Venture capital investments in the first half of 2026 have broken records, thanks to huge funding rounds for AI companies OpenAI and Anthropic.

Funding exits were the largest ever in the first quarter, and if its deal value were a full-year total, it would have been the third largest, according to a report by Pitchbook and the National Venture Capital Association (NVCA).

By itself, OpenAI’s $122 billion round collected more value than all other quarterly totals ever. The deal was more than four times larger than the second-biggest deal of Q1, Anthropic’s $30 billion round, which was larger than all deals under $100 million completed during the quarter.

Anthropic has since added a $65 billion round, and both companies have confidentially filed for initial public offerings (IPOs).

Mega-IPOs are the real story of the year. SpaceX’s IPO was completed at a roughly $1.75 trillion valuation in June, while Anthropic and OpenAI are expected to complete their own $1 trillion IPOs in the coming months.

These events have surfaced the biggest contradiction in the VC market so far this year: Liquidity is not widely available, yet these three companies have created more value than all VC-backed IPOs this century. They are the greatest example of the power law of venture. Beyond these companies, liquidity has remained low. There is a growing pipeline of IPOs, but it is in the single digits.

Fundraising also showcases the contradictions in the first half. About $62.4 billion has been closed year to date, putting 2026 on pace to have the third-highest annual figure ever. Yet 73.1% of closed commitments in Q1 went to five firms, and megafunds have roared back after a couple of years of slower fundraising.

The biggest difference in current fundraising from the highs of 2021 and 2022 is that those years brought hundreds of new limited partners into the venture ecosystem. Many of those LPs have since left. Those that are filling the space, such as sovereign wealth funds, now see that the venture market has grown large enough to put material amounts of money to work, and they are doing just that, investing amounts of capital in new funds that would dwarf past commitments.

H2 2026 will likely see many of the same trends. Mega-IPOs will be the main story. Secondaries are set to gain further popularity as liquidity keeps stalling. Dealmaking will continue to see increased activity levels despite concentrated fundraising and a lack of broad liquidity, unless the mega-IPOs have a poor reception from public market investors, which seems increasingly unlikely.

Overall, the report said the first half of 2026 has been six months of contradiction and concentration. Dealmaking, fundraising, and liquidity have each shown volatility, even if they have been largely insulated from the uncertainty surrounding war in the Middle East and returning inflation. VC activity has also been unencumbered by the rising political challenges to AI and the growing anti-AI sentiment among the U.S. population.

The view of the past six months

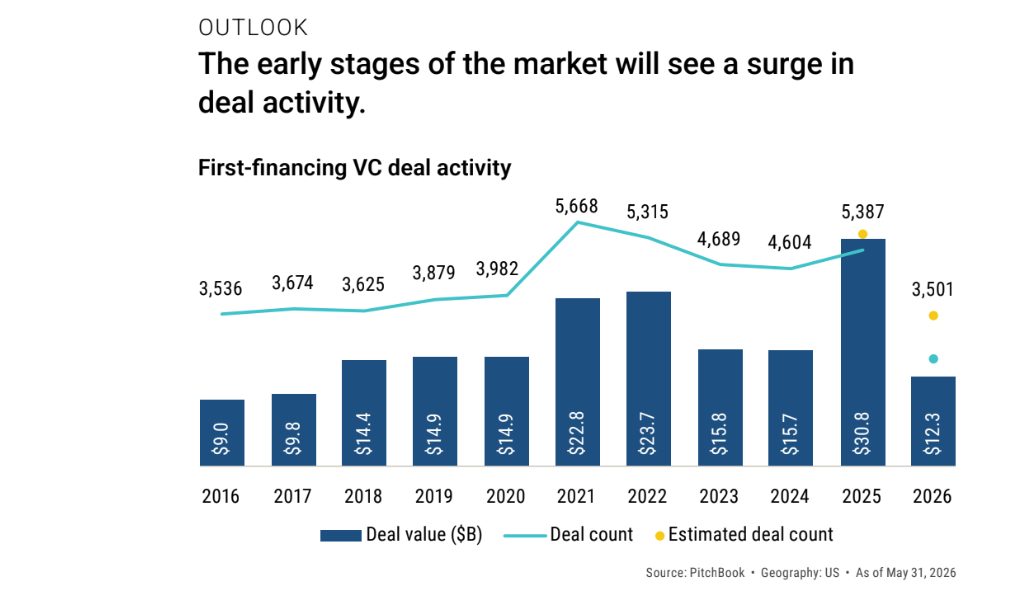

Kyle Stanford, director of VC Research at Pitchbook, said in the report it would have been counterintuitive to expect increased activity in the early stages of venture during a liquidity slowdown and a sluggish fundraising market, yet the early stages had already begun to defy expectations in late 2025. Through Q3 2025, venture funds had closed only $45 billion in new commitments, the lowest total since 2017.

Additionally, many small funds and emerging managers that raised capital in 2021 or even 2022 had likely used most of their dry powder and were unable to be active investors, at least to the extent needed to boost deal count. Yet first-financing activity through the first three quarters of 2025 was just 200 deals behind where 2021 stood in the same time frame, which had become the high-water mark for companies receiving their first investment. On top of that, early-stage deal count had increased in each of the previous three quarters, and our estimated early-stage deal count for full-year 2025 was roughly on par with full-year 2023 and 2024 totals.

Two major trends pointed directly toward 2026 being a highly active year for early-stage VC. First, AI had driven investor focus and shrunk the cost of building a company. This was not novel, as hype and costs are two directly related trends that can impact investment. Second, multistage investors with seemingly unlimited follow-on capital had increasingly been investing in seed and Series A rounds, and the data supported their recalibrated strategy.

Between the beginning of 2024 and November 7, 2025, Andreessen Horowitz had invested in more than 300 seed and Series A deals, and there was reason to believe that more large firms would adopt this strategy.

Through the end of May, US first financings were tracking to exceed 7,000 by year-end, which would be the highest annual number of deals by more than 1,300. Even without the estimated deal count, which estimates the number of lagged deals that will be recorded later, the year is on track for nearly 6,000 first financings, which would itself be a new record.

The ability of untrained coders to develop concepts and initial products or websites with Claude Code and OpenAI’s Codex has brought the barrier to launching a company down to the lowest levels ever seen. According to Stripe, the percentage of C-Corp companies launched through Stripe Atlas without co-founders reached 63% in Q2, an all-time high.

AI activity continues to reach a fever pitch, and the largest investors keep fueling the fire. As of June 11, Andreessen Horowitz had made 74 seed, Series A, and Series B deals in 2026. General Catalyst, Lightspeed Venture Partners, and Sequoia Capital together had accounted for another 104. These funds have not become active early investors; instead, they have continued to grow larger while becoming more entrenched in seed and early-stage deals.

Andreessen Horowitz has announced the closing of $15 billion worth of funds this year, yet its focus remains on young or new companies. And that is for good reason: The early stage continues to drive outsized returns, but for such large firms, the mechanics of those returns are different. Seed deals are as much of a deal-sourcing platform as they are a return-generating

investment.

A 50 times return on a $10 million investment would provide $500 million to a fund, but that would be roughly 3% of Andreessen Horowitz’s commitments closed this year. Megafund managers follow on to increase stakes or simply keep stakes high, and the continued development of the institutional secondary market is an opportunity afforded to existing investors. Holding a 20% stake in a $100 billion IPO was a hypothetical 10 years ago, but it will likely become a reality in the next few years.

AI’s ability to continue driving such high investor interest over the next six months may hinge on the Anthropic and OpenAI IPOs: not on their performance, but on their ability to sustain their growth under public market scrutiny. A high number of target companies will continue coming to market for a raise, but at some point, sustained investment levels will need to be validated by the continued dominance of the models that have driven investors’ focus on AI.

Later-stage deal activity will remain strong

By late 2025, late-stage deal activity had remained resilient despite the prolonged liquidity drought, said Kaidi Gao, senior research analyst for venture capital at Pitchbook, in the report.

Annualized late-stage VC deal value stood at $107.6 billion, second only to 2021. Venture-growth activity was on track for a record year, with annualized deal value surging to $150.2 billion, surpassing the 2021 record of $91.6 billion, and annualized deal count matching 2021 levels.

Deal value was heavily influenced by a handful of outsized AI rounds. The market kept bifurcating: Strong AI companies continued to access substantial capital from multistage funds and strategic investors, while companies that struggled to keep growing quickly faced funding strain. Through Q3, the number of active US unicorns had grown to 830 in 2025, with their aggregate post-money valuation reaching a record $3.9 trillion.

However, a large amount of capital remained tied up in these private companies, many of which had slowed in growth, increasing liquidity constraints and leaving them facing mounting survival challenges and difficulty raising follow-on rounds.

Against this backdrop, Pitchbook/NVCA projected a modest continuation of strength at the later

stages in 2026, contingent on the AI boom maintaining momentum and the exit market continuing to improve. A relatively stronger IPO environment was expected to pull crossover and corporate investors back into large, later-stage deals. The primary risk the team identified was the concentration of late-stage activity in AI: If public AI valuations were to contract meaningfully, private AI startups would likely face similar markdowns, weakening investor confidence and reducing their willingness to deploy large amounts of capital at that stage. A deterioration in the exit environment would compound that pressure, dampening appetite for companies approaching a liquidity event.

Midyear update: Outlook is tracking with some variations

Both late-stage VC and venture-growth deal activity have been strong YTD, with AI serving as a significant driver across both stages, said Emily Zheng, senior research analyst for venture capital at Pitchbook.

At the late stage, $59.3 billion was deployed across an estimated 1,990 deals through May 31, with annualized deal value on pace to reach the second-highest level in a decade, trailing only the 2021 record of $159.8 billion. Venture-growth activity was even stronger: $274.2 billion was deployed across an estimated 409 deals through May 31, already more than twice the full-year 2025 deal value, which was itself the highest in a decade.

Capital at both stages was heavily concentrated in a small number of high-valued AI companies. The four largest rounds YTD were raised by three leading foundation model companies: OpenAI; Anthropic, which closed two rounds; and xAI, collectively raising $237 billion. All four rounds were venture-growth deals, and their aggregate value accounted for 86.4% of total YTD deal value at that stage.

At the late stage, Waymo, the Alphabet-backed autonomous driving company, raised a $16 billion Series D round that alone represented 27% of total late-stage YTD deal value. The AI premium in median deal sizes further illustrates this dynamic: While the gap between AI and non-AI median deal sizes remains modest at Series B and C, at 12.5% and 7.5%, respectively, it expands sharply at Series D+, where the AI median deal value of $235million is 56.7% higher than the non-AI median of $150 million, reflecting the outsized rounds raised by the most mature and highest-valued AI companies.

The AI investment boom has largely tracked with the previous outlook, but the anticipated recovery in exits, especially large listings, has been slower to materialize. While fast-growing

AI companies continue to tap into abundant capital, the broader venture market has grappled with liquidity constraints amid a lackluster exit landscape. Since Q3 2025, the aggregate post-money valuation of US unicorns has grown from $3.9 trillion to $6.6 trillion YTD, driven largely by the highest-valued AI unicorns continuing to close record-high funding rounds at increasingly elevated valuations.

The scale of that appreciation is striking at the company level. The three highest-valued US AI unicorns—Anthropic, OpenAI, and Databricks—carried a combined valuation of $783 billion as of Q3 2025. So far in 2026, that same group, still the three largest active U.S. unicorns, has an aggregate valuation of $1.95 trillion, a near 2.5x increase over roughly eight months. The result is an unprecedented concentration of value in privately held companies, deepening the liquidity

constraints that continue to weigh on the broader venture ecosystem.

Despite record headline exit values in Q1 2026, underlying exit activity remains largely concentrated in a small number of transactions, with the broader IPO pipeline still thin and the pace of listings well short of what is needed to generate meaningful LP distributions.

The liquidity stalemate may be near a turning point. SpaceX went public on June 12, and Anthropic and OpenAI have filed to go public later this year. SpaceX’s debut was met with strong enthusiasm, with shares up 19% on the first day of trading on a heavily oversubscribed order book. However, the performance reflected constrained supply as much as fundamental conviction, with a limited float leaving unmet demand chasing a small number of available shares. A clearer read on business fundamentals will emerge as the company files its first earnings reports. Moreover, SpaceX is not a pure-play AI company: Despite growing AI revenue streams, its core business is aerospace and satellite connectivity. How the Anthropic and OpenAI IPOs are received will serve as the more direct pricing benchmark for mature AI companies and will likely shape valuation expectations at the late and venture-growth stages for the remainder of the year.