Gaming mergers and acquisitions and financings got off to a strong start in the first quarter of 2026, according to Drake Star Partners.

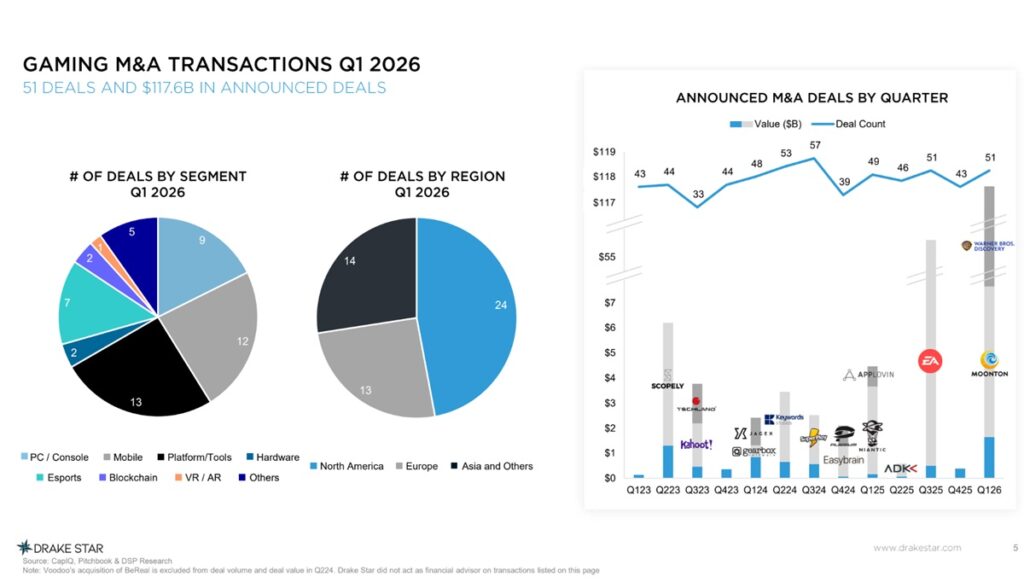

In Drake Star Partners’ Global Gaming Report Q1 2026, gaming and its adjacent industries saw landmark deals like Paramount’s $110 billion pending acquisition of Warner Bros. Discovery, which included Warner Bros. Games, and Savvy Games’ $6 billion acquisition of Moonton from TikTok.

On the company financing side, the activity was strong as well. XR, or extended reality, hardware was prominent in private financings with three deals that raised $100 million or more.

Michael Metzger, managing partner at the investment bank Drake Star Partners, said 2026

is set to be a historic year for game releases with the highly anticipated release of Grand Theft Auto 6 expected to be the biggest launch of all time. That could very well draw more attention from the larger investment community to gaming.

He said Q1’26 gaming M&A hit a 15-month high with 51 deals and over $100 billion in

disclosed value. Mobile led the activity, while the total valuation was driven by Paramount’s massive Warner Bros. Discovery deal, including Warner Bros. Games, and Savvy Games’ $6 billion acquisition of Moonton.

Other notable deals included majority stake acquisitions by Scopely (Loom Games, valued at $1 billion or more) and NCSoft (JustPlay, $202 million). Furthermore, Nazara acquired a controlling stake in Bluetile Games, Mattel bought out NetEase’s share in Mattel163, and Haveli agreed to acquire Budge Studios.

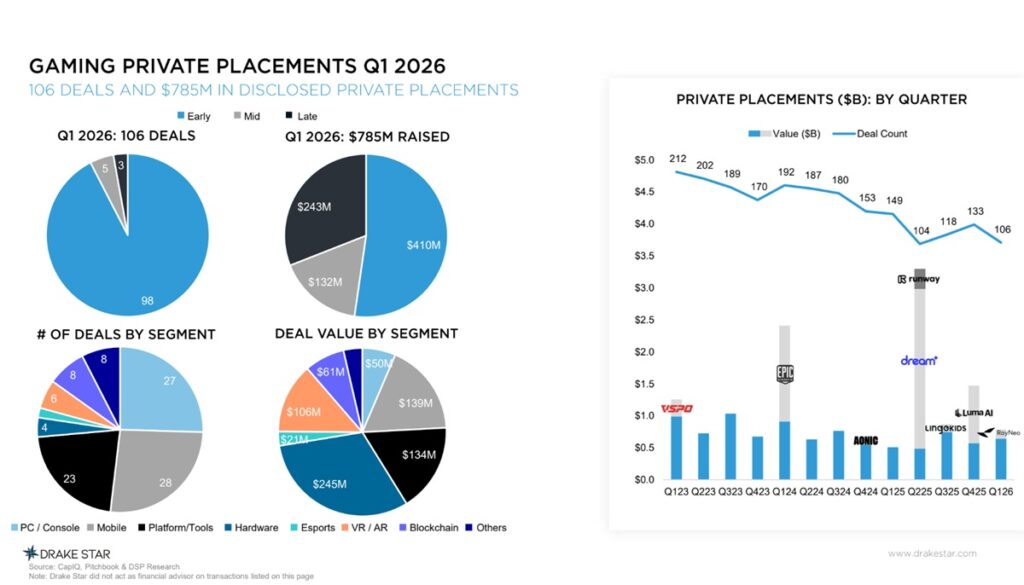

In private financings, Q1’26 saw 106 deals with disclosed deal value totaling $785 million. The 3 largest deals were in the AR / XR hardware category with RayNeo ($143 million), Xreal ($100 million), and VITURE ($100 million). Other notable rounds in include Ares Interactive ($70 million), VAST ($50 million), and ZBD ($40 million). Less than $200 million was raised for mobile and PC / console studios.

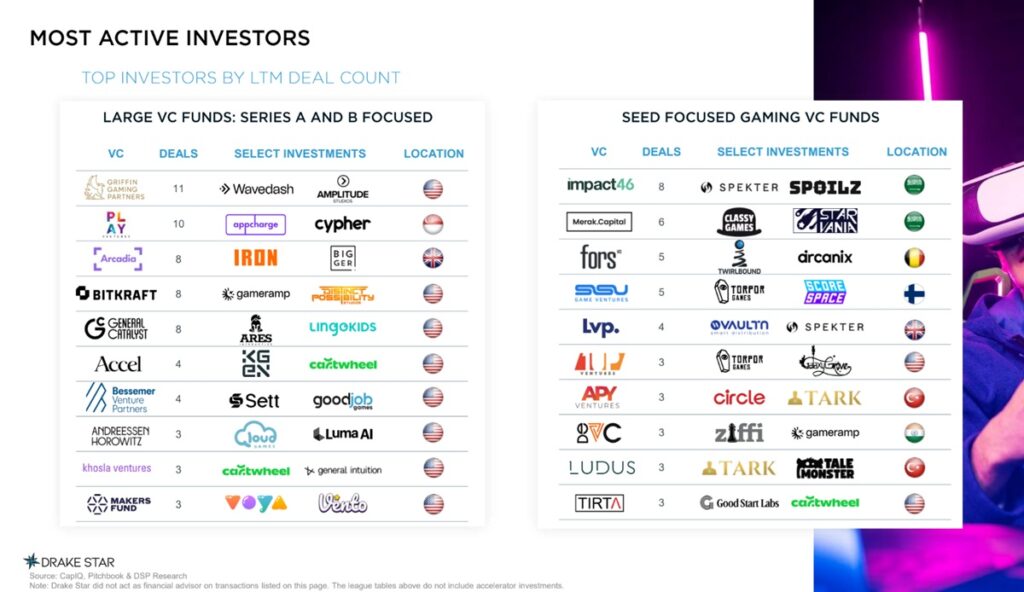

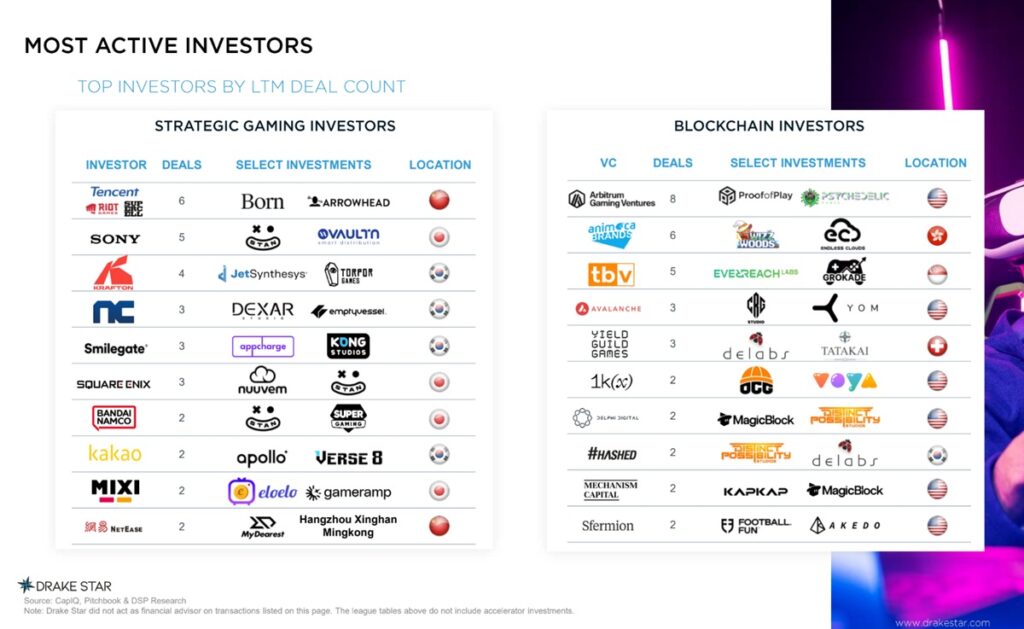

Over the last 12 months, Griffin Gaming, Play Ventures, and Arcadia topped large-fund activity, while Impact46, Merak, and ForsVC led at the seed stage. Tencent, Sony, and KRAFTON dominated strategic deals, with Arbitrum, Animoca, and TBV leading in blockchain. Animoca is attempting to pull off a SPAC, or special purpose acquisition company, which can circumvent IPO processes to going public. But Metzger has seen a drop in activity and interest in blockchain game companies.

Public deals were headlined by massive refinancings from Light & Wonder (owner of SciPlay in a $2.13 billion debt deal) and Playtika ($500 million). Hasbro added to the momentum by pricing $400 million in new notes, while LY Corp. doubled down on Kakao Games with a $201 million stake through equity and convertible debt.

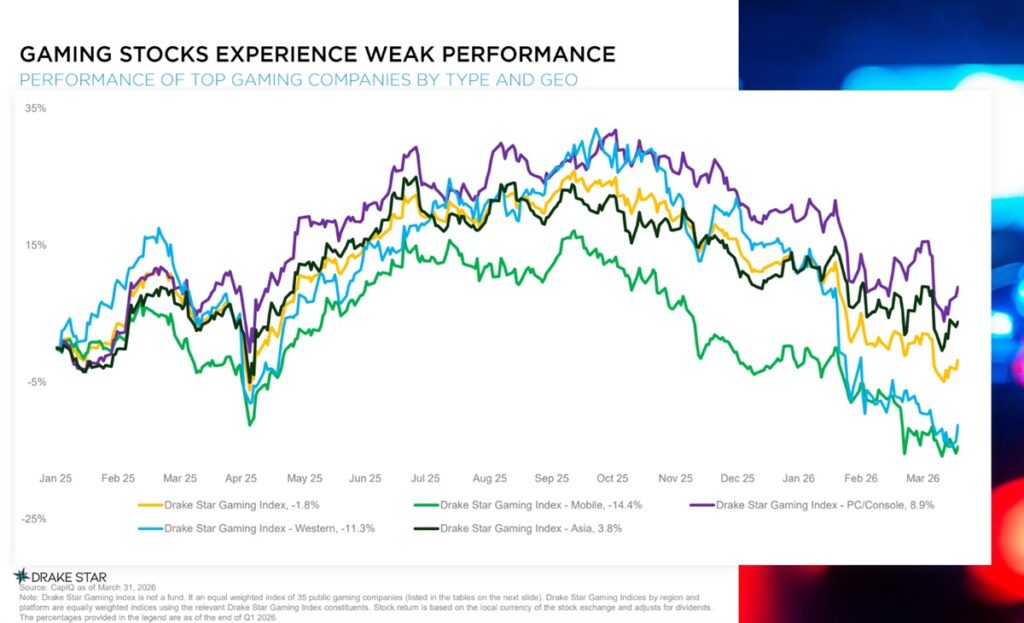

On the publicly traded company side, the Drake Star Gaming Index rose significantly through mid-2025 before giving back those gains, ending about flat since the start of last year.

Gaming stocks rallied in Q2/Q3’25, followed by a correction in Q4’25 and additional pressure from the broader market / software sell-off in Q1’26. PC and console companies, along with Asian publishers, significantly outperformed their mobile-focused and Western peers. Pearl Abyss led with a 149% gain, fueled by a strong Q1 2026 and the success of Crimson Desert, which sold more than five million copies in its launch weeks.

Some queries

I asked how Drake Star accounts for deals like the Paramount purchase of Warner Bros. Discovery. The $110 billion figure is the enterprise value, or the net amount paid when you consider the acquirer assumes the debt of the acquired company and also gets the cash that the acquired company has. But Metzger said he did not know how much the gaming division of Warner Bros. itself was worth, give it had perhaps $1 billion to $1.5 billion in revenues in any given year while the rest of the company had perhaps $45 billion in revenues.

“I don’t think they valued it independently. My understanding is WB Games was more like a ‘nice to have'” in addition to the rest of the business. He noted that Paramount’s execs are excited about the deal and Paramount wants to be more active in games.

I also noted that the Saudis were part of all the big deals and have invested in so many companies, taking small stakes in the likes of Nintendo and Capcom. Those deals help spread its risk out among more companies but also help it double down on its bet on the entire game industry, Metzger said.

Asked about the report and what it says about the health of gaming, Metzger said one thing he found very encouraging was the number of M&A deals at 51 in the quarter. That was equal to Q3 2025, and it was a high number given recent history.

“There are a good amount of really big deals, but also a good amount of mid-market deals happening,” he said. “I think that’s definitely very positive on the financing side. And that’s talking about the health of the industry. We saw the three biggest deals for financing were for the XR companies, and they all have gaming applications.”

There were also big deals like the $70 million raise for Ares Interactive.

At the same time, Metzger said there isn’t a lot of venture capital money being invested in game studios. Rather, the pattern is more project financing, or user acquisition funds for mobile games and publishing deals for PC games.

The war’s impact

Asked about the war, the price of oil and rising inflation, Metzger is concerned about falling consumer demand due to the economy. Disposable spending, which includes games, is being reduced due to all of the rising costs, he said.

“It definitely doesn’t help,” he said.

As a result, the last six months of public equities valuations have been pretty tough, especially for gaming. In Q1, the gaming stocks dropped.

The other problem is that gamers want and need new game consoles, but Microsoft and Sony haven’t lined up anything until perhaps 2028. The rise in memory chip prices could be to blame, since AI chip demand is so high. But if new machines do come out, the memory chip prices could push the costs to $1,000, and gamers won’t like that.

As for AI, the tools will likely make it easier for smaller companies to launch games. But there will be a flood of new games and that means more competition. As for direct-to-consumer trends thanks to the app store rulings, the mobile game industry is benefiting.

Outlook

Drake Star Partners expects a robust M&A market with a healthy amount of mid-market deals and some big ticket deals for the rest of the year. The firm is hopeful that excitement about gaming equities will accelerate as we near the launch of GTA 6, likely the biggest game release ever, now targeted for November 19, 2026.

Other highly anticipated games include Marvel’s Wolverine from Insomniac Games and 007 First Light from IO Interactive.

Metzger believes we will see more large deals and more mid-size deals in acquisitions. And with the launch of GTA VI, there’s “going to be just more eyes on the gaming industry.” GTA VI is sure to generate more excitement, he said.

But there are ten active game companies when it comes to potential acquirers in gaming.

Key strategics to watch include PIF/Scopely, Netflix, Tencent, Krafton NCSoft, MTG, Take-Two, everplay, and Keywords Studios. Metzger expects private equity to remain a major market catalyst, particularly as more publicly listed gaming firms become attractive targets for take-private transactions.

Metzger believes Tencent and Miniclip will likely become more active in part because they haven’t been as active recently. He also thinks Netflix will make additional acquisitions.

AI, UGC, and tech platforms will stay at the forefront of investment, likely joined by a surge in AR activity. With studio equity still facing headwinds, project financing has become the primary path forward. Meanwhile, the rise of dedicated UA funds offers a new lifeline for mid-stage mobile studios looking to accelerate growth.

“We’re pretty excited about the rest of the year, from an M&A point of view, I think it’s going to be a good year. And, yeah, hope that public equities will recover towards the end of the year,” he said.

All eyes are on the IPO pipeline as Discord and PlaySimple gear up for potential public offerings.

As for Discord and PlaySimple lining up IPOs, Metzger thinks it will happen but a lot of the growth could be happening in regions like China, where Chinese companies are becoming a bigger part of the market.

“I think we will see many more games made in China,” he said.