Game financing deals and M&A activity were strong in the second quarter of 2026, according to a quarterly report by Drake Star Partners.

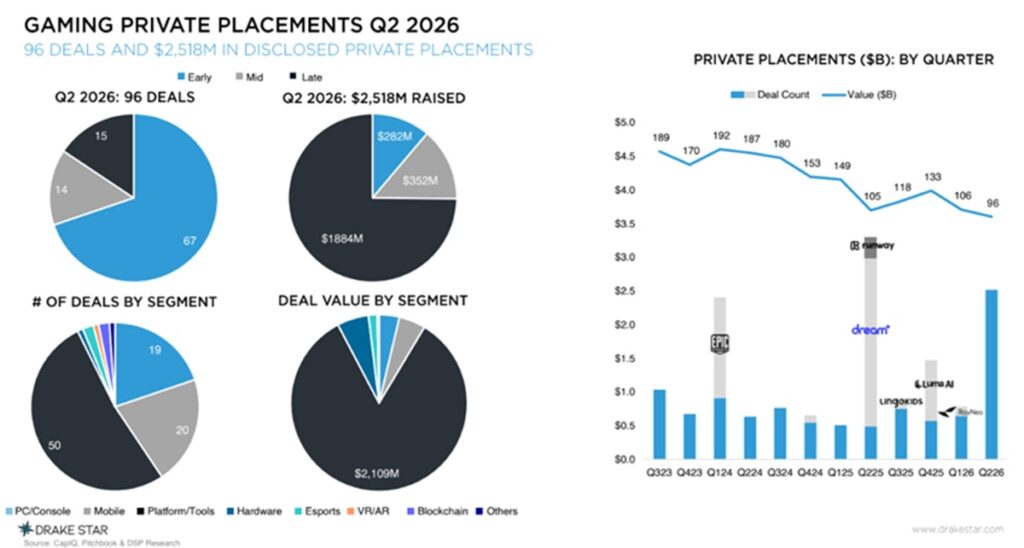

Game companies raised $2.5 billion across 96 private financing rounds, making it the strongest quarter by disclosed financing value in the past 12 months and the second-highest in the last three years, said Michael Metzger, partner at Drake Star, in an interview with GamesBeat.

The deal activity was driven by several large financings in gaming AI, AdTech, and hardware.

Notable financing rounds included AppsFlyer ($1.0 billion), General Intuition ($320 million), Decart ($300 million), Tripo AI ($200 million), Palmer Luckey’s ModRetro ($145 million), Chess.com, Grand Games, Astrocade and GreaterThan Group.

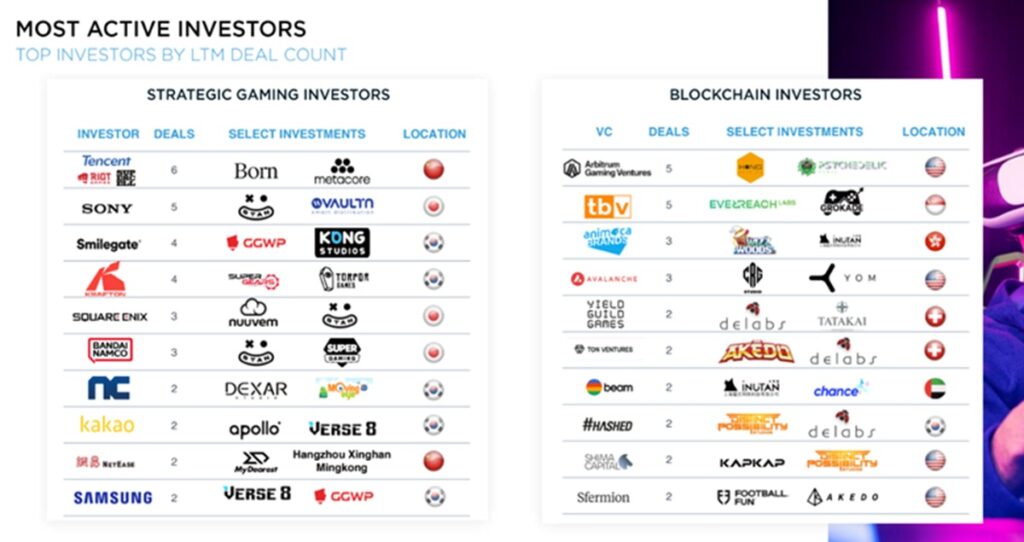

Over the last 12 months, Bitkraft, General Catalyst, and Play Ventures topped large-fund activity, while Impact46, Merak, and ForsVC led at the seed stage. Tencent, Sony, and Smilegate dominated strategic deals, with Arbitrum, TBV and Animoca leading in blockchain.

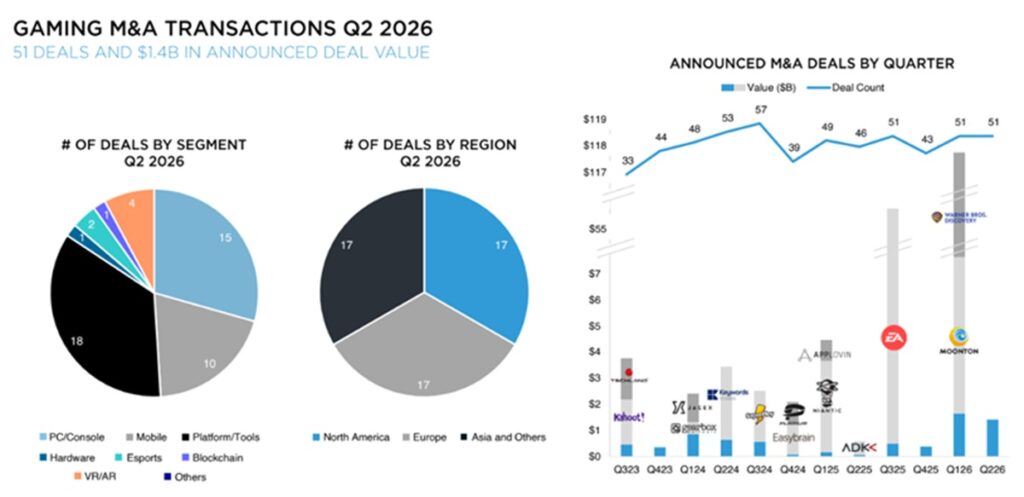

Gaming M&A activity remained at a healthy level at $1.4 billion in deal value, with 51 deals, primarily involving smaller to mid-sized platform/tools companies and PC/console and mobile game studios.

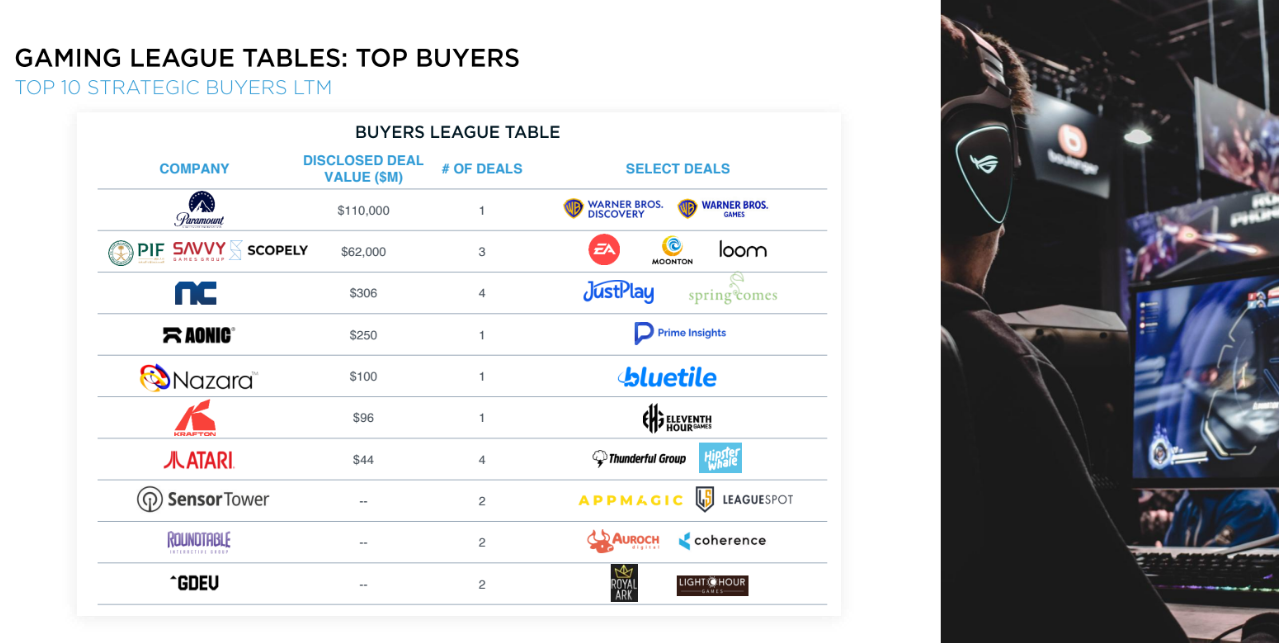

Notable deals included the acquisition of Playstack by TPG’s investment vehicle IMC, the CCP Games management buy-out from Pearl Abyss, Supercell’s acquisition of Metacore, and Atari’s purchase of Hipster Whale. The WeMade founder announced to sell a controlling stake to NeoPulse (in a deal valued at $590 million) and LY Corporation became the largest shareholder of Kakao Games. The CCP deal was in the works for a while, and the Atari deal showed the value of retro gaming, Metzger said.

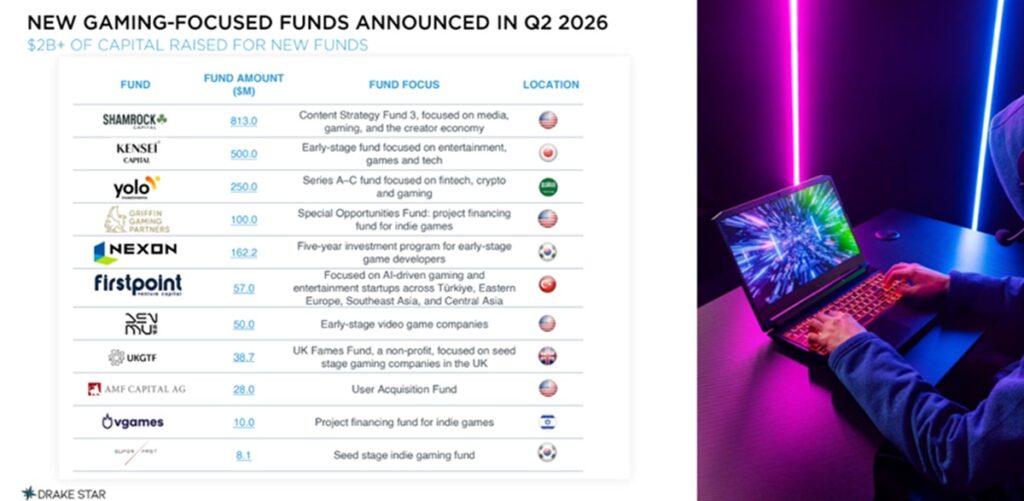

Also significant for the comeback of venture investments in games was this: Ten new funds were created with capital totaling more than $2 billion during Q2’26. These included Shamrock’s Content Fund 3, Kensei Capital ($500 million), and Yolo, while Griffin Gaming Partners and Vgames launched indie developer project financing funds.

Shamrock Capital will invest in a variety of entertainment, including games. In the past quarters, a few user acquisition funds focused on mobile games also got started, including at Vgames, General Catalyst and Plan A Games. This means that perhaps the dearth of funding for a few quarters in recent times was rock bottom for game financing. And maybe the funding could be more plentiful in the future.

Metzger noted that startups in certain territories like Turkey and Asia (outside of China) are attracting more capital, with more money going into mobile, Metzger said.

“It did seem like the pendulum had swung over too far over to too few fundings happening for for a time,’ Metzger said. “I think we are stll on the downtick in the number of financing rounds, which are heavily focused on platforms and tools.”

There were relatively few equity investments by venture capitalists in game studios. More money went into AI tools and other tech. That means game entrepreneurs will have to tap into other kinds of funding sources, as publishing deals are also scarce now.

The major console makers may be strapped for cash because of the cost of memory chips, driven upward by demand for AI chips because of the AI boom. Faced with rising prices of gaming hardware and expected high prices for new consoles, gamers may stick with their older machines for longer. China’s Tencent and NetEase are not as active as they used to be, but Tencent has articulated that it is still looking at potential investments closely.

The Korean game companies, on the other hand, are more aggressive at investing. Those include Nexon, NCSoft, Krafton and Pearl Abyss. But rather than buy firms outright, they tend to invest as strategic investors, taking minority stakes.

Drake Star said the key strategics to watch include Saudi Arabia Public Investment Fund (PIF)/Scopely, Krafton, NCSoft, MTG, Take-Two, Netflix, everplay, and Keywords Studios. Drake Star also expects more private equity-led deals involving CVC, EQT, Haveli, MEP Capital, Shamrock, Blackstone and TPG.

Blockchain deals were scarce, and most deals related to them are relatively small.

Public market activity was driven by the IPO of Liftoff Mobile ($502 million raised) and the $210 million debt financing by Stillfront. MTG’s PlaySimple Games announced an IPO ($350 million) and Embracer announced the plan to spin-off Fellowship Entertainment.

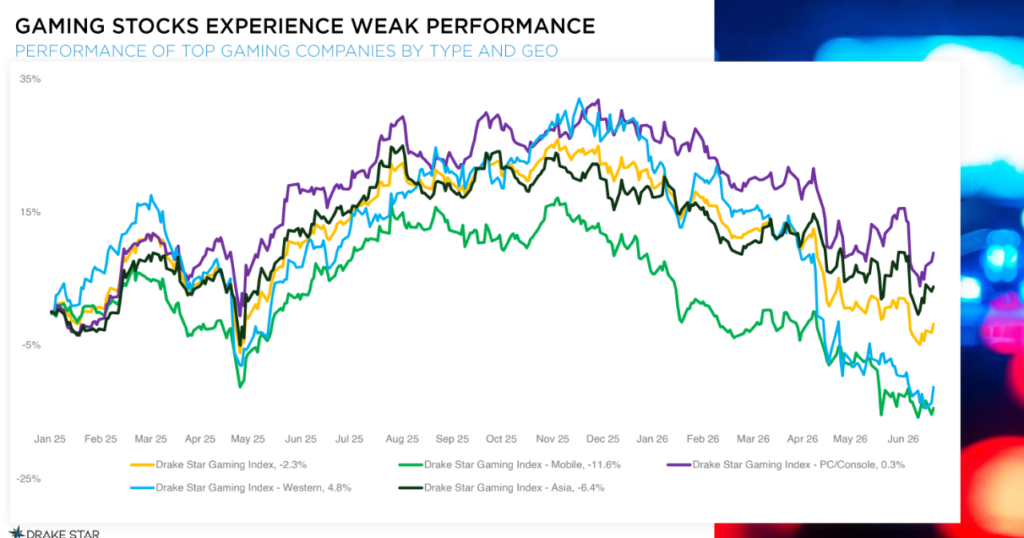

The Drake Star Gaming Index rallied strongly through mid-2025 before weakening over the following quarters, ending down 2.3% since the beginning of last year. Top performers included NetEase, Corsair, and NCSoft. Over half of the public game companies saw significant stock price declines in the public markets.

The funding round for Luckey’s ModRetro suggests that the Oculus founder remains interested in retro gaming, even though he has had a bigger score with AI-focused defense contractor Anduril. Luckey is coming back into games at a time when the core console companies are running into slowdowns, layoffs and challenges with memory chip prices.

Like with AI in the general tech market, there’s a lot of interest from investors in the combination of AI and games, as the General Intuition deal suggests. Another AI tool maker, Tripo AI, raised $150 million for games in early July a month after it raised $200 million. Drake Star expects continued financing momentum across AI/tools, infrastructure, and the user-generated content (UGC) space.

As for the 3,200 current and pending layoffs at Xbox, Metzger said it doesn’t help the perception of the gaming market in general, but familiar investors may see it as a reflection of Microsoft’s own strategy in gaming, rather than a declining overall market. Once Microsoft starts investing again, it’s hard to tell where it will focus, beyond its own core franchises.

“It probably is also not going to make a huge difference in the overall perception of gaming in general,” Metzger said.

More influential, he said, was the relative weak performance of gaming stocks in the second quarter.

Regarding Grand Theft Auto VI, Metzger believes there will be a general lift of the gaming sector and the perception of it, yeah, and more money will flow into it again. The game from Take-Two Interactive’s Rockstar Games is coming out on November 19, and out of respect for and fear of the IP, almost no other game companies are launching titles in November.

Meanwhile, Paramount is still waiting for its $110 million acquisition (enterprise value) of Warner Bros. Discovery. While Paramount’s game business is small, Warner Bros. Games can generate a billion dollars or more a year in revenues. The deal is facing some opposition, as California and 11 other states sued to stop the deal as anti-competitive. But if the deal closes, Metzger believes that the gaming expansion will continue.