Game company acquisitions are setting new records. In the first three quarters of 2014, acquisitions of game companies have topped $12.2 billion, or more than double the total amount for last year, according to game investment bank Digi-Capital in London.

Five large deals boosted the numbers this year, including Microsoft’s $2.5 billion acquisition of Minecraft maker Mojang; Facebook’s $2 billion acquisition of Oculus VR; Giant Interactive’s $1.6 billion deal to go private through a management buyout; Amazon’s $970 million acquisition of game livestreaming site Twitch; and Zhongji’s $960 million purchase of the game assets of FunPlus.

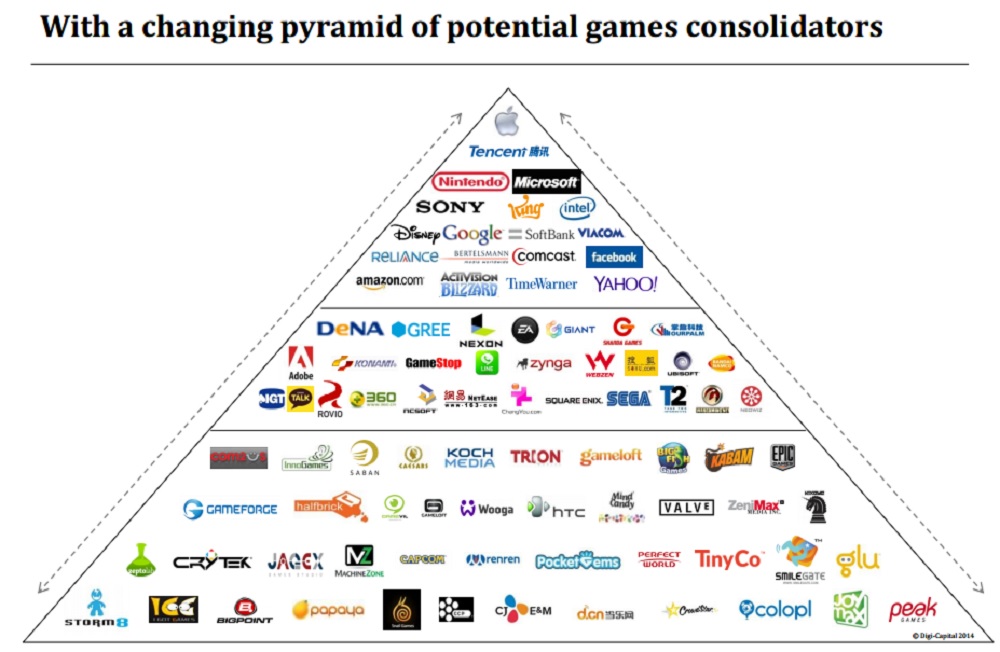

The Microsoft-Mojang deal was reportedly valued at 8 times revenue and 20 times profit, while Giant’s deal was value at 8 times revenue and 12 times operating profit. Tim Merel, managing director at Digi-Capital, said in a report that the big drivers of consolidation include mobile growth, mobile cannibalization, legacy pivots from one market to another, stock market cycles, and regional realignments.

Excluding the big deals, game acquisitions are running at similar levels to the previous record year in 2013. American and Chinese buyers dominated among the top 10 game acquisitions. Chinese companies accounted for five of the acquirers, and 5 were U.S. acquirers. That compares to 2013, when 9 of the top 10 were Chinese and Japanese acquirers.

The drivers of the game business are the growth in mobile and online games. Digi-Capital predicts the total game software industry revenue will grow from $70 billion now to $100 billion by 2017. Mobile and online games could grow at a compound annual growth rate of 23.7 percent from 2011 to 2017, with the total hitting $60 billion in 2017.

Returns for game investors hit 11 times investments so far in 2014. Game investment has reached $1.1 billion through the third quarter of 2014. That compares to $1 billion in investments in game companies for all of 2013. Mobile games and game technology are the top sectors this year for investment.

Asia is the biggest driver of economic value in mobile and online games. Digi-Capital estimates that Asia and Europe could take more than 80 percent combined market share for mobile and online games.

Among game-related initial public offerings, 15 out of 18 IPOs from 2011 to Q3 2014 were by Chinese, Japanese, or South Korean companies. Games accounted for 32 percent of mobile app usage in 2013 and 74 percent of mobile app revenue in 2013.

Average M&A deal size grew 145 percent from 2013 to $174 million through the third quarter of 2014. Investment values rose 45 percent through Q3 2014 from 2013.