Niko Partners said Southeast Asia will reach $6.47 billion in revenues by 2029, up from $5.37 billion in games revenue in 2024.

The market researcher said Southeast Asia is known to intimidate companies hoping to enter the region. A multitude of languages, country-specific regulations, cultural differences, and local gamer preferences that need to be considered all present hurdles that must be overcome.

However, the region also provides rich opportunities for those who can reach their target

audience. For example, the last M6 Mobile Legends World Championship had 4.12 million peak viewers? In comparison the U.S.-based Major League Baseball peaked at 2.23 million concurrent viewers for its best season since 2018.

The region has a huge young, tech savvy populace who see games as part of

their lifestyle, making it seriously important for companies to understand and succeed

in.

Niko Partners has tracked Southeast Asia’s game market for the past 11 years. The region has seen massive growth over the last decade driven by tech adoption and mobile penetration, strong game communities and events, growing social acceptance of games—particularly esports—as popular mode of entertainment, and high social media and video platform engagement.

Although Niko Partners predict slower growth in Southeast Asia this year, due to economic and political issues affecting some of its constituent countries, the region still represents a huge opportunity for companies who can navigate the market. Read on to understand the unique insights needed to find success among one of the world’s largest regional gaming populations.

Southeast Asia to reach $6.47 billion market size by 2029

According to Niko’s Southeast Asia Market Model and 5-Year Forecast, the region

generated $5.37 billion in games revenue in 2024, up 5.2% year-over-year (YoY).

Revenue is expected to continue growing in 2025, albeit at a slower growth rate than in years past. The slower growth is due to current economic and political issues faced by some of the countries in the region, although Niko projects the growth to rebound in the coming years.

There are also slight declines in Indonesia and the Philippines driven by economic woes, as seen in the multiple protests taking place in both countries this year. There are many more details disclosed in the Market Model reports.

Key highlights

The region’s market is expected to grow 1.8% in 2025 to $5.47 billion. The market is forecasted to reach $6.47 billion in 2029 at a 5-year CAGR of 3.8%.

The Southeast Asia video game market had 285.82 million gamers in 2024, up 3.1% YoY. This will grow a further 1.5% to 290 million in 2025 and reach 324.4 million in 2029 at a 5-year CAGR of 2.6%.

Annual ARPU was $18.80 in 2024, up 2%. We expect ARPU to grow through 2029, reaching $19.96 in 2029, at a 5-year CAGR of 1.2%

Southeast Asia: A highly social gamer base

Niko’s SEA Gamer Behavior & Market Insights Report, which includes a survey of 3,131 gamers, provide key insights on player demographics, behavior, and engagement. Niko produces individuals reports for each market on an annual basis to help clients

understand developments and opportunities in the region.

Some findings: Southeast Asian gamers are highly social, with more than 45% of gamers

wanting in-game chat and ranking or scoreboard features in their games.

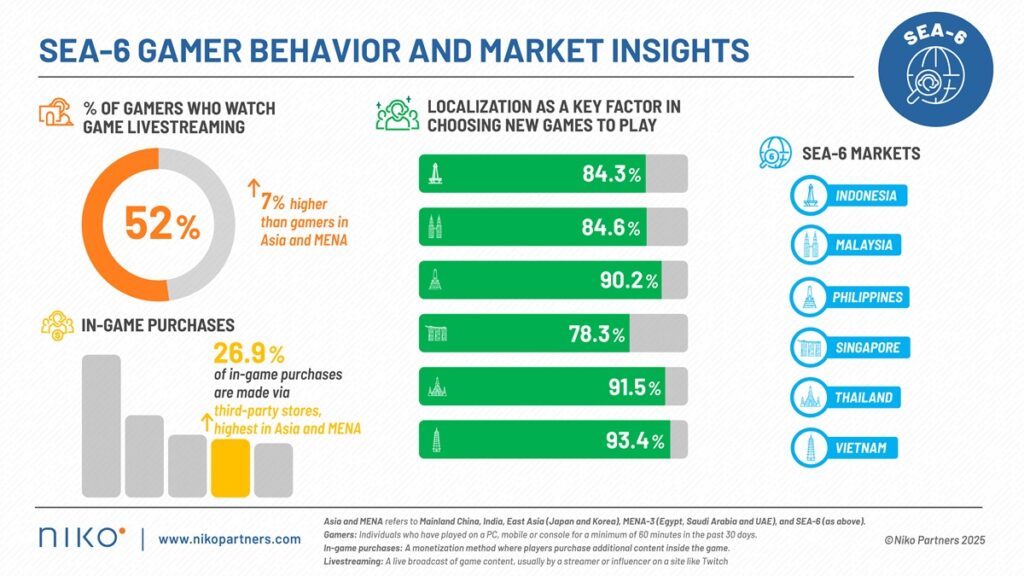

And 52% of SEA gamers watch game livestreams, higher than the Asia-MENA average of 45%. Game livestreams remain a popular activity for SEA gamers.

Gaming behaviors are shifting, with average weekly playing time seeing a decline to 15 hours compared to last year’s 21.8 hours. Similarly, Niko sees a rise of the share of non-spenders, with a 10-20 percentage point increase in each country.

Changes to play time and spending habits make it even more important for companies to understand how to reach their target audiences.

Popular genres and platform insights

One trend that has remained consistent since Niko started tracking Southeast Asian markets is the dominance of esports and competitive titles, even if different countries

have unique preferences for certain games.

For mobile, Mobile Legends dominates in Indonesia, Malaysia, and the Philippines, while Arena of Valor tops the market in Thailand and Vietnam. Understanding these trends at the regional and local level can help companies establish a foothold or improve market share in Southeast Asia.

Localization is important, from language to payments

Understanding the need for localization in each market is crucial, as there are different

priorities in each country, as far as player demands and expectations.

Gamer tastes, local financial structures, and language proficiency can all play a role – knowing what these are helps companies navigate the playing field. Globally successful games might not always find easy entry to the markets without thoughtful localization.

For example, across Southeast Asia, except for Singapore, a low credit card penetration rate and the highest adoption of digital wallets has produced a unique financial landscape that top companies are adapting to.

Mobile Legends includes SEA-based heroes or characters, while Genshin Impact has SEA languages options and features celebrations of local festivities Some insights about localizations from the Gamer Behavior report:

Localization remains crucial, with 87% of SEA gamers wanting some kind of localization. Thailand and Vietnam have the highest demand for localization, including language, with more than 91% of gamers in both countries seeing localization as a key factor in choosing new games to play.

And 26.9% of SEA gamers who purchase game items did it through a third-party store. This is the highest share among all regions that Niko covers, knowing which stores to prioritize may be a route to a quarter of the market.

E-wallets remain the most popular game payment option in almost all the

countries in Southeast Asia.