The early stage venture capital market will see a surge in deal activity in 2026, according to a report from Pitchbook. The company published the report in December, but we’re just getting around to writing about it now. Still, it’s data worth knowing.

Late-stage deal activity will remain strong and liquidity will return, though recovery will remain uneven. Fundraising has bottomed out, and a gradual rebound awaits as distributions and LP sentiment improve.

Introduction

Optimism in the U.S. venture market heading into 2026 may not differ much from that at the start of 2025. Public markets had been trading at or near all-time highs, liquidity is still a major concern for venture capital, and further rate cuts are expected as the new year begins.

Meanwhile, geopolitical tensions continue, though their impact on markets has somewhat lessened, and inflation is back to where it was a year ago. U.S. GDP growth has returned to an annualized rate of 3.8% (as of Q2), aligning with the 3.6% rate from a year prior.

What is different is that the Trump administration has had nearly a year to implement its policies, reducing the chances of legislative surprises in 2026. Now, the likelihood of rapid regulatory change in the market is low, contrasting sharply with last year when the changing administrations raised hopes of an M&A rebound and a more relaxed regulatory environment.

Overall, Pitchbook maintains a cautiously optimistic outlook for 2026, expecting tempered growth in IPOs, relatively improved market liquidity through secondaries, and continued growth in the number of completed deals, especially at the early stages.

Liquidity will remain the primary challenge for the VC market in 2026. Despite a rebound in exit value in 2025, the year’s total is projected to fall below $300 billion, trailing not only 2021 but also 2020 and 2019. Fourth place is not bad, except that the net asset value (NAV) of VC has doubled since 2020, with the prior three years also having relatively low exit values.

However, both big-ticket M&A and the number of unicorns going public noticeably increased in 2025. Exits of $500 million or more accounted for 91% of total exit value through Q3.

Pitchbook expects exit counts to continue to increase. Barring a major market event, public market multiples will likely keep expanding. Although the Federal Trade Commission has not explicitly commented on lowering M&A barriers, none of the year’s large deals has faced as much scrutiny as it might have under the previous administration.

This is another positive sign for the market. With nearly half of unicorns being held for at least nine years, liquidity for these companies cannot rely solely on the public market.

Despite these positive indicators, broad limited partner sentiment remains poor. Since 2022, net cash flows to LPs have been negative by $169 billion. The time to close new funds has increased sharply as LPs hesitate to commit more capital without any distributions.

This has led to a concentration of capital among established firms. We knew that

traditional venture mechanics would break with the extended liquidity timelines, and

we are starting to see that happen.

2026 U.S. venture capital outlook

On the dealmaking side, AI continues to foster optimism. It was a key driver of the surge in billion-dollar funds, and the nature of the AI market has significant implications for venture. AI startups have captured 65% of the total VC deal value in the U.S. year to date, and more than half of new unicorns are AI companies, said Kyle Stanford, director of Research for U.S. Venture, in the report.

Other contributors to the report were Emily Zheng, senior research analyst; Kaidi Gao, senior research analyst; and Susan Hu, quantitative research analyst.

The market value of AI startups exceeds $1 trillion. AI is often seen as a single sector, such as climate tech, or a specific business model, such as software as a service; however, it is increasingly becoming an essential part of a broader range of industries, including biotech, enterprise productivity, and the previously mentioned climate tech.

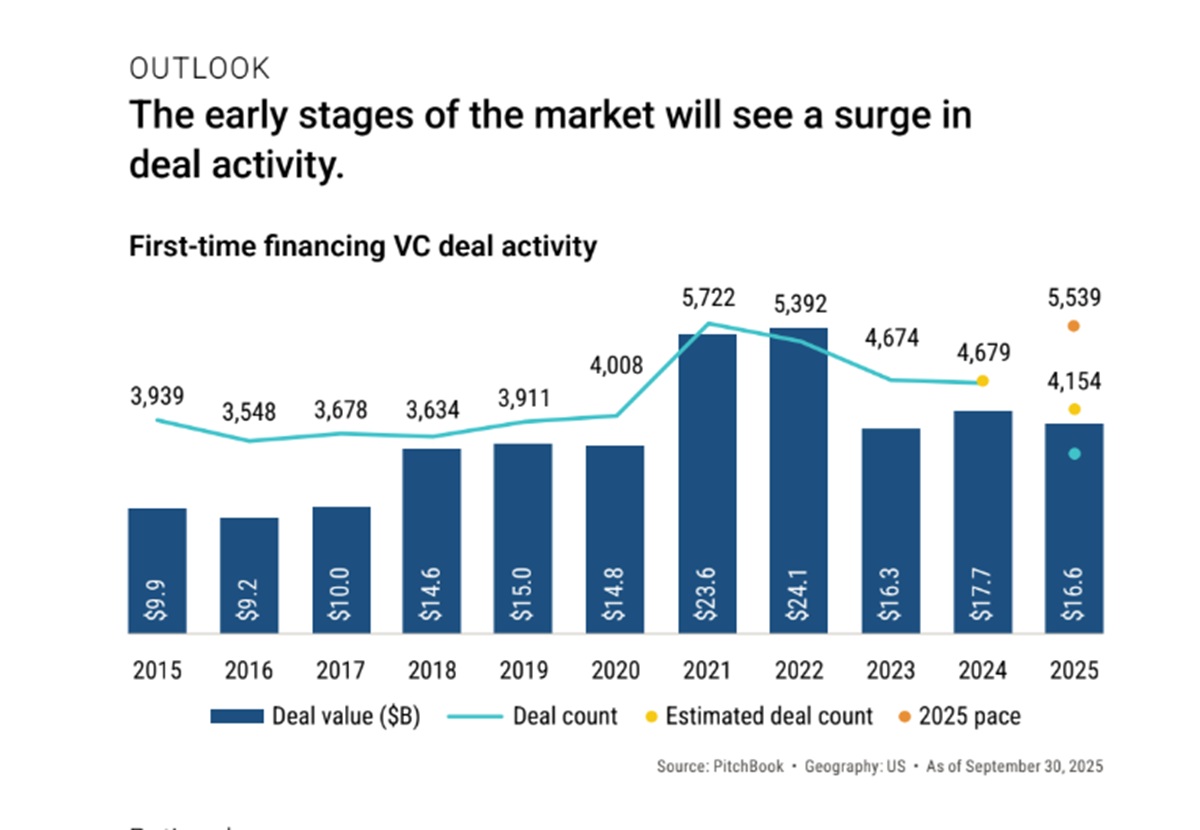

There is an endless stream of new AI tools being developed and adopted by corporations worldwide. It has been challenging for large companies to develop their own AI tools, so many have turned to tools created by startups. Through the first three quarters of 2025, first-time financings were nearing the all-time high set in 2021.

While this has led to a rally in the early stages of venture, it has also led to crowded vertical segments that will bifurcate into a few winners and many losers. The pace of investment in AI continues to increase despite the venture market’s slow liquidity and low fundraising levels. Should those flip in 2026, deal counts could reach levels seen in 2020 and 2021.

Pitcbhook is more optimistic about early funding stages than it has been since 2021 because of AI, its rapid development cycles, and its growing demand from global corporations. Still, continued improvement of liquidity markets is necessary. IPOs may

not be the most common exit path, but they will be crucial in expanding liquidity.

Deal count expected to rise in 2026

It is counterintuitive to expect increased activity in the early stages of venture during a liquidity slowdown and a sluggish fundraising market, yet the early stages have already begun to defy expectations. Through Q3 of this year, venture funds closed only $45 billion in new commitments, the lowest total since 2017.

Additionally, many small funds and emerging managers that raised capital in 2021 or even 2022 have likely used most of their dry powder and are unable to be active investors, at least to the extent needed to boost deal count. And yet, first-time financing activity through the first three quarters of 2025 was just 200 deals behind where 2021 stood in the same time frame, which has since become the high-water mark for first-financing deal count.

On top of that, early-stage deal count increased in each of the past three quarters, and the estimated early-stage deal count for the full year is roughly on par with full-year 2023 and 2024 totals. Since the 2022 slowdown, the idea of VC investment refocusing on early stages has manifested in a thriving early-stage market; however, the 2024 seed deal count

was still 27% lower than in 2021.

Clashing with the narrative of a refocused investor base was the hesitancy of investors to continue working through dry powder without meaningful markups in order to avoid returning to LPs without leverage for a new fund.

Pitchbook believes this has begun to change. Down and flat rounds peaked several quarters ago, and late-stage activity has picked up. As more managers see markups from

past investments and the rising value of funds, this should loosen their grip on their

remaining dry powder and boost activity as they look to capitalize on AI opportunities.

2026 U.S. VC outlook

Macroeconomic shocks will also have a relatively lower impact on the early stages of VC in 2026. Even in 2025, macro challenges such as tariffs were unable to sway activity outside of select verticals that were directly impacted by them. More broadly, business starts in the US are near all-time highs. Though a large majority are not VC investable, the uptick shows that the entrepreneurial spirit of the US has not dampened with the uncertain markets of the past few years.

Two major trends directly point toward 2026 being a highly active year for the early stages of the VC market. First, AI has driven investor focus and shrunk the cost of building a company. This is not novel, as hype and costs are two directly relatable trends that can impact investment.

Second, multistage investors with unlimited follow-on capital have increasingly invested in seed and Series A rounds, and the data supports their recalibrated strategy. Andreessen Horowitz has invested in more than 300 seed and Series A deals since the beginning of 2024 (as of November 7, 2025), and there is reason to believe more large firms will adopt this strategy.

AI investments

AI has become ubiquitous in VC, drawing 65% of capital invested through Q3. This figure is skewed by the multibillion-dollar rounds that have occurred this year, but in general, it illustrates the current interests of investors in AI. However, several other data points speak more directly to the speed and development of AI in VC:

- 37.1% of non-life-sciences first financings in 2025 have been for AI companies (up from 21% in 2022).

- The median age of AI startups receiving their first investment is 65% lower than that of non-AI startups.

- The median time between rounds for AI companies is three months shorter and falling, while it is growing for non-AI companies.

As mentioned before, first-time financings in 2025 are pacing to fall behind only 2021 in terms of completed deals. This is not a coincidence; AI is driving that growth No other emerging technology has accounted for a larger share of total deal activity.

In fact, mobile made up about 20% of deal count in early 2013, the second-highest proportion after AI’s current 35%. It may not be a direct comparison, but it still demonstrates AI’s dominance.

To compare AI more broadly with software, more than 40% of companies raising capital in 2025 have been software companies, and AI will likely be adopted by a much wider range of companies. As AI continues to develop in functionality and accuracy, its use cases will only increase.

Multistage investors

Amid limited partner hesitance, multistage firms have captured pricing power and are acting more like seed-stage investors with endless follow-on capital. These large investors can deploy spray-and-pray tactics, with less weight on the “pray” because of the size of their funds.

The median seed deal size has nearly reached $4 million YTD, and fewer stakes are being acquired, placing the onus on managers to remain disciplined in pricing while competing against market giants. This will continue in 2026 and likely be a market standard beyond next year.

The data shows that paying up at the seed stage works. Top-decile seed and Series A rounds by valuation exhibit higher annualized returns, with lower loss rates than lower-valued rounds. Casting a wide net in early deals boosts return potential for these firms, as long as they can identify and keep investing in winning companies. It ensures access to follow-on rounds and strengthens their portfolio companies against competitors that may not have as deep-pocketed of backers.

Five of the 20 most active seed and early-stage investors are multistage firms: Andreessen Horowitz, General Catalyst, Khosla Ventures, Sequoia Capital, and Lightspeed Venture Partners. Bessemer Venture Partners is not far behind. Together, these funds have made over 400 seed and early-stage deals in 2025, pacing for their second-highest combined total, behind 2021.

Bonus outlook: These trends will also drive geographic consolidation

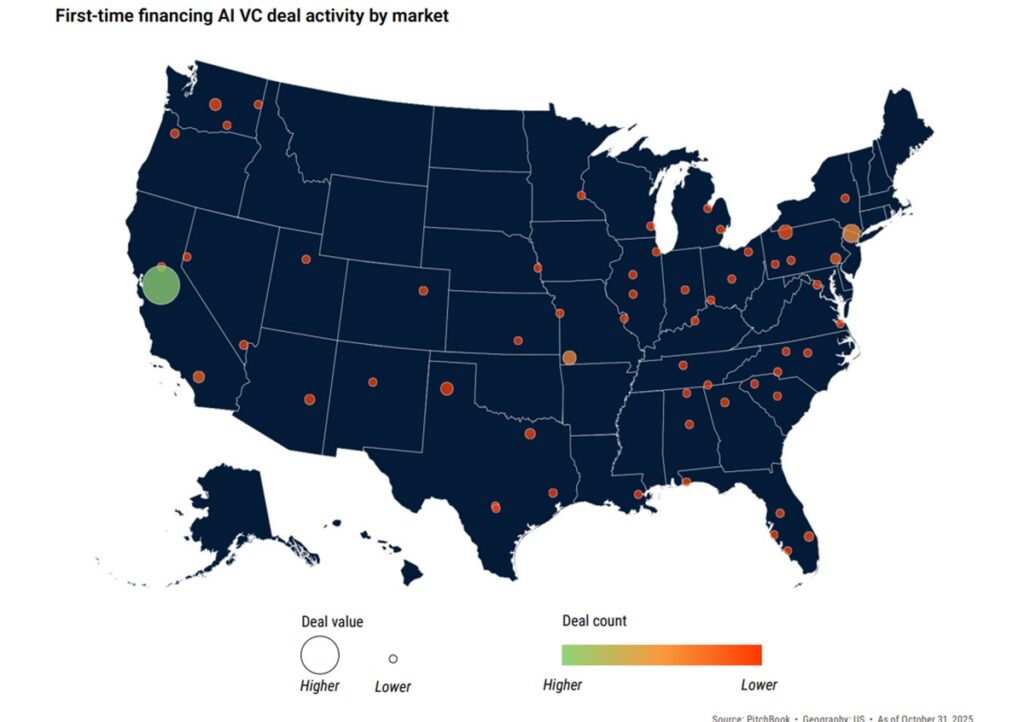

During the COVID-19 pandemic, capital was more widely spread across the U.S., leading to an increase in investment outside of the Bay Area, New York, Los Angeles, and Boston.

That has changed. Nearly 70% of the funds closed through Q3 have been located in those four markets. While capital typically does not remain inside a specific market, it does not tend to stay close in the early stages in particular. However, after a significant spike at the onset of the pandemic, the median distance in miles between a seed lead investor and the target company has declined each of the past three years.

Of Andreessen Horowitz’s seed deals in 2025, 81.4% have been made in California or

New York, two markets where it has physical offices. With the surge in AI, it is unsurprising that the Bay Area has held its highest share of total deal count since 2018 during the past two years. More than 36% of completed deals in 2025 have occurred in just the Bay Area and New York. With Y Combinator running four batches in person, more capital will be pulled into the Bay Area, and deal volume will increase. For fast-moving markets, in-person deals will always provide investors with the best chance for access. For now, the Bay Area and New York lead in company formation and investment opportunity. As long as AI continues to be the focus, these markets will remain the leaders.

For AI first financings, the Bay Area leads the way by a wide margin. With its large amount of local capital and high speed of financing, both outside investors and founders will continue to be drawn into the Bay Area, further increasing its activity.

Risks

This outlook seems almost too optimistic. The liquidity market is not in much better shape than it was at the end of 2024; market uncertainty may be slightly lower, but the chances of a recession remain high; and the AI market appears a bit bloated from the rush of investment, given that it is still very top-heavy. However, those risks have not caused a widespread drop in activity before.

The biggest risk in early-stage investing is likely the ongoing difficulty for emerging managers to raise new funds. While multistage managers may boost their activity, and AI will keep channeling more money into VC, emerging managers invest in many companies both inside and, importantly, outside major capital hubs. Emerging manager funds from 2021 and 2022 are probably running low on dry powder and need new vehicles for fresh investments. Data shows that only 33% of first-time managers in 2021 went on to raise a second fund, and just 12% of new managers in 2022 had follow-on vehicles. The past two years have shown a significantly different market for emerging-manager fundraising, with investors focusing on track record and distributions, which few emerging managers can generate early on.

Later-stage deal activity will remain strong

Late-stage VC deal activity has proven resilient in 2025. Annualized late-stage VC deal value stands at $107.6 billion across an estimated 4,459 deals—on pace for the highest total in a decade, second only to 2021. Deal value has steadily recovered since 2023.

Venture-growth deals are performing even better. Annualized deal count is tracking for a record high, and the stage’s share of total US VC deal count has risen steadily since 2022, notching 6.7% YTD. This indicates continued strength among mature startups nearing the end of the venture lifecycle due to sustained appetite and capital availability allowing these companies to stay private.

With this in mind, we expect a modest YoY uptick in the combined deal activity of the late and venture-growth stages in 2026 driven by the AI investment boom, as well as a relatively strong exit market that should elicit an increase in crossover and corporate investment. However, this will not come without hurdles for many companies that have

matured into the later stages without harnessing an AI story. A widening quality gap will translate into top-tier startups continuing to raise outsized rounds to fuel growth and potentially prepare for a near-term exit while mediocre ones struggle to meet growth expectations and garner investor traction.

Through the first three quarters of 2025, the number of active unicorns in the U.S. grew

to 830, with their total post-money valuation reaching a record $3.9 trillion—a tenfold increase over the past decade. However, this growth cannot continue indefinitely. A large amount of capital remains tied up in these private companies. Many unicorns have slowed their growth, which has increased liquidity constraints. These companies face mounting survival challenges and struggle to attract investor interest for follow-on funding.

The divide remains clear: AI-focused and rapidly growing startups continue to access

substantial capital from sources such as multistage funds and strategic investors. Through Q3, AI accounted for more than 28% of late-stage deal count in 2025, up from 24% in 2024 and 21% in 2023. This trend makes sense, as the current AI boom largely began in late 2022. The top-performing companies continue to raise private capital, demonstrating sustained investor appetite for these deals.

This divergence is most evident in the later stages: Strong startups are raising funds to support growth and prepare for an exit within the next year or two, while others, including many that reached unicorn status during the 2021 market boom, may never deliver outsized returns. Since 2023, the median pre-money valuation for Series C and D+ deals has steadily increased, reaching $307 million for Series C—the highest in a decade—and $838.8 million for Series D+ YTD. Top-quartile pre-money valuations have also risen consistently, reflecting high investor caution and capital selectivity.

Again, AI demonstrates its dominance and its influence on the late-stage divergence. YTD, the median deal value for AI startups has exceeded that of their non-AI counterparts by 25% at Series C and 26.7% at Series D+, indicating investor confidence and increased investment in AI. Additionally, the share of Series C and D+ deals within all US AI & ML VC rounds has grown steadily since 2023, increasing to 8.5% YTD from 5.8% in 2023.

This growth suggests more AI startups are reaching maturity and raising capital to

compete in a crowded market.

Pitchbook expects the AI investment boom to maintain momentum at later stages. The largest deals in recent quarters have tended to be for select later-stage AI startups. Beyond these high-profile names, there is a notable disparity in deal value between AI and

non-AI startups at later stages.

Venture-growth deal activity in 2025 is on track for a record year. Annualized deal value has surged to $150.2 billion, surpassing the 2021 record of $91.6 billion. The annualized deal count matches 2021 levels, but the total value is boosted by several large AI rounds: $40 billion, $14.8 billion, $13 billion, and $3.5 billion. Growth at this stage of VC indicates a key trend: Companies are staying private longer.

VC-backed exits showed signs of recovery in 2025 but fell short of expectations for a widespread IPO wave. Some prominent tech listings such as Figma and CoreWeave highlighted public appetite for high-quality companies, yet few IPOs in 2025 have

matched their private valuations. The IPO window remains open—though not wide open.

While Pitchbook expects increased liquidity, i is less certain that it will be driven by an

expanded IPO market. This may lead companies to raise more funds in private markets, creating more opportunities for investment and, somewhat artificially, boosting venture-growth investments as companies seek capital to sustain growth. These rounds will likely account for a significant share of late-stage VC and venture-growth deal value over the coming quarters.

Participation from nontraditional investors in large, later-stage deals will be essential to maintaining momentum in the final stages of the venture lifecycle. So far in 2025, these investors have participated in approximately 3,930 VC deals totaling $194.7 billion—the second-highest deal value in a decade, behind only 2021.

Although deal count with nontraditional investor participation has steadily declined since 2021, deal value has increased since 2022. This divergence suggests that nontraditional investors—especially corporate venture firms, PE funds, and sovereign wealth funds— continue to support select large transactions even as overall activity moderates.

What has been missing is hedge funds, which injected money into VC during the 2021 cycle. These investors might see an opportunistic market if rates fall enough during 2026.

Late-stage VC risks

Much of the recent strength in late-stage VC and venture-growth deal activity is tied directly to the AI boom. Many mature AI startups are trading at elevated valuations,

supported by expanding revenue multiples in the public AI sector. If public AI valuations contract meaningfully, private AI startups will likely face similar markdowns.

That would weaken investor confidence and reduce the capacity or willingness to deploy large amounts of capital into this category.

In addition, a weak exit environment in 2026 would add pressure. The rebound in exits during 2025 helped hold up later-stage activity by improving expected returns. Any reversal in that trend would dampen investor appetite for startups approaching an exit

and slow the pace of large later-stage investments.

Liquidity will return, though recovery will remain uneven.

The IPO window creaks open for select sectors

With valuations stabilizing, interest rate cuts likely to continue, and renewed investor appetite, the groundwork laid in 2025 suggests that 2026 will mark the beginning of a sustained recovery in liquidity. More startups are realigning their valuations with fundamentals, and investors are growing comfortable with down rounds, both of which should encourage more IPO filings.

Valuation compression remains a persistent hurdle, as the median US IPO valuation for unicorns relative to their last VC valuation is 0.9x YTD. However, down round IPOs are no longer stigmatized but now the norm, with two-thirds of 2025 unicorns going public at a valuation lower than their private market peak. Though painful in the short term, this recalibration is a welcome and essential step toward a healthier, more durable recovery of exits, allowing startups to move past the golden handcuffs of their peak pricing.

Pitchbook’s favorable outlook predicts 68 IPOs in 2026: the decade average excluding 2021. This average is 44.7% higher than 2025’s projected total IPO count, so reaching that level hinges on a set of favorable macro conditions, such as decreasing interest rates, market volatility, and valuation compression.

In the absence of these tailwinds, Pitchbook’s unfavorable scenario assumes IPO activity remains at 2025 levels of 47 offerings, only slightly above the post-pandemic years. This modest level of liquidity could still offer meaningful relief to VC if a handful of high-value listings generate significant distributions. Realistically, 2026 is shaping up to be a measured continuation of the IPO recovery, not a breakout.

The IPO window is expected to reopen slightly but remain highly selective, favoring

companies with exposure to sectors with regulatory support, similar to 2025.

Excluding healthcare and life sciences, 90% of YTD IPOs have occurred in AI, crypto, fintech, defense, and space, which are sectors that have benefited from favorable policies.

For example, the IPO of stablecoin issuer Circle coincided with the passage of the Guiding and Establishing National Innovation for US Stablecoins (GENIUS) Act and was soon followed by crypto exchange Gemini’s listing. A month after the government increased its investment in transformative space technology, defense and space technology firm Voyager completed an oversubscribed IPO, followed by space transportation firm Firefly Aerospace’s IPO two months later.

Overall, the recent wave of IPOs appears to be opportunistic rather than a systemic reopening. Barring a macro shock or renewed volatility, IPO counts are expected to rise

incrementally throughout 2026, but the window will remain narrow and biased toward

select sectors.

Venture secondaries are set to play an even larger role in 2026. For investors, secondaries offer a mechanism to realize returns without IPOs or M&A; for startups, they provide flexibility to extend private lifecycles while reorganizing cap tables, replacing early investors with long-term shareholders less constrained by the typical 10-year fund horizon.

2025 marked a turning point in institutional and retail engagement in secondaries. Wall Street’s wave of consolidation—including Goldman Sachs’ acquisition of Industry Ventures, Morgan Stanley’s purchase of EquityZen, and Charles Schwab’s move for Forge Global—signals that venture secondaries are maturing into a growth engine for advisory, underwriting, and wealth management. More large financial institutions are expected to

follow suit in 2026, highlighting how secondaries are becoming a valuable bridge between

private and public markets.

Special purpose vehicles (SPVs) have become the market’s fastest-growing access channel for retail engagement, granting exposure to coveted late-stage startups once reserved for institutional investors. Compared with 2023 levels, the number of secondary SPVs is up 682% and capital raised has surged 1,340% YTD.

A sustained rebound in primary dealmaking and exit activity would provide much-needed pricing benchmarks and significantly increase secondary participation.

Without that momentum, the market will likely continue its gradual expansion, supported by rising valuations and the normalization of secondaries, whether through company-sponsored tender offers, institutional acquisitions, or retail demand.

For many investors, a combination of policy tailwinds, pricing opacity, and restrictive transfer controls will continue to limit transaction volume to a narrow set of elite companies, particularly those with recent primary rounds or ties to sectors such as AI, defense, and fintech. Most opportunities will remain concentrated among established secondary investors with the scale and access needed to secure full information rights.

Risks

Venture’s biggest startups are expected to remain private, buoyed by substantial

capital reserves and tender offers, which would limit the upside in IPO exit value in 2026.

An increasing number of private companies are restricting secondary transactions, led by OpenAI’s decision to void any share transfers without written consent. The move signals a broader intent among top-tier startups to centralize and control liquidity, favoring company-led tender offers over third-party transactions. As a result, retail platforms such as EquityZen and Forge Global are competing for a shrinking pool of tradable assets, and this mounting pressure likely led to their recent acquisitions.

Without an increase in primary dealmaking and exit activity, well-capitalized investors will continue to dominate while others become sidelined, restricting the secondary market’s growth.

The explosive rise in SPVs has widened access to private companies but also introduced new layers of complexity. The mid-2025 collapse of fintech platform Linqto, which allegedly misrepresented investor ownership in more than 500 SPVs, illustrates the potential risks for less sophisticated investors.

Fundraising has bottomed out, and a gradual rebound awaits as distributions and LP sentiment improve.

Pitchbook expects fundraising to increase in 2026, supported by improving liquidity and gradually recovering LP sentiment. The exit environment is strengthening, helping restart the venture flywheel and restore the flow of capital back into the ecosystem.

Fundraising in 2025 remains subdued, with about $55 billion raised across 451 funds YTD, well below the 2021-2022 peak. The main constraint has been the persistent lack of liquidity, which has kept LPs cautious and concentrated commitments among established firms. Despite roughly $169 billion in cumulative negative cash flows since 2022, recent data through early 2025 suggests conditions are bottoming out, aided by more active exit and secondary activity. If momentum continues, fundraising could reach $100 billion to $130 billion in 2026, based on the historical link between distribution yields and fundraising trends.