduril recently

raised $4 billion in private funding, showing that IPOs are not necessarily imminent for

VC’s largest firms and that capital remains available in private markets for companies

beyond large language models, Pitchbook said.

Without these companies going public, our outlook for 2026 IPOs is more cautious. Positive progress from unicorns was made in 2025, with 17 companies completing IPOs.

Although the 48 total company offerings were just four more than in 2024 and below the

average of roughly 70 over the past 20 years, it indicates that companies are still seeking

liquidity for investors. Challenges such as high private market valuations and strong

returns from established businesses remain in place in 2026.

Another area to watch is how these companies going public will impact the secondary

market for private shares. Our estimate is heavily weighted toward these companies

because of the cadence they provide for liquidity to employees and investors, as well as

the size of their valuation. Our expectation for the secondary market is that a large gap

in the market will open, but it will be filled by increased secondary activity if the markets

react favorably and the share prices hold. Volatility in these companies and a significant

decline in their prices could cause problems for secondary markets, which have supported

liquidity for investors in the highest-valued companies.

Whether SpaceX, OpenAI, Anthropic, or other major IPOs occur in 2026 or later, the coming years could be transformative for venture market returns. Investors, founders, and often employees will likely see significant windfalls from these listings, which could reignite VC fundraising due to distributions and renewed interest from LPs.

It is safe to say that these will be the most impactful IPO and liquidity events for the

venture market ever, Pitchbook concluded.