The U.S. games and esports industry is expected to hit a cyclical slowdown driven by weak economic trends in 2027 — despite the launch of Grand Theft Auto VI on November 19, 2027, according to a new report on games and esports by consulting and accounting giant PwC.

The U.S. games and esports report was part of PwC’s larger analysis in PwC’s Global Entertainment & Media Outlook 2026-2030. I spoke with CJ Bangah, a partner at PwC and analyst on games and esports, in an interview about the report. While Bangah spoke about both the U.S. market and the global market, the analysis in the report focuses on the U.S. market for games and esports. I’ve attached most of Bangah’s answers to my questions at the end of this story.

The reasons for the weakness in 2027 is that the Xbox and PlayStation consoles are expected to be in the last year before a relaunch in 2028, based on the best industry knowledge. That means that 2027 is a transition year, where sales are typically in a cylical downturn. On top of that, sales for GTA VI could lift 2026 results, but they may not be quite enough to lift 2027.

And there are other factors such as economic and political uncertainty (related to the war with Iran and more), tariffs and the memory chip price increases related to huge demand for AI. The latter has resulted in artificially high prices for gaming hardware, keeping systems out of the reach of many in the broader gaming market.

The general market findings

The report’s U.S. commentary said the games and esports market is reliant on all device categories and monetization models and is therefore one of the most diversified globally.

The U.S. is the second largest games market after China and is home to the world’s largest console gaming market. The U.S. is also the second largest mobile gaming market and the second largest PC gaming market. Overall, the U.S. games market can be described as mature, with a large majority of adults playing games and with well-entrenched monetization.

As the market is so diversified in its games content and service consumption, it is exposed to all the different market dynamics across the sector. Continued sticky higher-than pre-pandemic inflation is expected to dampen future demand for games hardware, content and services to an extent and contribute to a lower growth cycle.

Prices for console hardware, games software, in-game items and subscription services have risen as supply chain and production inflation has taken hold, which is impacting middle-income affordability across the sector. This has been exacerbated in recent times due to

import tariff policies set by the U.S. and is most likely to be impactful on the console and PC gaming markets, where adoption of hardware assembled in markets outside of the U.S. is key to the scale of the market.

PwC’s Bangah said in our interview that gaming is maturing as a category, with the growth coming out of complimentary entertainment solutions, like monetizing intellectual property (IP). Revenue is also coming from advertising revenue, thinking differently about purchase versus subscription revenue, live events, esports, and other things like that.

“That still continues to be true when we look at the category this year. Some of the growth in gaming is actually being reflected in other categories, so it’s being reflected in strong performance of the media rights and the streaming platforms and other things. So, I would say gaming is a healthier category than it might look on face value, if you just look at the gaming filters themselves,” Bangah said.

But Bangah noted that there is a “deceleration in the growth rate for cloud and subscription gaming.”

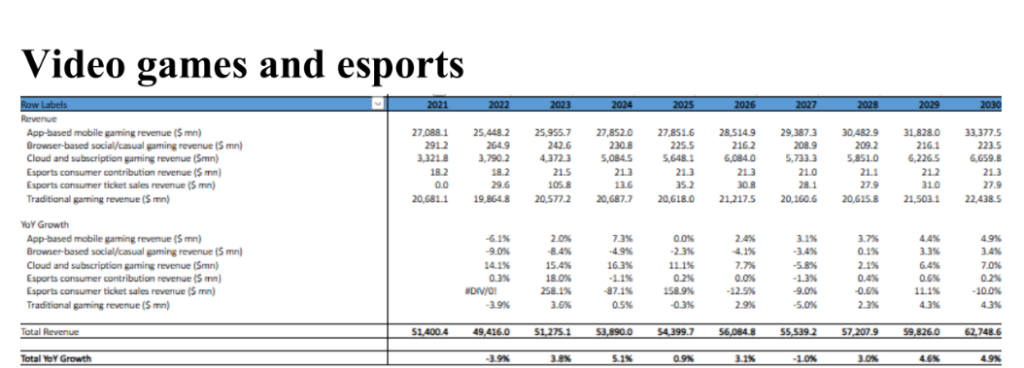

Back in 2020 and 2021, those categories grew at about 20%. But the forecasts are now slowing down to single-digit percentage growth. Esports is in the exact same state. In 2020 and 2021 it was a 16% growth rate and 23% growth rate, respectively. And now esports is also slowing to single-digit percentage growth. On top of that, video game advertising growth has decelerated.

“I would argue that this is partially not getting the form factor right and not getting the brands right. I do think there’s there’s untapped potential with video game advertising,” Bangah said. “Social games have gone back and forth. They did pretty well over the pandemic, slowed down a little bit, sped up a little bit, and are slowing down [again].”

“Then, to your point on console games, our forecast has years with negative growth rates, and our forecast has years with very positive growth rates tied to the release of new platforms or consoles,” Bangah said.

PC games had growth from 2021 to 2022 and PwC is still forecasting growth here, but it’s a growth rate that’s below GDP. If you’re growing at a rate slower than GDP, it doesn’t feel like you’re growing. Breaking down the categories in the forecast, you do have some different dynamics from different parts of the ecosystem, Bangah said.

Console gaming market

Console market performance and outlook depend on adoption of the various console platforms and the expected launch of new devices coming into the market. Overall U.S. sales volumes of new console hardware to consumers across 2024 and 2025 performed at historically low levels and is unlikely to significantly recover until the launch of the next-generation Microsoft and Sony consoles at the end of 2027 even with Nintendo’s Switch 2 selling well.

Some of this softening adoption is likely related to the increased cost of console hardware, and this will be a factor moving forward.

There has also been a shift in strategy from the console platform owners, which are now more focused on profitability of hardware as well as content rather than heavily subsidizing hardware to promote adoption.

This has resulted in console hardware price increases, higher than predicted console hardware launch prices and a prediction that future consoles will be more aligned to actual component costs. This expectation will impact the console adoption outlook to an extent. In the near term – over the next one to two years – there is also likely to be increased RAM costs for console hardware and PCs. Additional pricing pressure will have a negative impact on adoption.

Console market performance and future sales of hardware also depend on the availability of some standout titles which are big enough to move the market due to their expected sales volume. This includes Take-Two’s (expected to be) hugely popular game Grand Theft Auto VI, which has been delayed from 2025 into 2026, and which will drive adoption of PlayStation 5 and Xbox Series consoles when it arrives.

This title alone will help mitigate some of the expected decline of the console games market in the U.S. when it arrives at the end of the year. The importance of the U.S. to the broader console gaming segment cannot be underestimated. The U.S. represented 43.0% of the global consumer spending on console games content (outside of subscriptions) so any disruption to the sales in the territory is likely to have a detrimental impact on the global opportunity.

Mobile games market

The mobile games market is underpinned by smartphone adoption and the dominance of Apple iPhones in the U.S., which monetize at a higher level on average compared to Android smartphones. With smartphones heavily penetrated, market growth depends on the launch of specific games that ignite engagement – Monopoly Go! for example (with revenues that have topped $6 billion) – as well as the roll out of more in-game app advertising and improved monetization. These gains are likely to be relatively small due to the scale of the existing market.

Mobile games publishers with major exposure to the U.S. market are more aggressively pursuing off-app store direct-to-consumer monetization strategies to drive increased margins. While this is unlikely to dramatically alter the scale of consumer spending on mobile games, it will support the commercial viability of the U.S. mobile games market over the forecast period and the local industry.

Significant advertising revenue from in-game advertisements reflects the advanced nature of the advertising ecosystem in the U.S. market, and as a result will continue to play an important role in the overall mobile gaming segment performance. Advertising performance will be impacted by any future changes in macroeconomic factors. At present there are no major dynamic changes on the horizon built into the in-game app advertising forecast.

PC gaming market

The PC gaming market in the U.S. is largely driven by premium digital games bought via storefronts such as Valve’s Steam and Epic’s Games Store and live service PC online games.

The key drivers for these segments are threefold: continued interest in long-standing live service games including Fortnite, Battlefield 6, Call of Duty, Counter-Strike 2 and Grand Theft Auto Online; the popularity of user-generated content games platforms, such as Fortnite and Roblox; and the expansion of PC gaming access points including from Valve’s handheld Steam Deck, its upcoming Steam Machines and other PC gaming handhelds. The high pricing of this gaming hardware is an inherent dampener on adoption, with these devices expected to remain niche over the forecast period.

The premium PC games market is also being driven by increased access to franchises traditionally exclusive to the console platforms. This trend will continue to expand in the coming years. This is especially true of Sony PlayStation and Microsoft Xbox-based franchises. This major change in exclusivity strategies from the console platform owners is fueling a convergence of the console and PC gaming markets.

In terms of games content distribution, streamed or cloud gaming-based distribution remains a nascent pursuit for a vast majority of gamers. Usage is increasing, but fundamentally this form of distribution is not likely to reach an adoption tipping point over the forecast period. It is likely that Netflix and Amazon’s use of this technology to deliver family and party gaming experiences via connected TVs will expand usage from gamers unaware of how they are receiving the content, but these will not majorly change the commercial dynamic of this part of the market. Multi-game subscription services have reached high penetration across key console platforms, so growth moving forward is expected to be low.

Most consumer spending growth on these services in the U.S. will come from increased monthly pricing costs.

The esports market

The U.S. esports market grew rapidly from 2015 to 2022, driven by global enthusiasm and online streaming growth, attracting major investments in tournaments, teams, and media rights. In 2023, the sector entered a correction phase as interest declined and profits lagged, resulting in fewer sponsorships, reduced tournaments, team consolidations, and the loss of major tournament media rights deals. Key drivers for the esports market in the U.S. include stabilized media rights and sponsorship deals, alongside a gradually growing online video streaming advertising revenue and a moderate recovery in tournament ticket sales.

U.S. segment numbers and overview

The U.S. games and esports market is expected to grow at a compound annual growth rate (CAGR) of 3.8% over the next five years, moderately ahead of a global five-year CAGR of 3.6%. In 2025 the US share of the global games and esports market was 27.2%, making it the second largest market behind the Chinese Mainland.

That share of the global market is expected to stay consistent over the forecast period. The

slow growth performance of the sector and the inability to increase its share reflects the mature nature of the market, while the scale of the market reflects that monetization per gamer in the U.S. is significantly higher than other markets. The strength of the console market in the U.S. helps drive this high monetization.

The traditional gaming segment (console and PC gaming combined, but excluding multi-game

subscriptions) had a 29.4% share of the U.S. market in 2025 and was worth $20.6 billion. This share of the total market is expected to shrink to 26.6% by 2030, with traditional gaming reaching $22.4 billion.

While PC gaming is expected to accumulate slowly over the five-year forecast period, console gaming will be impacted by the decline in the Sony PlayStation 5 and Microsoft Xbox Series cycles and the launch of a next generation of consoles from these companies from 2027 onwards. Nintendo Switch 2 consoles will continue to sell well, but overall, not at the level of the original Switch, although digital in-game and downloadable content is a growth opportunity for the platform.

The release of Grand Theft Auto VI will be a major cultural event for the sector in the U.S. Console software sales volume in 2026 will be up and console hardware sales for both PlayStation 5 and Xbox Series will be supported by reducing any normally expected decline as these devices reach the later stages of their lifecycles. However, over the forecast period, neither console nor PC gaming markets are high-growth opportunities in the U.S., with an expected five-year CAGR of 1.7%.

The social/casual gaming segment (mobile gaming, mobile in-game app advertising and browser gaming combined) had a 59.6% share of the U.S. market in 2025 and was worth $41.8 billion. This share of the total market is expected to grow to 62.9% by 2030 with social/casual gaming to reach $53.0 billion.

Consumer spending on mobile gaming is predicted to grow slowly over the forecast period reflecting the mature nature of the market and existing strong monetization with less upside potential.

Direct-to-consumer growth

Against this backdrop of slow growth, most mobile games publishers will be looking to drive better profitability by shifting more business off native app store platforms and into direct-to-consumer webstores. This will not change the growth dynamic of the sector however but is likely to improve profitability, making it more commercially viable for a broader set of participants.

In-game app advertising is expected to grow at a more rapid pace as more games use advertising to monetize, and casual games that use advertising shift towards more engaging gameplay types. Browser gaming is expected to decline slowly over the five-year forecast, with the decline in PC-based browser gaming being largely offset by growth in the mobile-focused part of the market.

Multi-game subscriptions and cloud gaming growth

Consumer spending on multi-game and cloud gaming subscription services is predicted to grow at a 3.4% CAGR over the forecast period and reach $6.7 billion by 2030.

Recent increases in spending have been largely driven by service pricing increases, with some subscribers shedding as a result, and by upselling higher tier services to existing subscribers. This trade-off will continue to be made over the forecast period, and price increases will become more commonplace, much like the pricing strategies applied in the subscription video-on-demand business.

Subscriber numbers in the U.S. are expected to moderately grow from 50.2 million in 2025 to 53.6 million in 2030, although growth will not be linear. 2026 and 2027 are expected to deliver a reduction in overall subscriber numbers as Sony and Microsoft console platforms hit a transition period before the next generation of devices.

While consoles remain the core platforms spending on games subscription services, it remains to be seen if an ad-supported lower tier of games subscription services will be launched in the short- to medium-term. If this does occur, this is likely to deepen penetration, expand the number of revenue streams available to subscription service operators and diversify the revenue make-up away from consumer spending to advertising revenue to an extent.

Esports numbers

In 2025, the U.S. esports market entered a low-growth stage, reaching $363.3 million. The outlook is benign, with growth in the region expected to be flat over the forecast period. From 2026 to 2030, the market will experience some volatility due to tournament organizers rotating finals across major markets to optimize ticket and streaming revenue.

Annual events for titles such as League of Legends, Call of Duty, Madden NFL, EA FC, Valorant, and Apex Legends will help stabilize the market during this period, despite continued volatility from rotating major finals. The return of lapsed leagues like NBA2K suggests potential

upside as the market moves toward a sustainable business model and tournament format.

CJ Bangah’s interview observations: More competition for gaming

I noted that Matthew Ball’s slide deck drew attention to the attention war, or the battle for the available time that people have in the day for entertainment. I asked Bangah if she saw the market the same way.

“We see video gaming increasingly competing for share of attention, which translates to competition for share of wallet, and the competitive set that are attracting gamer dollars has expanded from prior years,” Bangah said. “You see things like futures markets, gambling, betting, other categories as well, growing. From our perspective we would agree with the forecasts that gaming is facing competition that is historically a captive base.”

Bangah noted other industries are growing from a smaller base and have higher growth rates.

How big will Grand Theft Auto VI be?

Regarding Grand Theft Auto VI’s arrival on November 19, I asked if a single title could shift the industry growth by multiple percentage points. Bangah noted the company doesn’t do forecasts on single games.

But she noted in this case that there is a lot of conversation about the potential market lift.

“You’ve got some really big, really exciting gaming titles coming out from a few publishers, and I think that you’re also seeing executive announcements on how they’re thinking about player engagement and listening to gamers on how they evolve the way that they go to market,” Bangah said. “We absolutely could see that a return to the roots of what makes gaming such a great category, with really compelling creative content driving enough lift and growth.”

She added, “For the most part, we’ve tried to model that into our methodology of expecting some of these big title releases and expecting that that could be a nice groundswell for growth, but unfortunately, we don’t do for title modeling or attribution.”

Gaming versus the addiction industries

I noted that games tended to stay on the side of fun and avoid addiction. It’s still possible with things like loot boxes to veer toward addiction. But gaming also catches kids while they’re young, prompting many brands to wonder if they need to be on Roblox or Fortnite. Gaming can also veer into over-monetization tactics, as Ball warned, when growth in a market slows, as game companies may try to extract more money from existing players. Gaming can also take the battle back to its competition by spreading into movies and TV and taking up a large percentage content on TikTok and YouTube, rising from a subculture to mass culture. All of these trends can push gaming forward in mass culture or hurt its expansion.

“I love that optimistic view, and I will say, if you look at all of the categories in the entertainment media outlook, gaming is an optimistic category in terms of relative growth rate,” Bangah said. “We have portions of this ecosystem that have a net negative growth rate in future years. Some of the traditional form factors have lost enough share that you know they’re decelerating.”

Bangah added, “For gaming companies, a growth rate that is a single-digit growth rate feels like not growing in some ways, because new entrants continue to enter as a space. You have different methods of monetization. It is still a great category overall. We’re extremely optimistic about the future, particularly as you look at gaming as the zeitgeist of broader entertainment experiences.”

She added, “Building on your point of view, games have an audience that starts for children that are very young. [Kids] can begin to play very simple games all the way up to folks that are retirement age. It has this wonderful broad reach. We are also increasingly seeing non-gamers discover gaming through other formats.”

And she said, “So they’re discovering it through movies and television, and they might may not even know that it was a game to begin with. I think we’re going to attract incremental gamers to this ecosystem, just as the gaming publishers do a more and more effective job of monetizing their IP and putting their IP in the market in a way that allows for year-round player engagement and year-round connection with some of these really, really beloved brands.”

Is gaming’s growth inexorable?

I asked if that growth of gaming throughout society gives us an annualized or inexorable growth rate. And I also asked what is affecting games in 2027, where the forecast shows a dip into negative growth. Was that due to war, inflation and a console transition that could happen by then, where the last year before a console launch usually shows negative growth?

“The baseline of all of our forecasts assumes a relatively stable economy, and when you have supply chain disruption, when you have rising hardware costs, when you have AI taking up a lot of capacity in terms of available energy, future construction –all of those dynamics can absolutely impact the potential for media categories that are beloved,” Bangah said. “The impact is not as stark as it is on some other categories of the economy, because even if, and particularly when things are maybe not ideal in the world, a very human reaction is to reduce the number of streaming subscriptions they subscribe to.”

She added, “Folks may delay getting a new phone. They may put off some expenses that are discretionary, but we, as human beings, want to be entertained, and we want to, in many ways, escape even more. And so when we look at economic down years — and we’ve done this report for 27 years now — it’s not a cratering of the ecosystem from a media perspective. It is a tightening in some categories, where again consumers may cancel some subscriptions, but they’re still playing games. They’re still watching television. They’re still often going to movies. They may just not go to as many. Those fundamental human desires to be entertained come through and drive some durability in the category. It may mean things like they may not buy the new console. They may wait another six months until they feel things are a little bit more secure.”

New forms of entertainment competition

I asked if there were new categories added to the entertainment and media markets, like prediction markets.

“We added online betting for exactly the reason you would think, and what you said earlier is competing for share of wallet and share of attention, and it’s something to pay attention to from a media and entertainment perspective,” Bangah said. “It is absolutely growing quickly, and it’s absolutely taking folks’ time. The thing I do like about it, though, is the linkage to broader media experiences. Live sports and some of these other things. There’s a growth flywheel that’s nascent right now that could mature over time and make it a category feels like it’s helping the industry as a whole grow and do better. That would be my optimism coming through.”

The risk of regulation

The risk for the addiction markets is that regulation will likely increase in different parts around the world and stop the growth of those categories, like in India, where all forms of gambling were banned. I asked about that.

I noted this is kind of the choice that the gaming companies have to have to make as well. If they they push more towards loot boxes, then they’re going to get regulated. If they stay in the lane of fun, they’re OK.

“Regulation will always have the ability to impact growth rates in the entertainment media sector. A really great example of this was a few years ago. The cinema market in Saudi Arabia just massive growth, right?” Bangah said. “Because it was finally legal, the number of movie theaters that were being built in Saudi Arabia went from zero to hundreds. And so we absolutely do see the impact of regulatory policy choices, by country, by category growth rates.”

Bangah noted that markets that have a preference towards local content, so a percent of airtime needs to be dedicated to local artists [when it comes to] local television shows.

“You see this in Canada, you see this in China, you see this in other markets around the world, so I do think those dynamics are always going to be there,” Bangah said. “In terms of regulation, it can be a powerful force for growth and performance, and you can protect culture. Some regulations can also inhibit growth in a very meaningful way.”

Will gaming attract more investment?

I asked if PwC monitors investment levels and whether gaming might be losing investment to other categories that are growing faster. She noted the company doesn’t include that in the entertainment media outlook.

“We do look at market shifts more broadly in some of our work with clients, but usually that’s like a project-specific consideration versus something that we have at the 10,000 foot level,” Bangah said. “It’s a good question, because if you think about the broader private equity ownership shift, where you’re seeing PE companies gobble up all sorts of firms, like dentist offices and other things, then you put them together, put them on one back office, you take the costs out.”

Bangah added, “I don’t know that I’ve seen that in gaming. That would be an interesting thing for us to talk about in the future, if those dynamics shift. I think that we have large, established gaming companies that are self-sufficient and don’t need to attract a ton of outside investment beyond normal market mechanics. So I don’t know that we have seen anything that would suggest a massive capital reallocation play, or somebody like a PE firm coming in to fundamentally change the ownership dynamics. But it could be something that comes on the horizon.”

The concentration of entertainment

I noted there is an increasing concentration of entertainment in big companies, like with Paramount’s acquisition of Warner Bros. Discovery.

In response to that, Bangah said, “I can’t speak specifically to individual companies, but I will say it’s part of a broader trend where the gaming companies are looking to create a growth flywheel that spans outside gaming. We saw this with esports. We see this with media rights. We see this with IP monetization. More broadly, with live experiences, rides, T-shirts, stuffies, collectors’ items — all these other kinds of things. And you’re seeing traditional media companies look at video gaming, see a growth rate that is above most categories in entertainment media. Gaming technically has a better growth rate, and on average, particularly for marquee titles, highly engaged fans that buy the next release.”

Bangah added, “They are playing frequently to spend time on gaming, to connect with their community and have a place that feels fun and engaging. So you’re seeing the traditional media companies want to do more with gaming because they know how powerful it could be in terms of a growth flywheel.”

And she said, “They know how amazing it is to have gamers in your consumer set, versus some of the traditional consumers, just because there is again the potential for so much brand love that fosters loyalty, and it fosters retention, and it fosters this ability to drive revenue growth in a way that some of the other categories have struggled with particularly in the last five or 10 years.”

Is gaming the most engaged form of fandom?

I asked about the comment from Dan Prigg, head of games at Paramount Games, in an interview with GamesBeat. He said that games are the most engaged form of fandom of any entertainment.

“You could debate this with some of my colleagues have kids, and they’ll watch their kids play games, and they’ll watch their kids play games and be on their mobile devices. They watch short form video and play games as well, but I think just the nature of a form factor, like if you’re using your hands on a controller and you’ve got your headphones on and you’re in your gaming chair and you’re hanging out with your friends online, that is a very leaned-in experience.”

She added, “Whereas many other media experiences have become almost leaned out, where being on your social media and watching a television show is a super common way to consume television, and I think that’s where you’re seeing some of the providers of those services look for ways to make it a little bit more interactive and make it a little bit more engaging because they want it to be something that is as sticky with the consumer as gaming

is.”

How much are brands diving into gaming?

I noted we hear anecdotal stories of the brands recognizing this and leaning into gaming, like the hundreds of brands that have gone into Roblox. Is this measured in some way?

Bangah said, “When you think about how generative AI is changing discovery — like it’s changing search — it’s changing how consumers plan trips, decide what’s better to buy. Etc. When you look at a world where GenAI is fundamentally transforming things, the agentic navigated internet is one of the fastest growing internet categories out there.”

She added, “From a brand perspective, if I’m presuming that some television experiences are going to be leaned out experiences, it makes it hard to want to put the same number of ad dollars behind some of those experiences. If my hypothesis is a consumer is going to be on their phone and watching television at the same time, and they may not really see my ad, and so I think what you see with some of these gaming platforms that have effective brand sponsorships and effective brand advertising arrangements, it’s brands saying, ‘gaming is pretty darn close to universal.'”

Bangah said, “If you have an internet connection, gaming compatible advice, it doesn’t matter if you’re a child or you’re a retiree. You could play and find joy in games. So, I think the brands realize that, and so finding ways to partner with some of these gaming publishers in a way that opens brand awareness and brand preference for new consumers and audiences in a highly engaged format can be really appealing from a brand perspective.”

She added, “From a publisher perspective, if you’re facing rising hardware costs, rising development costs, rising costs just to get your game out the door, having the ability to have a brand augment your profit margins and not have to pass costs on to the consumers is really appealing. We’re not tracking that specifically, but does feel like an industry focus area that’s going to continue to grow.”

Could rising memory prices help cloud gaming?

I noted that rising memory chip prices could be counteracted by cloud gaming, as all that requires is a connected TV, a broadband connection, and a controller — as well as a connected data center. You don’t have to buy a console for cloud gaming and so the memory cost is lower.

“We’ve been talking about cloud gaming having a great profile for a long time, and it’s interesting because it does vary by by market, right? So I think the markets that you know have healthier growth rates. If you look back, India had a 59% growth rate between 2020 and 2021. It had these really healthy growth rates. And so cloud gaming tends to be this category that clearly has value from an ecosystem perspective. It can be really effective, and I think the question of why isn’t cloud gaming bigger — this feels like it ties back, I hate to say, to the business fundamentals. The business fundamentals is the price not quite right, the product not quite right, the user experience is not quite right. So, I do think as the category matures, it absolutely could become more and more compelling, particularly when you look at the dynamics with hardware costs.”

Growth from 2028 to 2030

I asked Bangah if PwC foresees an industry driver that returns gaming to growth from 2028 to 2030.

“A lot of what we are forecasting tied to growth really does tie to the things we’ve talked about earlier,” Bangah said. “It is the dynamics of presuming that gaming continues to win the attention wars. You have fresh consoles, fresh content, and IP. We have some of those zeitgeist or growth catalyst releases that you talked about earlier.”

Bangah added, “We’re also continuing to expect mobile and casual gaming to do well. We’re also expecting that, while esports is maturing, the broader industry growth flywheel comes from durable entertainment ecosystems that are being created. Look at gaming, advertising, subscriptions, IP monetization, and just broader audience engagement. So it’s the underlying linked dynamics that are underpinning our projected growth forecast.”

Bangah noted ther are major acquisitions happening in gaming and entertainment. Traditional media is trying to get into gaming, and gaming is getting into traditional media.

“How those come together could be an interesting thing for you to explore. Not that we perfectly cover that topic in the entertainment media outlook, but I do think it’s an interesting dynamic of the industry that I don’t see getting a ton of coverage in terms of why are others coming to gaming and why is gaming going everywhere else. What is the entertainment company of five to 10 years from now? Is it going to be a full stack entertainment company that has everything from theatrical releases to streaming services, to games, live experiences, and everything else? It does feel like that powerhouse ability is being curated across a few large market players right now,” Bangah said.

Will the U.S. become a smaller part of games?

I asked if the U.S. was a smaller and smaller percentage of the gaming market, mainly because of high growth rates in places like the Middle East and China and Brazil.

“We have for years been forecasting the majority of entertainment media growth coming from outside the U.S. across all categories, gaming included, and a lot of this in the markets that have really high growth rates. They’re increasing with good GDP growth, typically a younger population with growing disposable income. So when you look at markets like Pakistan, and when you look at Middle Eastern countries, where you know there may be policy shifts that open up new entertainment categories, there’s a lot going on there that could be really, really positive, and then create those growth rates.”

She added, “When you think about why the U.S. isn’t growing at a faster rate, maturity is the biggie, and our population isn’t growing at a high rate. The latter brings you a bunch of new, younger consumers on a regular basis that’s consistent with some of these other countries around the world that have massive population growth, improved buying power. Folks that have the ability, through better internet connections, to afford devices, to enter these new categories, and so they’re just doing really, really well.”