As 2026 begins, there should be renewed optimism about the growth of the U.S. VC market, according to the year-end Venture Monitor report by Pitchbook and the National Venture Capital Association.

Despite an overall lack of new fundraising and a liquidity market that did not shape up as hoped in 2025, deal activity has begun a phase of regrowth, with deal count estimates

showing increases at each stage, and deal value, though concentrated in a small number of deals, falling just 8% short of the 2021 figure, the report said.

First financings are estimated to nearly hit the highs of 2021, as are early-stage funding rounds, both of which indicate high investor appetite for developing companies. The

other stage showing significant growth YoY is venture growth. While deal growth at this stage is a net positive for the market, venture-growth companies should be finding liquidity, and further capital raises at this stage signal further extension of liquidity cycles.

The report expects this growth to continue in 2026, particularly in deal count, as AI continues to penetrate the economy and new use cases are developed.

Some of these figures are a bit misleading, particularly deal value. And 50% of the 2025 deal value was invested in just 0.05% of the completed deals. Each quarter of 2025 also had more than $50 billion invested in megadeals, making for the first-, third-, and fourth-highest-valued quarters on record, despite 44% fewer megadeals than in 2021. However,

crossover investor deal activity continued to decline. These investors, which have traditionally supplied large portions of megadeal capital, have remained on the sidelines and completed the lowest number of deals of any year since 2020.

Corporates, on the other hand, showed a relative increase in deal activity, though they participated in just 21.3% of deals in 2025, down 6% from their high. The investors propping up the top end of the market are largely VCs, a change from the historical trend.

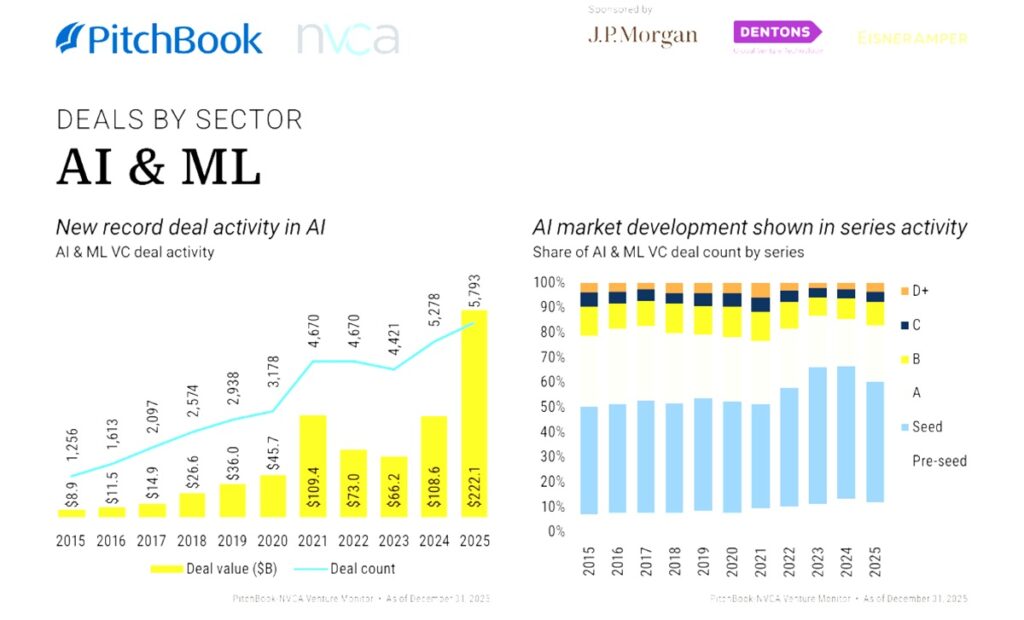

The easy explanation for the increasing deal value and count is AI, which represented 65.4% of deal value and 39.4% of deal count in 2025. Further data supporting the focus on AI is abundant. According to a Menlo Ventures study, enterprise AI spending scaled from $1.7 billion to $37 billion between 2023 and 2025.

That spending growth highlights not only corporate excitement for AI but also the fear of

being outcompeted in AI. The potential for AI technologies to be implemented across every sector also opens up endless opportunities.

As new AI companies are built to fill market needs, VCs keep putting money to work.

This fast-paced dealmaking market highlights a variable recovery for venture. Large firms with dry powder are controlling the market environment, including by increasing activity at the seed and early stages, while the lack of distributions have held back many firms from restocking capital stores to take advantage of the developing AI market.

The remaining value in VC funds has hit a high point of $1.02 trillion, finally surpassing 2021’s figure. This is due to the surge in markups, especially in AI, which now accounts for nearly 40% of US VC market value.

2025 IPOs generated a strong boost to exit value and a sense of returning liquidity. 17 unicorns went public, but more will need to realize returns for investors to make a significant dent in the negative cash flow to LPs over the past four years. While we expect

dealmaking to remain elevated in 2026, it may take longer for fundraising to return. The uncertainty hanging over the market in 2025, which manifested in tariff-related chaos and a government shutdown, is not as distinguishable in the current environment.

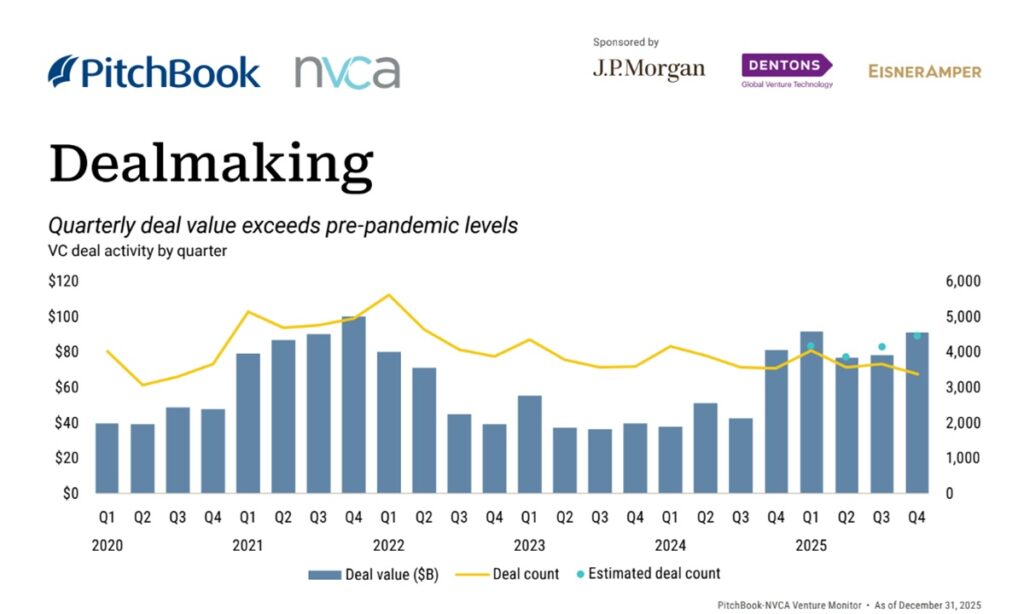

In the fourth quarter of 2025, $91.6 billion was deployed across an estimated 4,482 VC deals.

Quarterly deal value exceeded the prior two quarters and was nearly on par with the high-water mark set in Q1. Although activity continued to trail the 2021 peak, quarterly deal value in 2025 materially exceeded pre-pandemic levels, indicating a steady recovery from

a prolonged market downturn.

Dealmaking momentum in 2025 was sustained by later-stage activity. Late-stage VC and venture-growth deal value rose 45.4% and 131.1% YoY, respectively, with deal counts also increasing in both stages. At first glance, this expansion appears counterintuitive given the

prolonged liquidity constraints across the venture ecosystem. However, several factors help explain the trend. A small number of outsized transactions—particularly in AI and

other policy-favored sectors—captured a disproportionate share of capital in 2025.

High-performing AI companies continue to access substantial funding pools, supported by strong investor conviction and the escalating capital requirements of the AI development cycle. Corporate VC firms (CVCs) have also played a meaningful role, with many of them drawing on capital from their corporate parents to participate in large AI rounds. In 2025, VC deals with CVC participation totaled $196.7 billion—the highest level of the past decade.

Collectively, these dynamics have propelled later-stage deal value upward despite broader

market caution. AI continued to anchor total deal value in Q4. 11 rounds reached or exceeded $1 billion, and the eight largest deals were all AI related. The top 11 deals

totaled $37.4 billion, representing 41% of quarterly deal value and underscoring the market’s continued concentration in a small set of high-profile raises. In 2025, AI accounted for 65.4% of annual deal value—up 16.3% YoY—and 39.4% of deal count.

Anthropic’s $15 billion late-stage round was the largest deal of the quarter.

Project Prometheus’ $6.2 billion early-stage round also stood out: Founded less than a year ago, the company closed its first venture round with Jeff Bezos as both a co-founder and an investor. That transaction pushed Q4 first-financing value to a historic $12.8 billion; excluding it, quarterly first-financing value was roughly in line with the prior two quarters’ levels.

Investor conviction in AI remained strong throughout 2025, with substantial capital continuing to flow into the sector. Notably, outsized first financings became more prominent.

In Q2 2025, Thinking Machines Lab raised a $2 billion seed round backed by corporate investors such as Nvidia, multistage firms including Accel and Lightspeed Venture Partners, and government participation. The company was founded by the former

chief technology officer of OpenAI.

While large AI rounds are no longer uncommon, investors are increasingly willing to deploy significant capital into first financings, driven by confidence in exceptional technical talent despite the absence of mature financial metrics at this stage.