Partner content, presented by Boston Consulting Group (BCG)

After several years of headlines dominated by layoffs and studio closures, it’s easy to think the games industry is in decline. But Boston Consulting Group’s (BCG) new industry outlook signals a shift, highlighting strategic growth opportunities for companies that adapt quickly. These findings, and more, are shared in our latest global gaming report, How Platforms Are Colliding and Why This Will Spark the Next Era of Growth.

Our findings are not only based on extensive industry conversations and market data, but also on landmark research. We surveyed almost 3,000 gamers worldwide, who shared their unfiltered views on cloud gaming, AI, game prices, and more.

We selected five key insights to highlight from our research, but there’s much more to uncover in the full report:

The cloud wars

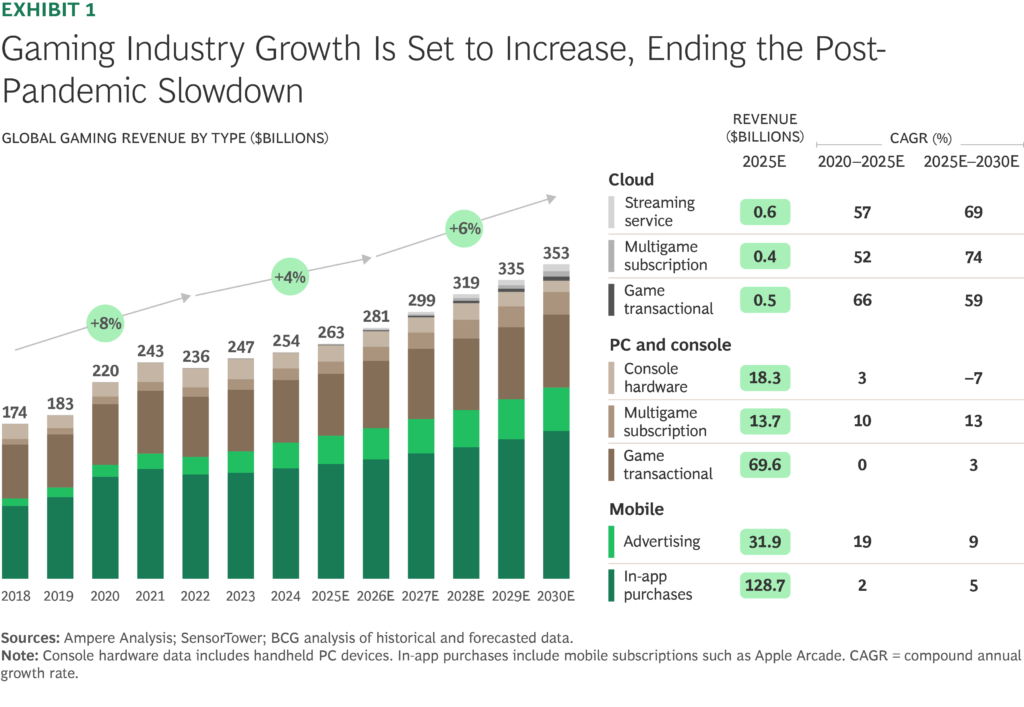

The most prominent theme in our report is how the new battle in gaming will be between competing ecosystems underpinned by omniscreen cloud gaming technology. Some 60% of players say they have tried cloud gaming, and 80% reported positive experiences. We forecast cloud gaming will grow into an $18 billion market by 2030, with 65 million players.

Despite this growth, we expect consoles to remain important, but more so as ecosystem enablers, not as standalone boxes.

This move towards competing ecosystems is driven by much more than cloud gaming, though. Roblox, Fortnite, and other titles are emerging as hardware-agnostic distribution channels, reshaping the industry landscape.

AI in gaming is inevitable

Players are largely comfortable with generative AI; even among older gamers, less than 10% expressed concern about AI-generated art, storylines, or NPC dialogue. Controversies will arise, but experiences matter more than the method of creation. Expect a new wave of AI-enabled studios focusing on novelty and topicality, with more games being published than ever.

The fight for discoverability

The increased number of games getting published, thanks to AI, and the shift to ecosystems will make discoverability even more vital. Developers who master community, algorithmic discovery, and new engagement-oriented business models, including subscription and microtransactions, will be the winners.

Instead of counting downloads, the winners will measure engagement by the minute and know how to monetize it, including via subscriptions, microtransactions, and advertising—we’ve got more insights on this specifically in the full report as well.

The app store revolution

We forecast an earthquake in mobile gaming as app stores open up under legal and regulatory pressure. By 2030, we forecast $50 billion in transactions outside Google and Apple channels. Developers who adapt, through their own app stores or consortia, will reduce platform dependency, improve profitability, and attract more players to their ecosystems.

Strategies for the subscription era

It’s well-known that subscriptions will be a key revenue stream. Our report offers strategies for improving monetization, both subscription and one-off, such as “windowing”.

Subscriptions, combined with the increasing direct-to-consumer transactions enabled by the loosened app store rules above, are a powerful combo that will create winners and losers. For many games, user-generated content will be invaluable (we have a long section on strategies for UGC, which has potential far beyond its current teen/Gen-Z demographic).

In conclusion, as platforms collide, new business models will emerge, and traditional ones can be revitalized. The insights in this report provide a roadmap for developers, publishers, and investors to navigate this transformation and capture the next wave of growth.

You can download the full report, “How Platforms Are Colliding and Why This Will Spark the Next Era of Growth,” right here to see all of the insights and research for yourself.